Profit rate is only 1.97%, almost "bottom" of the banking industry

In the first quarter of 2025, ABBank recorded net interest income of VND832 billion, up 25.9% over the same period last year. Net profit from service activities also increased by nearly 60%, reaching VND162 billion. Notably, the loss from trading investment securities decreased from negative VND45 billion to just over VND5 billion.

However, the cost of credit risk provisioning during the period nearly doubled, from VND177 billion to VND340 billion. This shows that the bank is having to set aside large provisioning costs due to increased risks from credit loans, meaning that asset quality is seriously deteriorating. The cost of credit risk provisioning has significantly eroded the bank's profits.

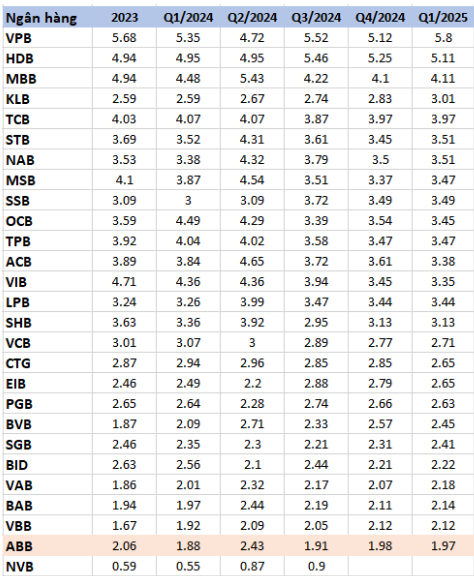

As a result, ABBank recorded a profit after tax of VND 333 billion, more than double the VND 154 billion in the same period last year. Although profit increased, the NIM (Net Interest Margin) in Q1/2025 was only 1.97%, slightly down from 1.98% in Q4/2024.

This ratio reflects the bank's ability to generate net interest income from loans and investments. Compared to other banks, with a NIM of 3-5%, ABBank is currently at the bottom of the banking industry.

Non-term deposits decreased by 16%, temporary loss of 1,150 billion in securities investment

By the end of the first quarter of 2025, ABBank's total assets reached VND 183,753 billion. Of which, customer deposits decreased by 1% to VND 89,749 billion. In particular, the amount of non-term deposits only reached VND 9,242 billion, down 16% compared to the previous quarter, a large decrease in the top of the banking industry.

ABBank's LDR (loan-to-deposit ratio) only reached 87.49% in Q1/2025, down 2% year-on-year, showing that the bank is not taking full advantage of lending opportunities, causing a waste of capital.

Notably, ABBank increased its securities investment assets from VND20,922 billion at the beginning of the year to VND26,755 billion. However, with this investment, the bank is temporarily recording a loss of VND1,150 billion, an increase of more than VND30 billion compared to the loss provision at the beginning of the year.

Bad debt ratio jumps to 3.8%, missing expectations to stay below 3%

The story of ABBank's bad debt has long been a matter of concern for many shareholders. At the end of the first quarter of 2025, ABBank recorded a continued increase in the bad debt ratio.

Specifically, substandard debt (group 3) and doubtful debt (group 4) decreased to VND613 billion and VND838 billion, respectively. However, debt with the possibility of losing capital increased sharply to VND2,278 billion. Total bad debt was VND3,729 billion, equivalent to the ratio of bad debt to total outstanding customer loans of 3.8%.

Previously, at the 2025 Annual General Meeting of Shareholders, responding to shareholders' opinions on the bad debt ratio at 2.48% which is still quite high, Mr. Dao Manh Khang - Chairman of the Board of Directors of ABBank shared that the bank aims to control the bad debt ratio below 3% and strive to reduce the bad debt level to 2% in 2025.

Mr. Khang also emphasized that 2024 is a difficult year, with many businesses caught up in bad debt and losses, and pledged to implement more radical solutions to handle bad debt.

However, ABBank's bad debt handling area is a bright spot with a dedicated team continuously achieving very positive results. ABBank's goal is not only to reduce bad debt to below 3%, but also to perfect a more professional and effective debt handling system in the long term.

However, with the bad debt ratio exceeding 3% in the first quarter of 2025, the target of controlling below 3% becomes distant, posing a big challenge for banks in improving asset quality and regaining shareholders' trust.

Source: https://baodaknong.vn/abbank-loi-nhuan-tang-no-xau-vuot-nguong-tam-lo-1-150-ty-tu-dau-tu-chung-khoan-254364.html

Comment (0)