Growth drivers

According to Dr. Nguyen Tu Anh, Director of Policy Research at VinUni University, to achieve an economic growth target of 10% or more per year, the size of the economy's credit must double in the next five years. Specifically, he calculated that if real GDP growth reaches 10%, plus about 3% inflation, nominal growth would be around 13%. To meet this level, credit growth needs to reach at least 15% per year, about 2 percentage points higher than the nominal GDP growth rate.

That figure clearly shows that the banking system will remain the main channel for capital flow, playing a crucial role in "injecting lifeblood" into the economy. "Clearly, the role of the banking system in the economy is extremely important," emphasized Dr. Nguyen Tu Anh.

According to this expert, Vietnam is still a "bank-based" economy – relying primarily on banks to provide capital. This model, following the trend of East Asian countries, is likely to persist for at least the next 15 years. Even if the capital market (stock market, corporate bond market, etc.) develops, banks will still maintain an advantage in providing long-term capital and managing risk for the economy.

This stems from the nature of the financial industry. While capital markets require investors to assess and manage risk themselves – a difficult task given the still-developing institutional and legal framework – banks are specialized institutions in collecting, processing information, and managing credit risk. With the development of digital technology , banks are increasingly able to access big data, optimize costs, and expand access to capital to a wider range of stakeholders. Therefore, banks are not only an efficient channel for capital flow but also a channel for managing risk in the economy.

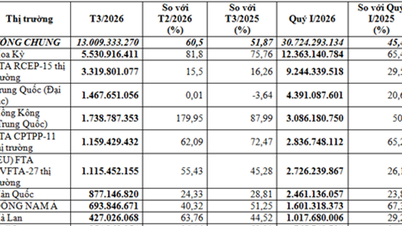

Sharing the same view on the central role of banks, Mr. Quan Trong Thanh, Director of Analysis at Maybank Securities Vietnam, believes that the potential for corporate credit in Vietnam remains very large. Currently, Vietnam's credit-to-GDP ratio is around 134%; of which new corporate loans account for less than 80% of GDP, a fairly healthy level compared to similar economies.

According to Mr. Quan Trong Thanh, the period from 2013 to 2022 witnessed a boom in retail lending, especially for personal consumption, home purchases, and car purchases. However, since 2022, with the volatile macroeconomic environment and a slowdown in personal lending demand, credit flows have shifted strongly towards the corporate sector. From 2024 onwards, corporate lending has become the main driver of credit growth, and Mr. Thanh believes this is the right direction.

The overall investment structure also reflects this trend. Citing statistics, Mr. Thanh stated that in the period 2020-2024, total investment capital reached approximately US$682 billion; with the manufacturing sector accounting for the largest proportion. Although FDI still holds the dominant share in manufacturing investment – mainly borrowing from international banks – the remaining 44% of investment capital comes from domestic banks. Notably, the three state-owned commercial banks (VietinBank, Vietcombank, BIDV ) account for up to 60% of the market share, narrowing the space for joint-stock banks and forcing them to strengthen their retail banking segment. However, in the context of a strong economic growth phase, corporate credit, especially for private enterprises, will be a logical direction for expansion.

The direction of development stems from infrastructure and energy.

In the short term, Mr. Quan Trong Thanh believes that two sectors could become new drivers for bank capital flows: infrastructure and energy. According to calculations by the Ministry of Finance, to achieve a GDP growth target of 10% per year, Vietnam needs a total investment of approximately US$1.4 trillion over the next five years, equivalent to US$280 billion per year. Of this, FDI only accounts for about US$24-30 billion, meaning that more than US$250 billion per year must come from the domestic sector, including the government and private enterprises.

The government is currently strongly encouraging private sector participation in infrastructure and energy investment. “This market is expanding, and the level of private enterprise participation is also increasing,” Mr. Thanh stated. When private enterprises participate, banks are also willing to partner, provided that the businesses demonstrate the capacity to implement the projects. This is an opportunity for banks and the private sector to create an efficient “capital cycle” for the economy.

From an overall perspective, both experts agree that banks remain Vietnam's primary source of capital in the medium and long term. However, this does not mean the capital market should be neglected. On the contrary, a parallel development strategy is needed to reduce the burden on the banking system, especially in the context of sharply increasing capital demand for production, infrastructure, and energy.

Improving the legal framework, enhancing corporate governance capacity, ensuring information transparency, and fostering investor confidence will be prerequisites for the capital market to become an extension of the banking system.

Developing capital channels for the Vietnamese economy in the new phase requires a balance between the central role of banks and the rise of the capital market. Dr. Nguyen Tu Anh affirmed that banks will remain the "backbone" of Vietnam's economic capital flow for at least the next 15 years, while Mr. Quan Trong Thanh indicated that the room for corporate credit, especially in the manufacturing, infrastructure, and energy sectors, remains wide open.

When capital channels develop in harmony, Vietnam can absolutely achieve its target of 10% annual growth in a sustainable and balanced manner, building a safe, flexible financial system ready for a new phase of development.

Source: https://baotintuc.vn/kinh-te/don-bay-von-cho-tang-truong-20251116085922996.htm

![[Photo] General Secretary and President To Lam meets with National Assembly delegates from ethnic minorities.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/04/20/1776696701056_a1-bnd-8331-3342-jpg.webp)

![[Image] National Assembly discusses the implementation of the socio-economic development plan.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/04/20/1776696707422_ndo_br_img-20260420-185419-jpg.webp)

Comment (0)