Thanks to positive signals from tariff policies and flexible management measures of the State Bank of Vietnam (SBV), pressure on exchange rates is showing signs of cooling down. In that context, KBSV Securities forecasts that in the second half of 2025, the exchange rate may continue to move sideways and stabilize again, although there are still many potential risks that need to be monitored.

Pressure on USD/VND exchange rate temporarily eased thanks to more positive developments in tariff policy

According to KB Securities Vietnam (KBSV), the USD/VND exchange rate in the second quarter of 2025 recorded an increase in the range of 25,600 - 26,200 VND/USD (equivalent to +2.5% YTD), maintaining the upward momentum from the beginning of the year until now in the context of many fluctuations in the world economy . Although other currencies increased significantly, causing the DXY index to decrease by 11% in 6M2025, the VND had the opposite trend when it depreciated by more than 2% against the USD. The main reason comes from the Government's loosening of monetary policy and the risk of tariffs still existing, increasing the demand for foreign currency reserves in the country.

Faced with tense developments in exchange rates, the State Bank of Vietnam has taken flexible measures to manage exchange rates, including raising the central rate to over VND25,000/USD; regulating liquidity through the open market (OMO) to maintain the VND-USD interest rate gap at a reasonable level.

Information on tariff levels after recent negotiations shows that the 20% tariff that the US imposed on Vietnamese goods is relatively favorable compared to the previously announced 46% tariff. The interbank USD/VND exchange rate has decreased from the peak of 26,205 VND/USD but is still moving sideways around 26,129 VND/USD (+2.53% YTD).

KBSV believes that the reason comes from the fact that the market is still concerned about the potential risk of the 40% tax rate on "transit" goods when the definition of this type of goods does not have specific regulations.

Meanwhile, in the black market, the exchange rate also recorded an upward trend similar to the interbank exchange rate, even increasing more strongly at some points when the world gold price continued to set a new record above 3,400 USD/oz due to geopolitical issues in the Middle East. The domestic gold price also recorded a sharp increase, at times reaching over 124 million/tael, but the difference between domestic gold and international gold is still relatively large (over 10 million/tael). This indirectly puts pressure on the free market exchange rate when the demand for smuggled gold increases. As of now, the black market exchange rate is at 26,430 VND/USD (+2.2% YTD).

In that context, the State Bank has proposed a number of solutions to stabilize the gold market, including amending and supplementing Decree No. 24/2012 of the Government on the management of gold trading activities (expecting to end the state's monopoly on importing gold bars/raw materials); at the same time, directly intervening in selling gold. Thanks to that, the price difference between domestic and international SJC gold bars has initially narrowed, thereby reducing pressure on the exchange rate.

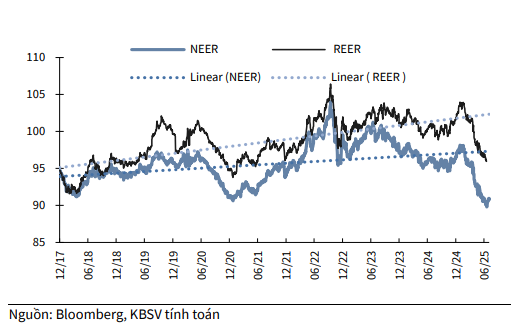

According to KBSV's calculation model, in the second quarter of 2025, NEER (the nominal multilateral exchange rate measuring the value of VND against a basket of 8 reference currencies according to the central exchange rate mechanism) continued to show a downward trend since the beginning of the year (-6.6% YTD). This reflects the relative depreciation of VND against the basket of key currencies for the reasons mentioned above.

The REER (the real exchange rate is an inflation-adjusted index compared to the NEER) also saw a similar decline (-6.5% YTD), indicating a slight improvement in the price competitiveness of Vietnamese goods amid a weakening domestic currency and domestic inflation being controlled below 4%.

Exchange rate pressure will increase at some point but will cool down towards the end of the year.

With the above analysis, KBSV maintains the forecast that the USD/VND exchange rate for the whole year of 2025 will still fluctuate within the allowable range of +4% compared to 2024 as mentioned throughout the previous reports. Although the exchange rate has shown signs of cooling down recently when the new tax rate announced for Vietnamese exports to the US is 20% instead of 46%, KBSV assesses that the exchange rate risk still needs to be monitored.

Accordingly, the clarity of specific regulations of tariff policy with Vietnam (especially the definition of transit goods); Vietnam's reciprocal tax rate compared to other countries; and the fluctuation trend of the DXY index will be important factors determining exchange rate movements in the coming time.

Factors related to tax rates affect foreign currency inflows into Vietnam from export channels and foreign direct investment (FDI). The current 20% reciprocal tax rate for Vietnam is relatively favorable compared to other countries (China, Japan, Thailand, Bangladesh, etc.), but the final tax rate decision applicable to US partners will not be announced until August 1.

KBSV believes that the reciprocal tax difference (20%) between Vietnam and other countries will not be too significant. KBSV is more cautious with the figure of 40% for transit goods when the definition of “transit” goods is still unclear.

According to some FTA agreements that the US has signed with other countries, the US defines transit goods as goods with a localization rate of <_3525_. _ne1babf_u="" quy="" _c491_e1bb8b_nh="" _ve1bb81_="" _te1bbb7_="" _le1bb87_="" _ne1bb99_i="" _c491_e1bb8b_a="" _cc3a0_ng="" cao="" _thc3ac_="" _e1baa3_nh="" _hc6b0_e1bb9f_ng="" _tic3aa_u="" _ce1bbb1_c="" _ve1bb9b_i="" _vie1bb87_t="" nam="" _se1babd_="" gia="" _tc483_ng="" _vc3a0_="" _ngc6b0_e1bba3_c="" _le1baa1_i.="" _dc3b9_="" _ve1baad_y2c_="" _vie1bb87_c="" so="" _sc3a1_nh="" _cc3a1_c="" _que1bb91_c="" _c491_e1bb91_i="" _the1bba7_="" _lc3a0_="" quan="" _tre1bb8d_ng2c_="" _c491_c6b0_e1bba3_c="" _c3a1_p="" common="" cho="" _te1baa5_t="" _ce1baa3_="" _nc6b0_e1bb9b_c2c_="" _hoe1bab7_c="" _me1bba9_c="" _chc3aa_nh="" _nc3a0_y="" _khc3b4_ng="" _quc3a1_="" _c491_c3a1_ng="" _ke1bb83_="" _tc3a1_c="" _c491_e1bb99_ng="" _gie1baa3_m="">

In the short term, KBSV believes that the exchange rate may remain tense at some points in the third quarter when the export promotion during the tax deferral period (Q2 export turnover +20% YoY), while the PMI index below 50 in the last 3 months will put pressure on growth in the third quarter due to the lack of orders; the season when businesses transfer profits back home; the new disbursed FDI flow may slow down if the tariff outlook after August 1 is not as expected.

However, the USD/VND exchange rate is expected to cool down towards the end of the year thanks to the recovery of export activities during the peak season; remittances to the country; the weakening of the USD in the context of the US applying Trump's One Big Beautiful Bill Act policy and the expectation that the Fed will cut interest rates twice this year. Pressure on the exchange rate is still a factor that needs to be closely monitored in the coming months, especially when tariff policies are announced to apply to Vietnam and other countries.

With the forecast that the USD/VND exchange rate will increase by no more than 4% this year, KBSV believes that the SBV will continue to have flexible management measures so that the exchange rate fluctuates within the allowed range, creating favorable conditions for implementing a loosening policy to promote growth. Although in 6M2025, the exchange rate recorded tension at some points, the SBV has intervened promptly, including raising the central exchange rate; regulating the open market, maintaining the USD-VND interest rate gap at a reasonable level. In the second half of 2025, it is likely that these tools will continue to be used to stabilize the exchange rate, while the possibility of increasing the operating interest rate this year is relatively low. In general, KBSV still maintains the view that the SBV's monetary policy orientation in the coming time will continue to support growth, but will respond flexibly to economic shocks.

Source: https://baolamdong.vn/nhieu-kha-nang-ty-gia-se-ha-nhiet-vao-cuoi-nam-383532.html

![[Photo] National Assembly Chairman attends the seminar "Building and operating an international financial center and recommendations for Vietnam"](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/7/28/76393436936e457db31ec84433289f72)

Comment (0)