The Vietnam Commodity Exchange (MXV) said that cautious sentiment continued to dominate the world raw material market in the past trading week (July 21-27). Before the US applied new tariff policies, concerns about increasing global trade tensions led to strong fluctuations in the prices of many commodities.

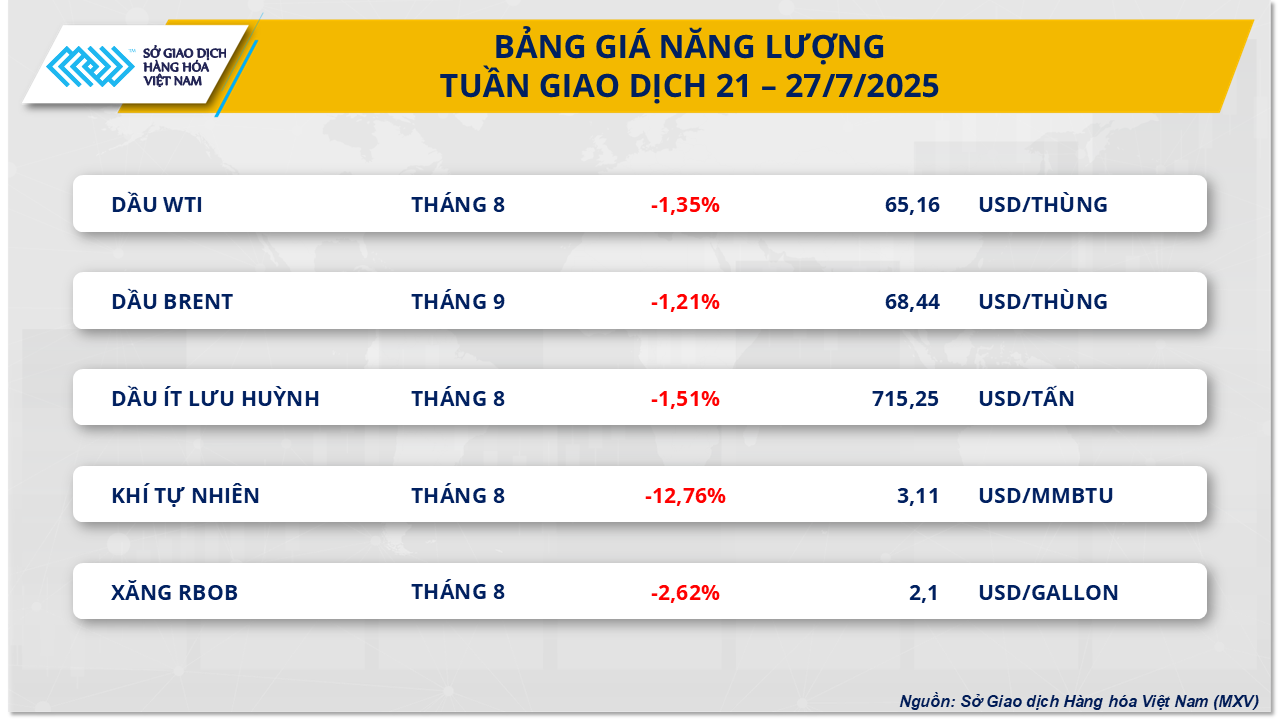

In the energy market, according to MXV, the energy market last week witnessed overwhelming selling pressure across all five commodities in the group. At the end of the trading session on July 25, WTI oil prices recorded a weekly decrease of about 1.35%, falling to 65.16 USD/barrel, the lowest level since early July. Brent oil prices also stopped at the lowest level in nearly three weeks, 68.44 USD/barrel, corresponding to a decrease of 1.21%.

Over the past week, the focus of market concerns continued to be on global trade tensions, as the US has yet to reach a new trade agreement with key partners such as the EU and China, as the August 1 deadline approaches. This development has increased concerns about the risk of a global economic slowdown, while also making the outlook for energy consumption less positive.

On the supply side, pressure on oil prices continues to be present as Saudi Arabia and Kazakhstan, members of the OPEC+ group, have simultaneously boosted exports, significantly increasing supply to the market. In addition, the market is also focusing on OPEC+'s September production decision, with most forecasts leaning towards the possibility that the group will continue to increase production, continuing the trend of increasing supply that has appeared in previous months.

Meanwhile, positive information on energy demand in the US has helped to curb the decline in oil prices last week. Both the labor market and PMI index groups were relatively positive for the world's largest economy, thereby supporting the prospect of increasing energy demand. In addition, data from the US Energy Information Administration (EIA)'s weekly report also showed that crude oil inventories continued to decline sharply, indicating an increase in demand for gasoline by Americans.

This week, the market is particularly focused on the Federal Open Market Committee (FOMC)’s decision on the base interest rate. According to experts, the possibility of the FED cutting interest rates from 4.25–4.5% is not high, due to concerns about the risk of re-emerging inflation, causing most forecasts to lean towards the scenario of keeping interest rates unchanged. However, the FED is still under great pressure from the Trump administration with proposals to sharply cut interest rates to boost short-term economic growth – a factor that could create more waves in the financial and energy markets.

For the domestic market, the retail price of gasoline and oil has been adjusted down slightly by the Ministry of Industry and Trade and the Ministry of Finance, in line with world oil prices. On the afternoon of July 24, the prices of three out of five items were adjusted down; notably, the two gasoline items were adjusted by more than 1% while the price of diesel oil was adjusted in the opposite direction. During the recent adjustment period, the Ministry continued not to make any provision or use the Petroleum Price Stabilization Fund.

In another development, natural gas prices in the US market recorded a sharp decline last week. At the end of the trading session on July 25, natural gas prices traded on the NYMEX stopped at 3.11 USD/MMBtu, corresponding to a decrease of nearly 12.8% compared to the beginning of the month. The main reason comes from forecasts of prolonged cool weather in many areas in the US this week, increasing concerns about electricity demand - especially for gas power plants that often increase capacity in peak hot weather conditions. Along with that, the latest report from the US Energy Information Administration (EIA) recorded that natural gas inventories continued to increase sharply in July, leading to significant downward pressure on prices of this commodity in the US domestic market.

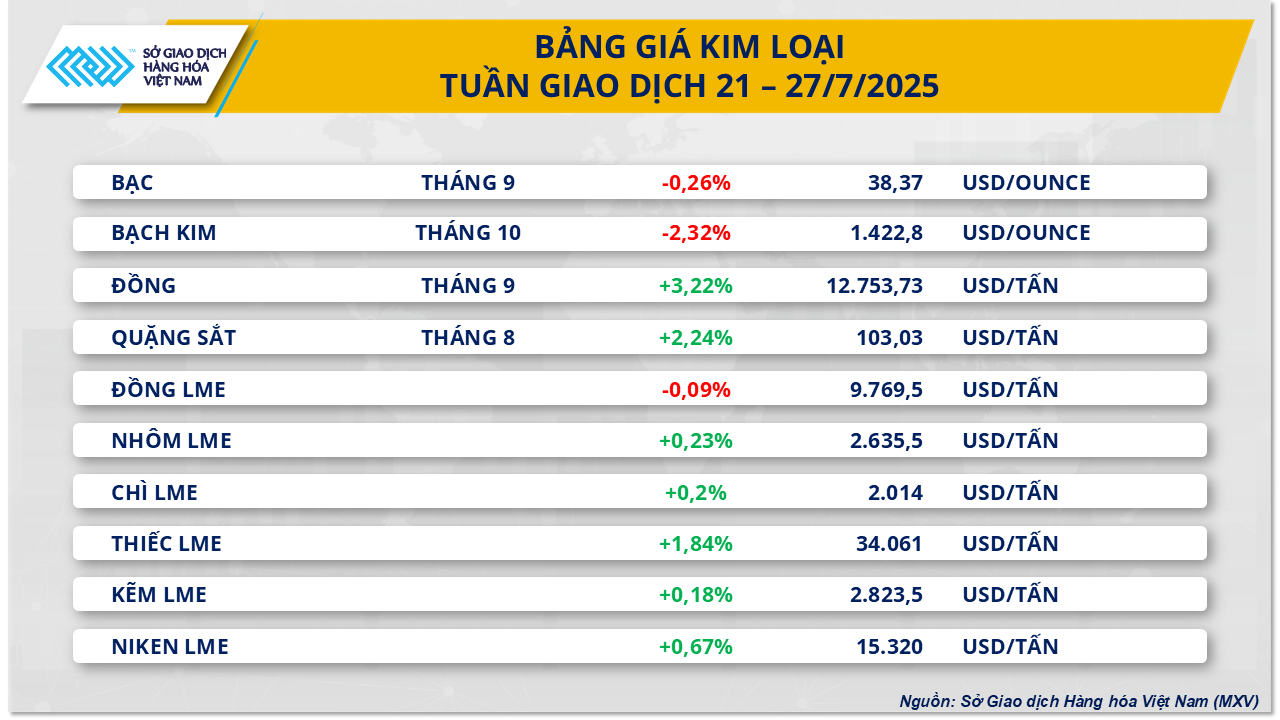

For the metal market, the last trading week ended with mixed developments. Notably, at the end of the trading session on July 25, the price of iron ore futures for August recorded a weekly increase of 2.24%, reaching 103.03 USD/ton, marking the 5th consecutive week of increase.

Over the past week, iron ore prices have risen to their highest level since late February, mainly due to the news that China has started construction on the lower Yarlung Zangbo River hydropower project in Tibet – a project considered the “project of the century” with a total investment of up to 167–170 billion USD. According to analysts, this project alone is expected to consume about 2–2.5 million tons of steel, equivalent to nearly 3% of China’s average monthly crude steel output, thereby creating a significant driving force for the demand for input materials such as iron ore in the coming period.

Citigroup’s assessment shows that if construction progress is maintained for 10 years, the project will not only boost steel and iron ore consumption but also contribute up to 120 billion yuan (about 16.7 billion USD) to China’s GDP each year, with the actual economic benefits potential being much higher than the initial estimate. This is a clear signal of the Chinese government’s determination to use large-scale infrastructure investment to support economic growth targets, especially in the context of the domestic real estate market that has yet to show signs of a stable recovery.

This groundbreaking move has thus contributed to alleviating market concerns regarding the prospects for steel and iron ore demand in the medium and long term, helping to create a supportive foundation for the raw materials market in the coming years.

On the contrary, the increase in iron ore prices last week was restrained when the market received more negative information about the actual consumption situation.

According to data from SMM Metals Market Analysis, as of July 23, the blast furnace operating rate at 242 surveyed Chinese steel mills fell 0.11 percentage points from the previous week to 86.9%. The capacity utilization rate also fell slightly to 89.57%, pulling the average daily hot pig iron output down 2,100 tons to 2.4 million tons.

On the supply side, iron ore prices are also under pressure from a sharp increase in exports. According to data from the Pilbara Port Authority (Australia), at the world's largest iron ore export port, Port Hedland, exports in June reached a record high of 54.6 million tonnes, up 2.8% compared to May. Of which, exports to China alone increased by more than 8% to 49.2 million tonnes. At the port of Dampier, Australia's third largest iron ore export port, exports in June also increased by 4.8% to nearly 13 million tonnes.

Source: https://baolamdong.vn/thi-truong-hang-hoa-28-7-gia-nhieu-mat-hang-bien-dong-manh-384055.html

![[Photo] National Assembly Chairman attends the seminar "Building and operating an international financial center and recommendations for Vietnam"](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/7/28/76393436936e457db31ec84433289f72)

Comment (0)