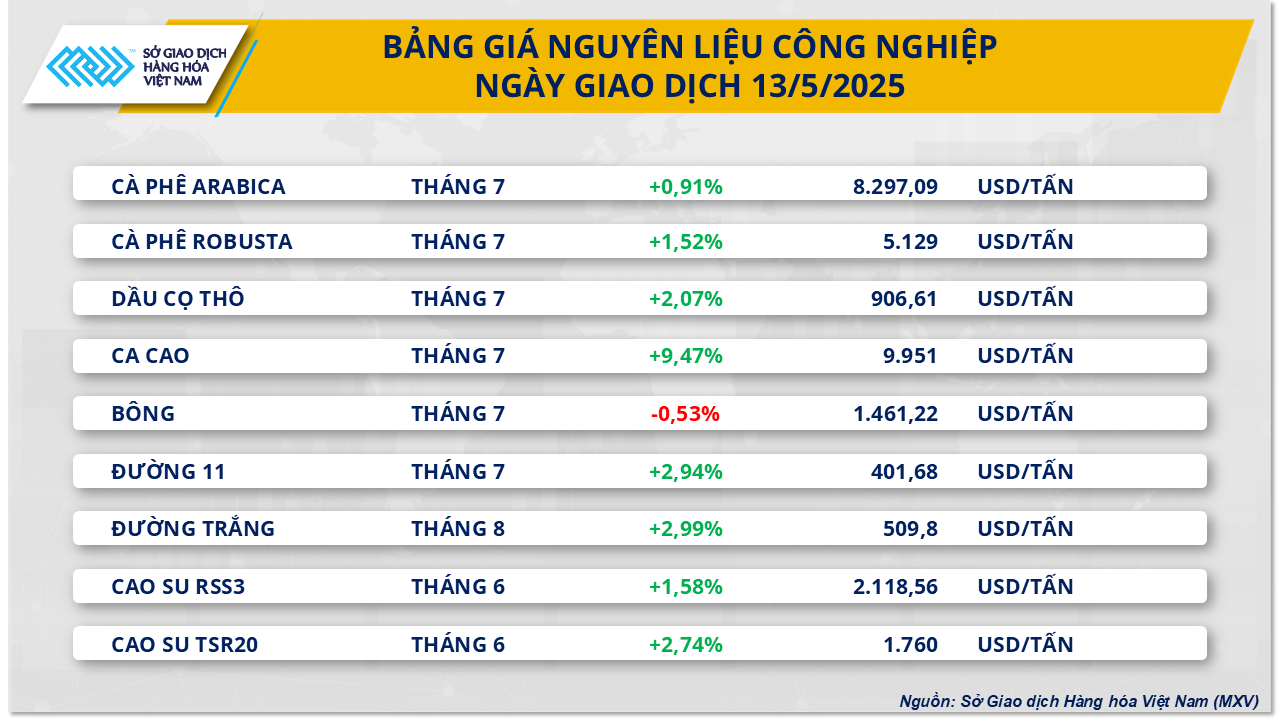

Regarding the industrial raw material group, at the end of yesterday's trading session, the industrial raw material market recorded positive developments when 9 out of 10 items increased in price. In particular, world sugar prices increased sharply on both major exchanges. Sugar price 11 on the ICE US exchange increased by 2.94% to 401 USD/ton, while sugar price on the ICE EU exchange also increased by 2.99% to 509.8 USD/ton. The increase in sugar prices was recorded in the context of global supply continuing to be under pressure.

The latest report from UNICA said that sugarcane crushing output in the Center-South region of Brazil in April reached only 34.25 million tons, down 33% compared to the same period last year, while sugar production also decreased by 39% to 1.58 million tons due to heavy rains that slowed down the harvest and reduced the sugar content in the cane.

In addition, according to statistics from the Brazilian government , sugar exports in April continued to decline by 17.7% compared to the same period last year, reaching only 1.55 million tons. In the first four months of the year, the country's sugar exports decreased by 32.3% compared to the same period last year. This has raised concerns about supply shortages, thereby supporting sugar prices to skyrocket in yesterday's trading session.

Also yesterday, the US Department of Agriculture (USDA) announced its latest forecast for US sugar production for the 2025-2026 crop year, estimated at 8.42 million tons, down slightly from 8.454 million tons in the 2024-2025 crop year. Notably, sugar beet production is forecast to drop to 5.2 million tons, compared to 5.33 million tons last year. In contrast, sugar cane production is expected to increase to 4.1 million tons, up from 3.97 million tons in the previous crop year.

On the import side, USDA forecasts that this figure will decrease to 2.5 million tons in 2025-26, compared to 2.94 million tons in the previous year. Deliveries (domestic consumption) are expected to remain unchanged at 12.25 million tons. With the above factors, ending inventories are expected to decline sharply to 1.4 million tons, significantly lower than the 2 million tons in 2024-25.

In the coffee market, the prices of two coffee products recovered simultaneously in yesterday's session. Arabica coffee prices increased by 0.91% to 8,297 USD/ton, while Robusta coffee prices increased by 1.52% to 5,129 USD/ton. According to the latest report from the Brazilian Coffee Export Council (Cecafé), Brazil's coffee exports decreased by 27.7% in April compared to April 2024, reaching 3.09 million bags (60 kg each). However, export revenue increased sharply by 41.8% over the same period, reaching 1.34 billion USD. In the first four months of the year, coffee exports decreased by 15.5% over the same period, but the turnover reached a record high of 5.23 billion USD.

Cecafé President Márcio Ferreira said the drop in exports was justified given the mid-season period, especially after Brazil exported a record amount in 2024. He added that exports would slow in the next two months, until the Arabica crop begins. Brazil is likely to harvest its largest Robusta crop in history, while production in Vietnam and Indonesia is also expected to grow compared to last year.

In addition, dry and warm weather is forecast to dominate Brazil's coffee growing regions over the next 10 days, which could affect the harvest progress and quality of the new crop.

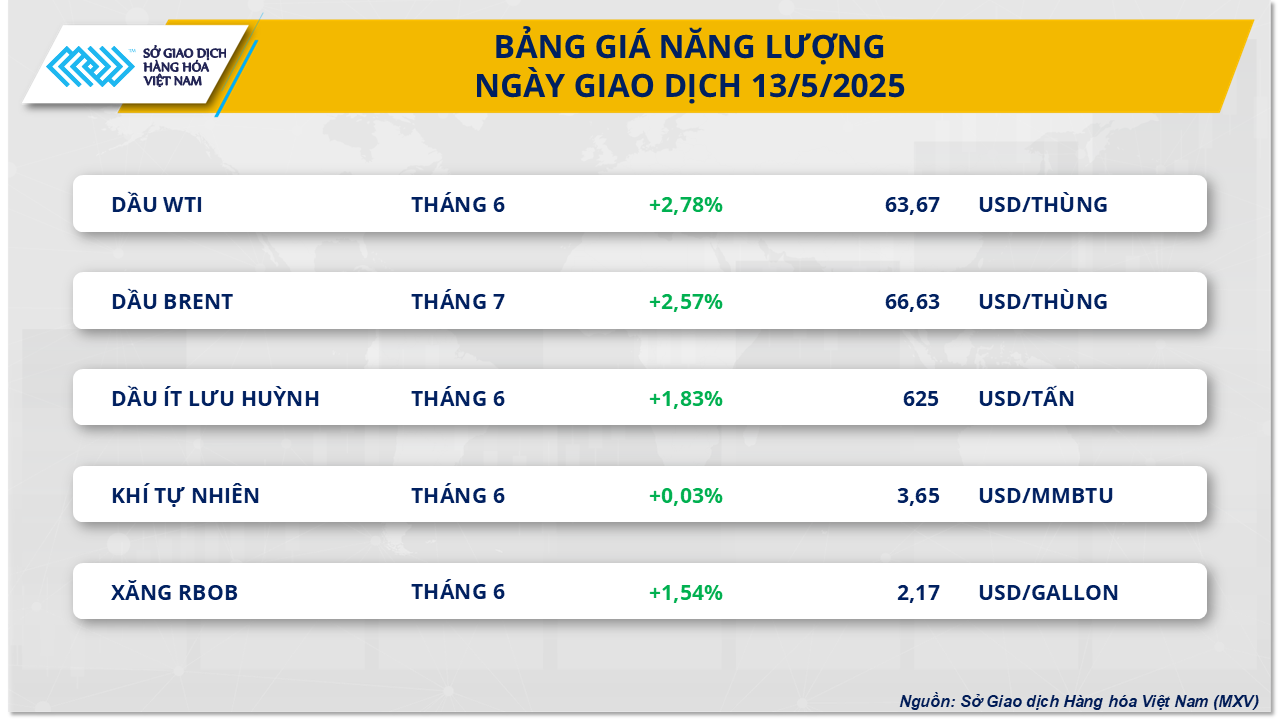

In the energy market, the optimistic sentiment continued to be maintained in the energy market after the interim trade agreement between the US and China. This supported the strong increase in world oil prices in yesterday's session.

At the end of the trading session, Brent oil price stopped at 66.63 USD/barrel, up 2.57%. Similarly, WTI oil price also recorded an increase of up to 2.78%, up to 63.67 USD/barrel. These are the two highest price levels of these two commodities since the end of April.

Overall, the optimistic sentiment in the market was mainly reinforced by the agreement reached on May 10 between the US and China. Although it is only a temporary agreement within 90 days, after a long period of "confrontation" between the two countries, this move is considered a positive signal, especially for US importers, when the demand for imported goods from China is forecast to increase sharply in the next 3 months, leading to an increase in demand for crude oil and fuel.

In addition to the impact of the US-China agreement, the latest inflation figures in the US also contribute to reinforcing a more positive macroeconomic outlook in the world's two largest oil consuming countries. According to the US Bureau of Labor Statistics, the consumer price index (CPI) in April increased by only 0.2% compared to the previous month and 2.3% compared to the same period last year - the lowest level since March 2021; Core CPI also increased by only 2.8%. These data show that inflation in the US is not as worrying as many previous forecasts, thereby creating speculation about the possibility of a decision to cut interest rates by the US Federal Reserve (FED).

US President Donald Trump did not miss the opportunity, continuing to put pressure on FED Chairman Jerome Powell through a post on the social network Truth Social, asking the Federal Open Market Committee (FOMC) of the FED to make a decision to cut interest rates. The relatively high interest rate of 4.5% currently in effect is helping the FED control inflation but is also a major obstacle to economic development. The upcoming decision of the FOMC on interest rates is expected to be made on June 19; however, the possibility of a decision to cut interest rates is still open because the inflation target set by the FED is 2%, which is still lower than the latest increase in the CPI index.

Source: https://baodaknong.vn/thi-truong-hang-hoa-14-5-sac-xanh-bao-phu-thi-truong-252494.html

![[Photo] Prime Minister Pham Minh Chinh receives Rabbi Yoav Ben Tzur, Israeli Minister of Labor](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/511bf6664512413ca5a275cbf3fb2f65)

![[Photo] Prime Minister Pham Minh Chinh attends the groundbreaking ceremony of Trump International Hung Yen Project](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/ca84b87a74da4cddb2992a86966284cf)

![[Photo] Determining the pairs in the team semi-finals of the National Table Tennis Championship of Nhan Dan Newspaper](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/eacbf7ae6a59497e9ae5da8e63d227bf)

Comment (0)