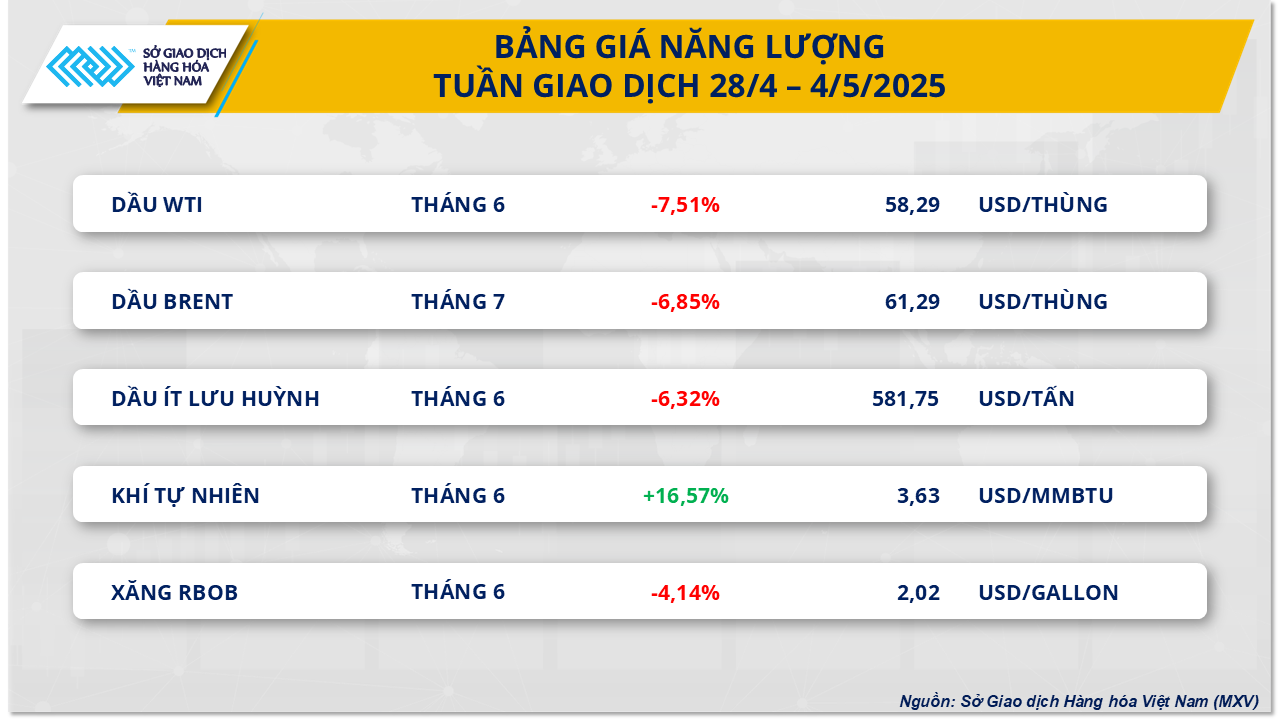

In the energy market, according to MXV, oil prices have just experienced their second consecutive week of decline in the context of the global market facing many uncertainties about supply, while investor sentiment is under pressure amid many concerns about the health of the world's number one economy .

Closing the week, Brent crude oil price stopped at 61.29 USD/barrel, down 6.85%. WTI crude oil also recorded a decline of 7.51%, falling below the 60 USD/barrel threshold and closing at 58.29 USD/barrel.

The downward pressure on prices mainly comes from speculation that OPEC+ will continue to increase production sharply in June, following the decision to increase production in May. This information appeared on April 23, causing Brent and WTI oil prices to fall sharply in the first three sessions of the week, with a decrease of 5.61% and 7.63%, respectively, in just three days from April 28 to April 30. This information became even more negative when some OPEC+ members continued to produce beyond their quotas, raising concerns about oversupply in the market. Notably, the meeting between the eight OPEC+ member countries was also moved up two days earlier than expected on May 3, making the market wait even longer for the June production decision.

In addition to supply factors, a series of negative macroeconomic data from the US also contributed to increasing pressure on oil prices. In the three days from April 29 to May 1, negative indicators were continuously announced, from the narrowing of the labor market, the decline in consumer confidence to the first decline in GDP in the first quarter of 2025 of the US in the past three years. Concerns about the US economic outlook led to doubts about future oil demand.

However, investors still have expectations about the possibility of reaching new trade agreements between the US and major partners, especially between the US and China. Last week, China announced that the US had approached the world's second largest economy about future negotiations; information that helped to restrain the decline in oil prices.

In addition, the decline in US crude oil reserves and the decline in oil exports from Venezuela also contributed to the support for oil prices. In addition, the unstable developments in the US-Iran relationship also made the market speculate about the prospect of no more supply from Iran, the main reason for the only price recovery session this week on International Labor Day, May 1.

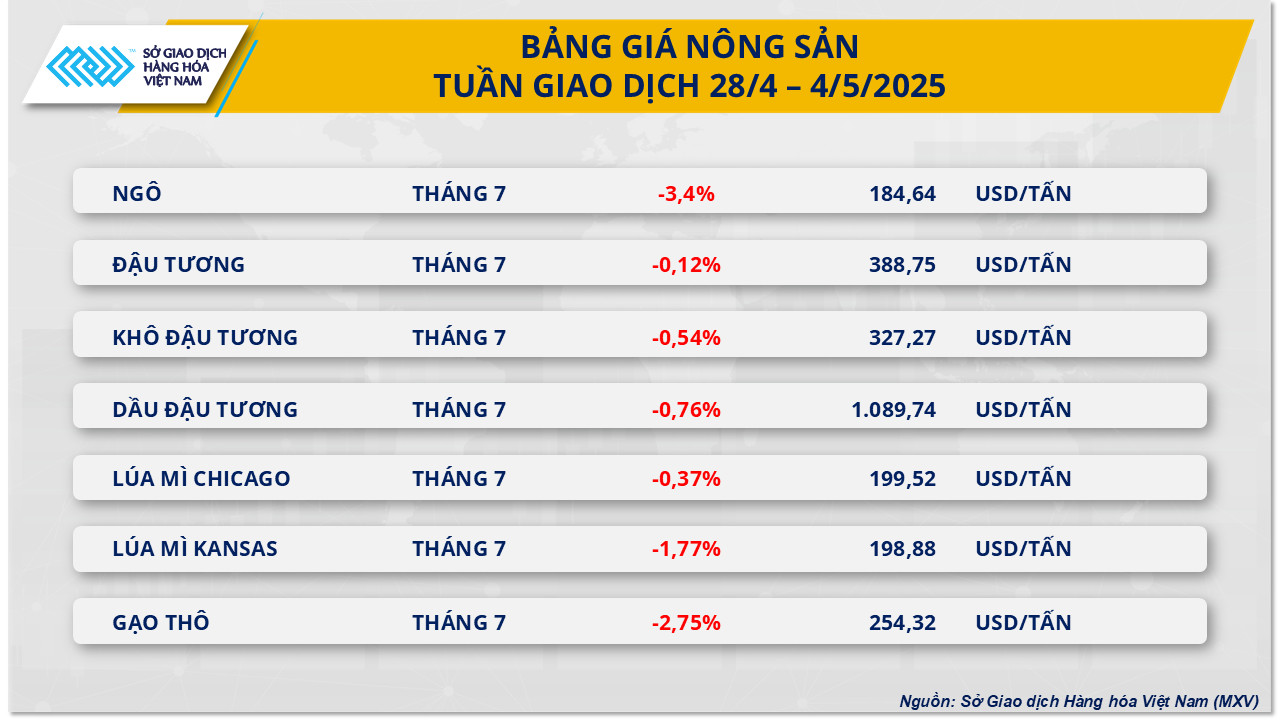

Regarding agricultural prices, the closing of the last trading week saw negative developments in the agricultural market as all 7 commodities in the group weakened. In particular, the corn and wheat markets both ended the trading week in the red, clearly reflecting the impact of supply and demand factors as well as technical developments.

Corn prices alone recorded their third consecutive weekly decline, losing about 3.4% to $184 per ton, while wheat prices fell slightly by 0.37% to $199 per ton thanks to strong recovery in the last sessions of the week.

The downward pressure on corn prices is both technical and psychological after the previous unsustainable rally. The latest Export Sales report shows that the US has sold only 1.01 million tons of corn for the 2024-2025 crop year, below the recent average. Despite the participation of many large customers such as South Korea, Vietnam, Israel and Mexico, demand is still not strong enough to create momentum for price increases. The news that Türkiye has opened a 1 million-ton duty-free import quota for corn is also only a slight support and has not had a clear impact on the market.

On the weather front, favorable planting conditions in the US, coupled with positive crop conditions in South America, have eased supply concerns, adding pressure to corn prices this week.

In wheat, the market recorded a strong technical recovery in the last three sessions of the week after falling into oversold territory. The July contract recovered significantly on the back of technical buying and some supportive fundamentals. Although crop conditions in France remained stable, localized drought in northern Europe and the UK raised yield concerns. In the US, spring wheat planting progress as of April 27 was only 30% of the expected area, lower than market expectations and compared to the same period last year, creating some concerns about this year's planting and supporting prices.

Source: https://baodaknong.vn/thi-truong-hang-hoa-5-5-sac-do-bao-trum-thi-truong-251509.html

![[Photo] French President Emmanuel Macron and his wife begin state visit to Vietnam](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/25/03b59c7613144a35ba0f241ded642a59)

![[Photo] Pink ball and table tennis](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/26/d9f770bdfda243eca9806ea3d42ab69b)

![[PHOTO] Hanoi fences off demolition of "Shark Jaws" building](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/25/1b42fe53b9574eb88f9eafd9642b5b45)

![[Photo] Ea Yieng commune settlement project abandoned](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/25/57a8177361c24ee9885b5de1b9990b0e)

![[Infographic] Vietnam-France Comprehensive Strategic Partnership](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/5/26/986f63068ea9413dbbb558ee6c6944f3)

Comment (0)