Sharp declines in output in two key producing countries, Brazil and Vietnam, are shaking up the supply chain, leaving the market facing a serious shortage in the 2025-2026 crop year and pushing coffee prices back to record highs.

The USDA ’s optimistic forecasts of a year of production recovery of nearly 179 million bags are being gradually denied by reality. Prolonged heat in Brazil has damaged the Arabica bean crop, while floods in the Central Highlands are directly threatening the world’s large and important Robusta crop. With global inventories at record lows and supply chains disrupted, analysts warn that the coffee market is closer than ever to a new “price fever”, even surpassing historical peaks in the coming months.

Double crisis across the coffee market, disillusionment with "bumper harvest"

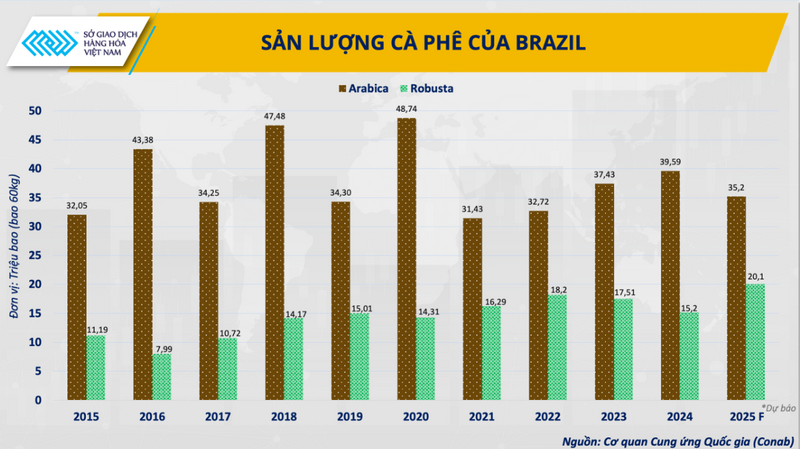

In Brazil, the National Supply Agency (Conab) forecasts total coffee output for the 2025-2026 crop year to reach about 55.2 million bags, down 1.82% from the previous crop. Although Conilon (Robusta) coffee is in a good season, increasing sharply to 20.1 million bags, a record high equivalent to an increase of more than 37%, the output of the strong product Arabica has decreased sharply by 11.2%, to only 35.15 million bags. The reason is due to unfavorable weather and the biennial biological cycle of the coffee tree. According to data from the Brazilian Coffee Exporters Association (Cecafe), the decline in output and record low carryover inventories have caused Brazil's green coffee exports (including Arabica and Robusta) in the first four months of the 2025-2026 crop year to reach only nearly 12.5 million bags, down 22% over the same period.

Brazil's coffee production (Source: Conab)

The situation became even more chaotic when, from August 1, the US imposed an additional 40% import tax on coffee from Brazil, raising the total tax to 50%. This move caused a serious shortage of supply to the US as Arabica inventories on the ICE continuously decreased, reaching the lowest level in nearly two years. The amount of Brazilian coffee in the ICE warehouse alone was only about 22,000 bags, almost zero compared to the same period last year of nearly 430,000 bags.

In addition, the heat wave in early October burned and tore off flower buds, threatening long-term supplies for the 2026-2027 crop. As a result, Arabica prices have skyrocketed over the past three months, spreading the rise to Robusta.

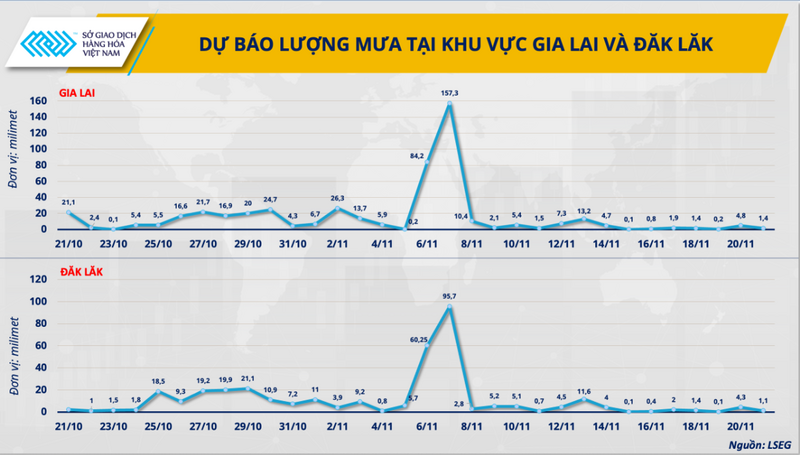

Meanwhile, on the other side of the globe, the market had hoped that a bumper crop in Vietnam would help ease the pressure of global supply shortages, with Robusta output forecast to increase by more than 7% to around 30 million bags. However, the actual weather conditions have shattered all those expectations. In late October, when the harvest was about to peak with more than 80% of the coffee cherries still on the branches, prolonged heavy rains caused flooding in many key areas in the Central Highlands.

Rainfall forecast in Gia Lai and Dak Lak regions (Source: LSEG)

According to MXV analysis, humidity saturation above 95% in the past 10 days has almost paralyzed traditional drying, increasing the risk of mold and causing coffee beans to crack, ferment or fall prematurely. Gia Lai and Dak Nong provinces recorded 81.8 mm and 75.7 mm of rain, respectively, with potential yield losses estimated at 10-20% in the directly affected areas. More worryingly, Typhoon Kalmaegi, forecast to be level 13-14, gusting to level 17, is expected to make landfall in the early morning of November 7, possibly dumping more than 200 mm of rain on already flooded areas.

According to Ms. Maja Wallengren, a reputable Mexican commodity analyst who has followed the Vietnamese coffee industry for more than 31 years, “there is no agronomic evidence that Vietnam can achieve a bumper crop.” She explained that many growing areas are still struggling to recover from severe droughts over the past 2-3 years, and are affected by prolonged drought during the flowering period of March-April.

Before the floods, Vietnam’s most likely production was around 27-28 million bags, a slight recovery. But after the heavy rains, damage from fruit drop and tree rot could see that figure drop to 26-27 million bags, depending on the severity of Typhoon Kalmaegi’s impact.

These losses not only significantly reduce Vietnam’s Robusta output, which contributes up to 40% of the total global supply, but also prolong the harvesting, drying and processing time, making the world coffee supply chain more vulnerable than ever.

A new bullish wave is slowly taking shape...

This crisis is particularly dangerous because the market entered this phase without a safety net. The past three years of volatility, from the frost shock in Brazil in 2021 that sent Arabica prices soaring, to the drought that will cut Vietnam’s output by 20% in 2023-24, have steadily eroded and depleted stocks. So the adverse weather events in Vietnam and the blossom drop in Brazil are not isolated shocks.

MXV predicts that the coffee market will soon react to the serious situation in Brazil, especially Vietnam. If the assumption that Vietnam's coffee output will fall below 26-27 million bags (about 25 million bags for Robusta), that is, a decrease of about 16-17%, or in a worse scenario because the extent of damage caused by the storm is not yet known, Arabica and Robusta coffee prices could therefore skyrocket by at least 20%, or nearly 11,000 USD/ton for Arabica and 5,600 USD/ton for Robusta, and potentially repeat the historic increase due to the drought in the 2023-2024 crop year.

In both Brazil and Vietnam, the global coffee industry is facing a double supply crisis as three key factors – extreme weather, trade policies and low inventories – simultaneously tighten the market. The “bumper harvest” that was thought to cool coffee prices is now likely to become a “dream”, and at the same time, it also signals that a new cycle of high prices may be about to begin...

Source: https://congthuong.vn/con-khat-ca-phe-toan-cau-khi-chu-ky-gia-ky-luc-moi-chi-con-la-van-de-thoi-gian-429299.html

![[Photo] Prime Minister Pham Minh Chinh receives the delegation of the Semiconductor Manufacturing International (SEMI)](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/06/1762434628831_dsc-0219-jpg.webp)

![[Photo] Closing of the 14th Conference of the 13th Party Central Committee](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/06/1762404919012_a1-bnd-5975-5183-jpg.webp)

Comment (0)