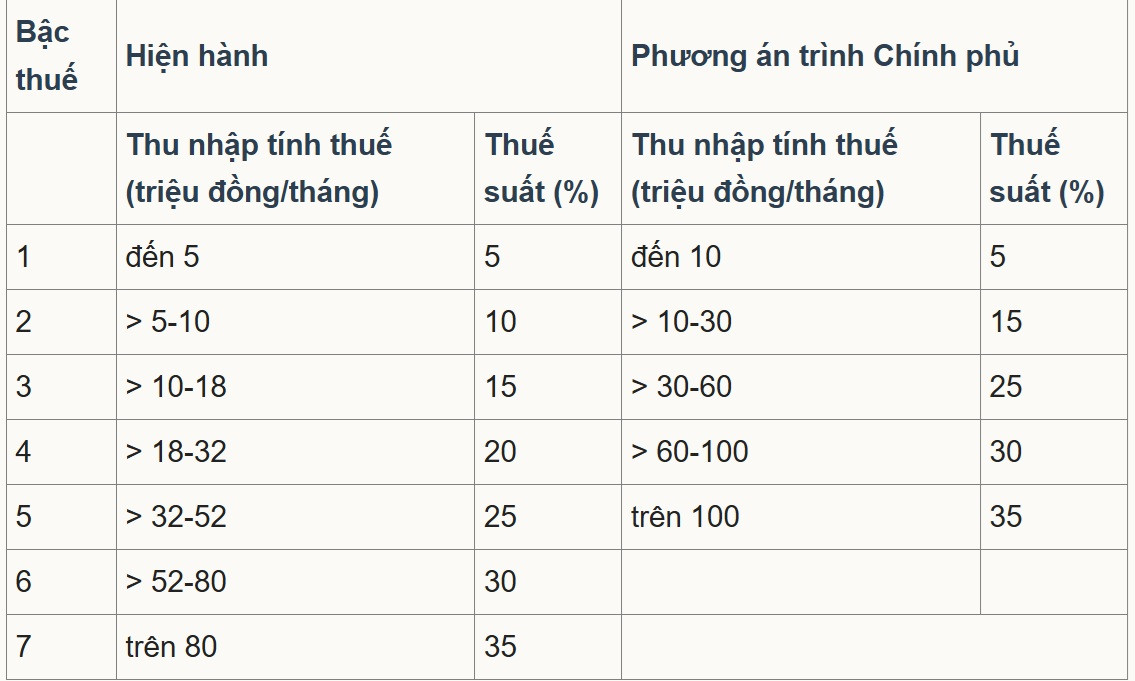

According to the Ministry of Finance , the draft Law on Personal Income Tax (amended) has adjusted the progressive tax schedule - one of the basic and core contents.

Specifically, the draft law restructures the "partially progressive tax schedule applicable to income from salaries and wages", simplifies the tax schedule and regulates income to suit the socio -economic situation in the direction of reducing the number of tax rates from 7 to 5 and widening the gap between the rates, corresponding to tax rates of 5%, 15%, 25%, 30%, 35%.

In the two proposed options, the majority of opinions agreed with option 2 and the Government submitted this option to the National Assembly . Accordingly, the gap between tax brackets is widened and gradually increased to 10, 20, 30, 40 million VND; the lowest tax bracket remains at 5% and the last tax bracket is 35%, applied to taxable income over 100 million VND/month.

Sharing with VietNamNet reporter, Dr. Nguyen Ngoc Tu, lecturer at Hanoi University of Business and Technology, said that reducing the number of levels from 7 to 5 to make the tax system simpler is appropriate. However, the proposed tax threshold of 10 million VND for level 1 is too low, it needs to be raised to 30 million VND to be subject to 5% tax.

“The final tax threshold raised from over 80 million VND to over 100 million VND subject to a tax rate of 35% is not consistent with other targets,” he said.

Mr. Tu analyzed that from 2007 to now, after 18 years, prices have increased about 2.5 times, GDP scale and per capita income have also increased 2.5-3 times. Therefore, the tax threshold also needs to be adjusted to at least 2.5 times, equivalent to 200 million VND to be taxed at 35%.

“The Ministry of Finance will maintain the highest tax rate at 35%, while corporate income tax will be reduced from 25% to 15-17%. Personal income tax should be adjusted to a maximum of 25% or 30% to attract high-quality human resources and foreign experts,” he proposed.

Mr. Tu emphasized: “The soul of each tax is the tax rate and the tax schedule. If there is a revision, the tax rate must be lowered, and the tax threshold must be adjusted upwards to make sense. Just changing the wording, while the tax rate does not decrease and the tax threshold increases insignificantly, cannot be considered a comprehensive revision.”

He also said that the gap between tax rates 1, 2 and 3 is too wide, each rate should only be 5% apart to be reasonable. According to him, between rates 1, 2 and 3, the tax rate should only increase by 5%, but according to the current plan, it increases from 5% to 15% and from 15% to 25% (ie 10% between rates). Meanwhile, those with high incomes in rates 4 and 5 only increase by 5% each rate.

"This design goes against the spirit of the progressive tax schedule. People with just enough income should enjoy a low tax rate; while people with higher incomes should have a higher tax rate and a higher rate of tax escalation," Mr. Tu analyzed.

Meanwhile, Associate Professor Dr. Pham Manh Hung, Deputy Director of the Institute of Banking Science Research, Banking Academy, also assessed that reducing the number of levels from 7 to 5 helps simplify the tax system, while reducing the "jump" at the middle thresholds.

The threshold for the highest tax rate has also been raised from over VND80 million to VND100 million/month, meaning that only the very high income group will be subject to the 35% rate. This is considered an improvement friendly to investors and skilled workers, as the number of people falling into the highest tax bracket has been reduced.

However, Mr. Hung said that the 35% ceiling is still significantly higher than that of competitive human resource centers such as Singapore (the highest is 24% for residents, with many incentives and deductions). This could affect the ability to retain high-level human resources and international experts.

The expert suggested that the 35% tax threshold could be raised above VND100 million or targeted deduction and incentive policies (R&D, technology experts, green finance) could be expanded to increase Vietnam's competitiveness compared to regional centers.

Source: https://vietnamnet.vn/sua-thue-thu-nhap-ca-nhan-muc-10-trieu-dong-cho-bac-1-la-qua-thap-2460607.html

![[Photo] Heavy damage after storm No. 13 in Song Cau ward, Dak Lak province](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/08/1762574759594_img-0541-7441-jpg.webp)

![[Video] Hue Monuments reopen to welcome visitors](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/11/05/1762301089171_dung01-05-43-09still013-jpg.webp)

Comment (0)