Need more attraction to bring foreign investors back

SSI Research's report on investment cash flow into the Vietnamese stock market said that ETF funds continued to maintain a net withdrawal status in February and increased in intensity compared to the previous month.

The net withdrawal value was recorded at -1,155.7 billion VND, the accumulated value in the first 2 months of 2025 was -1,771.8 billion VND, equivalent to 3% of total assets of ETF funds at the end of 2024, bringing the total assets of ETF funds to 56,900 billion VND. However, the withdrawal value in the first 2 months of 2025 was still 34.5% lower than the same period in 2024.

Some foreign funds have reduced their net withdrawals. Specifically, VanEck Vietnam ETF (-VND264 billion) significantly reduced its net withdrawals compared to the previous 3 months, or Xtrackers FTSE Vietnam Swap UCITS ETF (-VND6.3 billion) only had a slight net withdrawal. Fubon fund alone slightly increased its net withdrawal value to -VND254.9 billion in February.

Domestic funds recorded a slowdown in net buying, with some funds switching to net selling. DCVFMVN30 ETF (-433 billion VND) recorded its fourth consecutive month of net withdrawal, DCVFMVN Diamond ETF (-190 billion VND) reversed to net selling, after 2 previous months of net inflows.

Cash flow from active funds all recorded net withdrawals in February. Active funds investing only in Vietnam and multinational investment funds withdrew net VND826 billion and VND787 billion, respectively. Accumulated in the first two months of 2025, active funds investing only in Vietnam withdrew VND1,658 billion.

The proportion of foreign investors owning in the Vietnamese stock market is currently only 13.1%, the lowest level since 2015, and the weakening of DXY will limit net selling pressure from foreign investors in the coming period. However, SSI believes that global investment capital flows are still prioritizing developed markets and the Vietnamese stock market needs more specific market development measures to attract foreign investors to return.

The current market trend is stable and is expected to attract stronger cash flow from domestic investors, coming from the rapid cash flow between industry groups, low valuations, along with the Government 's strong economic growth orientation and individual stories, typically the story of imposing defense tariffs on the steel industry, legal solutions for some residential real estate projects , expectations for the implementation of the KRX system, or the Draft Law amending and supplementing a number of articles of the Law on Credit Institutions...

Stocks will continue to rise

Vietnam's stock market has increased completely in February 2025. The VN-Index closed at 1,305.4 points on February 28, up more than 40 points (+3.2%) compared to the previous month and up 3.1% since the beginning of the year. The Vietnamese market is performing positively thanks to a stable macro foundation with the Government's target of 8% GDP growth and 16% credit growth in 2025, along with expectations of market upgrade.

More optimistic investor sentiment has led to more money entering the market than in the previous period. The average matched liquidity on the HoSE floor increased to VND14,300 billion/session, the highest level in 6 months. Stronger money flow is participating across the board, especially in large-cap industries such as banking , steel, real estate and food and beverage, creating the main driving force for the general market to rise.

In this context, SSIResearch said it continues to see factors that continue to push the Vietnamese stock market to continue to rise, although there may be risks of short-term correction.

Factors that continue to drive the index are attractive valuations, upgrade prospects and government growth support measures.

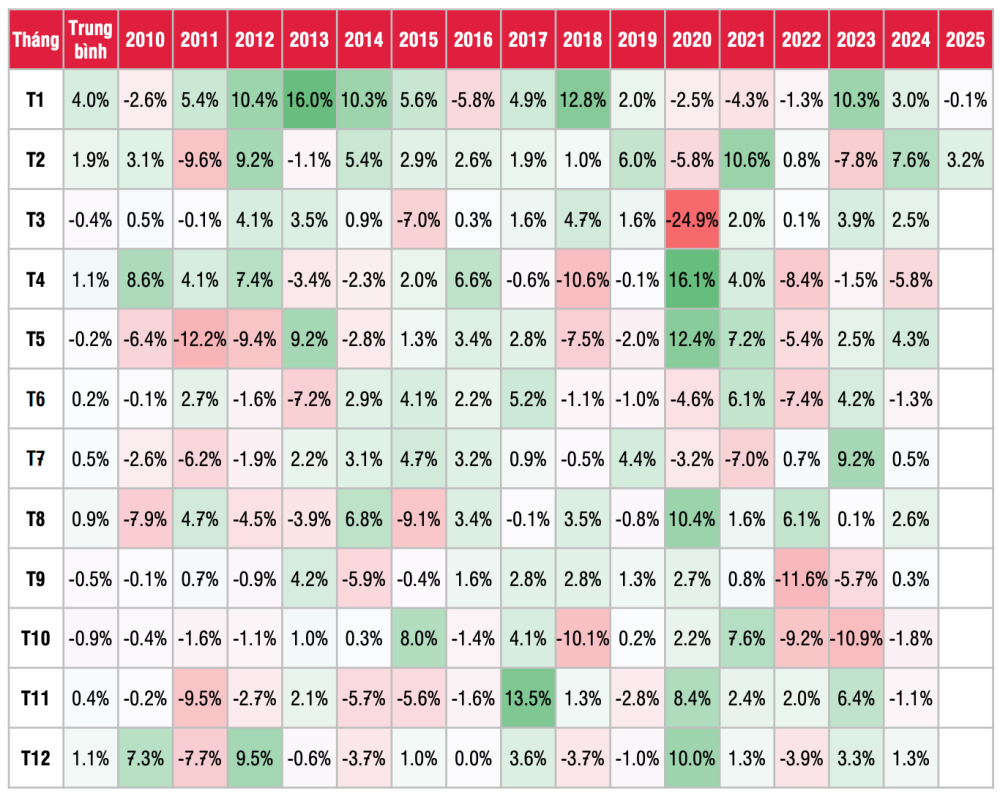

Historical data over 15 years shows that the stock market's movement trend in March was positive with 12 increases. The market challenged the 1,300 mark on VN-Index data from the last week of February with the valuation ratio of the most recent 4-quarter trailing P/E and estimated 1-year P/E of 14x and 10.3x, respectively; significantly lower than previous challenges in the 2020-2024 period.

|

| Historical data on monthly stock market trends. Source: SSI Research |

The Government's monetary policy direction continues to lean towards supporting the economy . There is a tariff risk for Vietnam, but it is lower than other countries. Currently, the long-term story of the market will focus on the Government's reform process starting from the end of 2024.

Regarding capital flows, we continue to expect a more prosperous foreign capital flow in 2025 thanks to the prospect of upgrading to emerging market status by FTSE Russell, stepping-stone policies such as implementing the KRX trading system, applying the amended Securities Law and the amended Decree 155/2020/ND-CP.

In the period when the market is improving in liquidity, SSI believes that the trading strategy at this time should focus on industries that strongly attract cash flow such as banking, securities, real estate; in addition to industries that benefit from the Government's growth orientation such as construction - building materials, retail.

Regarding technical signals, SSI expects the short-term uptrend of VN-Index to continue in the coming time. The target is towards the resistance zone of 1,320 - 1,330 points. If it is successful, the VN-Index will continue to move up to challenge the 1,360 point zone.

Source: https://baodautu.vn/nhieu-tro-luc-vung-chac-chung-khoan-viet-nam-se-tiep-tuc-di-len-d251459.html

![[OCOP REVIEW] Tu Duyen Syrup - The essence of herbs from the mountains and forests of Nhu Thanh](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/6/5/58ca32fce4ec44039e444fbfae7e75ec)

Comment (0)