The KRX system is the necessary infrastructure for deploying the Central Clearing Counterparty (CCP) model, thereby improving the Payment Cycle (DvP) criterion.

The KRX system is the necessary infrastructure for deploying the Central Clearing Counterparty (CCP) model, thereby improving the Payment Cycle (DvP) criterion.

Currently, Vietnam is classified as a frontier market by two international organizations, MSCI and FTSE Russell, and is included in their frontier market indices. To date, the Vietnamese stock market accounts for the largest proportion in the frontier market index basket (approximately 30% of total assets under management).

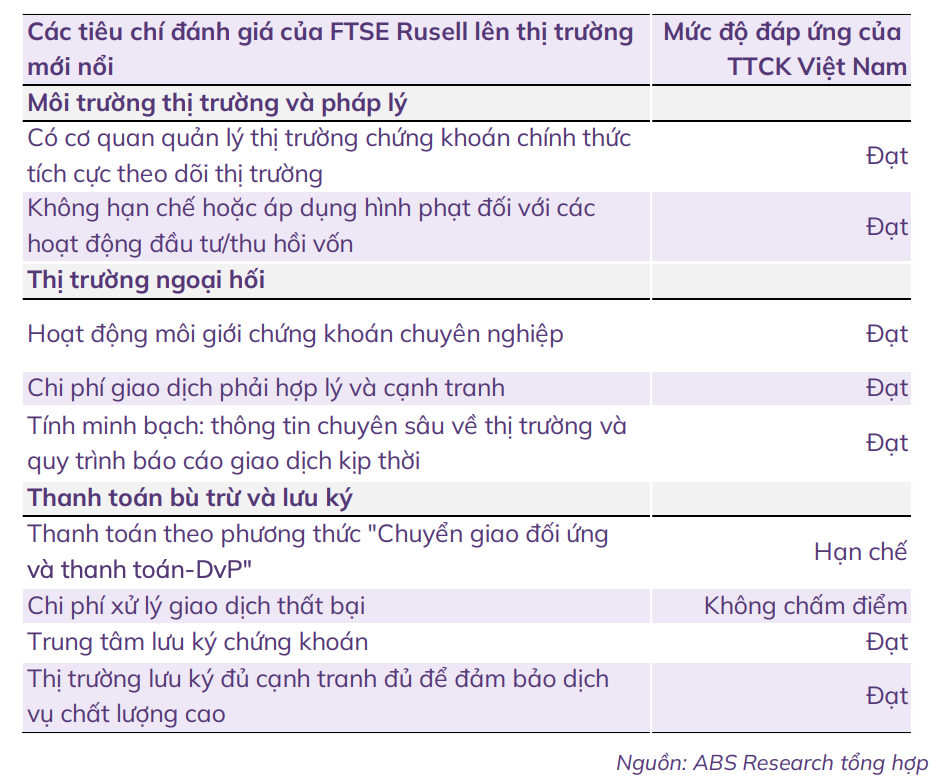

In the September 2024 review, the Vietnamese stock market met 7 out of 9 criteria necessary for an upgrade from frontier market to emerging market status, according to FTSE Russell's assessment.

|

| The extent to which the Vietnamese market meets FTSE's criteria for emerging markets. |

In the September 2024 assessment, based on MSCI criteria, Vietnam improved in one criterion compared to 2023, but still needs to improve in eight more criteria, including: foreign ownership limits, foreign room, equal rights for foreign investors, degree of freedom in the foreign exchange market; investor registration and account establishment, market regulations, information flow, and finally, clearing and settlement.

An Binh Securities (ABS) believes that the Vietnamese market could be upgraded by FTSE as early as the September 2025 review. "The key point is that the KRX trading system must become operational, laying the groundwork for the implementation of the Central Counterparty Clearing (CCP) model, which is a necessary condition for the market to be upgraded," ABS stated.

The system has been in preparation for several years, expected to shorten settlement times, provide many new conveniences, and facilitate the development of new products and services. The KRX system is the necessary infrastructure for deploying the Central Clearing Counterparty (CCP) model, thereby improving the Payment Cycle (DvP) criterion. However, to date, the KRX trading system has been continuously delayed due to incomplete development.

This system has repeatedly failed to meet its deadlines. Most recently, at the end of April 2024, the Ho Chi Minh City Stock Exchange (HoSE) announced to securities companies that the KRX system was preparing to operate from the beginning of May 2024 and requested them to check transactions on their systems against the new KRX system. However, shortly afterward, the State Securities Commission (SSC) sent a notice to the Stock Exchanges and the Vietnam Securities Depository and Clearing Corporation (VSDC) stating that it did not approve the application of KRX on May 2nd, 2024, as proposed by HoSE, citing non-compliance with legal regulations.

The early implementation of the new information technology system is also one of the key tasks of the securities industry in 2025, as directed by the leaders of the Ministry of Finance and the Vietnam Securities Commission.

In its analysis, ABS estimates that the Vietnamese stock market could immediately attract approximately $1.4 billion in passive investment funds such as ETFs (which currently invest in emerging markets), with Vietnam's upgrade automatically allocating some capital to this market. For active investment funds, improved market performance will make the Vietnamese stock market even more attractive.

Source: https://baodautu.vn/nang-hang-thi-truong-chung-khoan-mau-chot-la-he-thong-krx-d239183.html

Comment (0)