Retail space is still growing steadily

According to Savills' survey of leasing transactions in the last quarter, F&B tenants accounted for 37% of the total leased area, fashion industry accounted for 24% of the market share, and the remaining sectors such as health, beauty & entertainment accounted for 13% each.

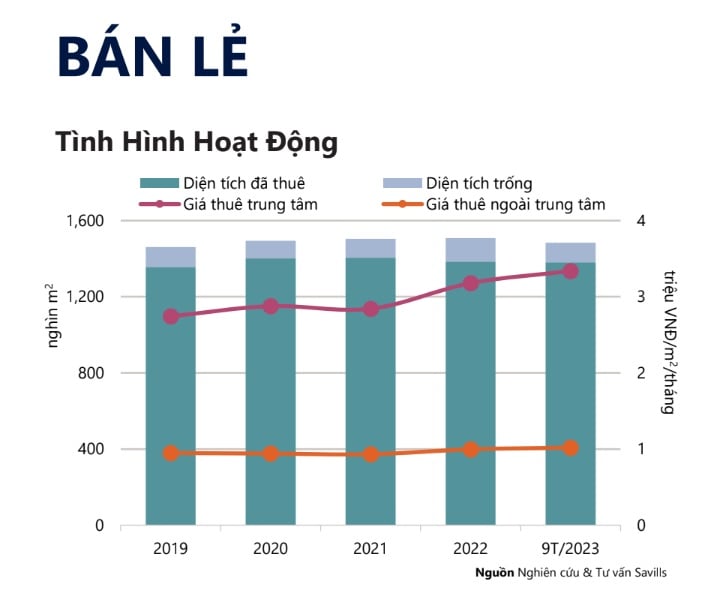

It is worth noting that the operating capacity of retail space in Ho Chi Minh City is very stable, maintained at 91% and unchanged quarterly.

The survey shows that most landlords in central areas are still confident with stable high rental prices at 3.3 million VND/m2/month, 3 times higher than in the suburbs. Rental prices in suburban areas also increased slightly by 1% quarter-on-quarter to 1 million VND/m2/month.

Retail space has grown steadily for many years.

Some typical leasing transactions for expansion purposes in non-central areas include Dragon Golf Land leasing 1,900m2 of floor space at Long Son building and Poseidon Company leasing 900m2 of floor space at Vincom Plaza Phan Van Tri project.

Savills data also shows that the retail podium segment is struggling. This is the segment with the strongest fluctuations in over the past decade. After peaking at 100% occupancy in 2010, rental capacity continued to decline by 2 percentage points in the last quarter, reaching 80%, while rental prices also decreased by 6% per year.

In the last quarter of the year, new supply is expected to be 82,227 square meters from four projects. In 2024, major projects such as Vivo City, Giga Mall and Vincom 3/2 also plan to renovate and change the tenant mix to refresh the retail cycle.

Office supply continues to increase

Also according to Savills research, in the third quarter of 2023, office supply for lease will grow by 3% quarterly and 4% annually after four new projects entered the market with more than 93,000 square meters of net leasable area.

In particular, the Thu Thiem new urban area dominates the new supply with 90% market share from two class A projects, The METT and The Hallmark. The occupancy rate of class A office space in this area is also at 50% with rental price of 1.2 million VND/m2/month.

Due to its proximity to the CBD and the high quality of new developments, the area has attracted tenants from the finance, banking, real estate (FIRE) and information and communications technology (ICT) sectors with the aim of expanding their scale. Notable tenants come from Australia, Korea, Taiwan, Malaysia and Vietnam.

Grade A office buildings in Thu Thiem are very well received.

As for the remaining 10% of new supply in the market, it is identified as belonging to two projects: The Waterfront Saigon, a class B project that has completed renovation, and L'MAK The Signature, a class C project that has just entered the market.

Commenting on the development of the office leasing sector, Ms. Giang Huynh, Head of Research & S22M, Savills HCMC said: “The good performance was driven by high demand for new Grade A projects. After many years of the market witnessing a scarcity of high-end supply, new supply has attracted companies in the FIRE sector”.

According to Savills' survey of transactions in the first 9 months of 2023, FIRE, ICT and Distribution accounted for the largest leased area. FIRE tenants accounted for 68% of the leased area with an average transaction area of 1,800 m2 NLA. Of which, in new projects, banking tenants accounted for 80% of the leased area.

Future supply is expected to come from six projects in the fourth quarter of 2023, providing 81,000 square meters of NLA. The Nexus and VP Bank Saigon Tower in District 1 are notable projects. Both are Grade A projects and are in the completion stage.

Hotels reduce capacity during low season

According to Savills data, the hotel market in Ho Chi Minh City remains stable on a quarterly and annual basis with 15,641 rooms from 109 hotels. Developers are also focusing on improving and enhancing the quality of their projects to maintain competitiveness as 100% of the closed rooms under renovation are expected to reopen in the near future.

In Q3/2023, hotel room occupancy reached 58%, down slightly by 2 percentage points quarter-on-quarter. Average room rates reached VND1.9 million/room/night, unchanged from the previous quarter.

Four- and five-star hotels also saw a 4% drop in occupancy rates quarter-on-quarter, down to 60%, due to the impact of the low-season market. For this type of hotel, the dependence on the peak season and the MICE customer base – a group of customers using high-end services – also slowed the recovery in the third quarter.

“The low season for MICE activities has posed a challenge for the hotel market in Ho Chi Minh City - a market that mainly depends on business travelers. Meanwhile, the number of international tourists has not yet returned to pre-pandemic levels,” explained Mr. Troy Griffiths, Deputy General Director, Savills Vietnam.

Mr. Troy Griffiths, Deputy General Director, Savills Vietnam

Despite year-on-year growth, the number of international visitors to Ho Chi Minh City only reached 57% compared to the first 9 months of 2019, lower than the national level of 70%.

However, according to Savills, from August 2023, Vietnam will allow citizens from all countries and territories to register for e-visas, increasing from 80 countries previously. At the same time, extending the stay to a maximum of 90 days with multiple entries. Savills assesses that this will be the main driving force to promote the recovery of this market.

Source

![[Photo] General Secretary To Lam receives Vice President of Luxshare-ICT Group (China)](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/15/1763211137119_a1-bnd-7809-8939-jpg.webp)

![[Photo] Prime Minister Pham Minh Chinh meets with representatives of outstanding teachers](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/15/1763215934276_dsc-0578-jpg.webp)

![[Photo] Panorama of the 2025 Community Action Awards Final Round](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/15/1763206932975_chi-7868-jpg.webp)

Comment (0)