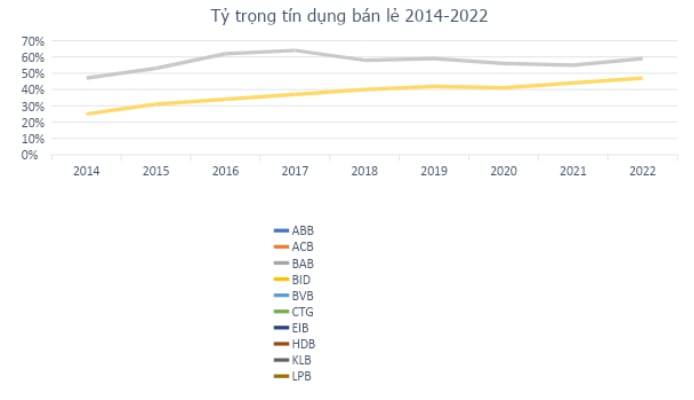

Retail credit has been the main growth driver of credit in the entire Vietnamese banking system over the past years, increasing from about 25% in 2014 to 47% of total outstanding loans by the end of 2022. With the increase in the young population and the middle class, Vietnam's retail banking sector in the future is assessed to have a lot of potential for development. Early recognition of this opportunity, since 2010, Vietnam Prosperity Joint Stock Commercial Bank ( VPBank ) has implemented a strategic initiative to switch to a modern retail banking model on a digital platform, being the pioneer bank pursuing this strategy in Vietnam.

Source: Fiinpro

VPBank's Retail Banking Strategy

With close consultation from McKinsey, VPBank has deployed a modern retail banking model with a strict risk management framework, an advanced credit scoring model, and a strong focus on appraisal and approval.

VPBank is also known for its unique “segment coverage” strategy. VPBank is the only bank that serves all customer segments from the general/near-general customer group through FE Credit to individual customers, business households, SMEs to large enterprises. In order to best serve each customer group, the bank divides different segments to provide specialized financial solutions designed according to needs, such as the Prime brand serving young customers who love to break through, the Diamond brand specializing in serving priority customers in the VIP group, etc.

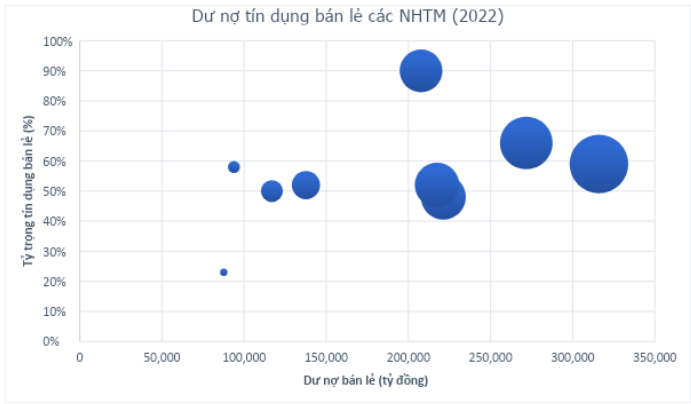

With a comprehensive ecosystem from banking services, to insurance, securities investment, wealth management, fintech (UBank, Cake, Be, LynkID) to serve all financial needs of customers, all revolve around VPBank's Retail Banking strategy. Currently, the proportion of retail accounts for about 60% of the bank's credit portfolio. Credit growth from retail reaches 37% in 2022, while the proportion of capital mobilization from individual customers is also up to 50%. In addition to avoiding concentration risks, this also helps the bank have a more stable and sustainable source of income, although it requires more efforts to deploy business.

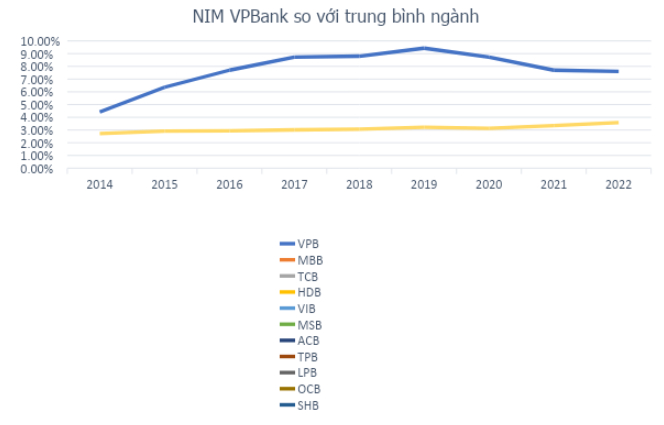

This strategy helps the bank own the industry's largest customer base of 24 million people, meaning that 1 in 4 Vietnamese people will be a VPBank customer. This number increased 2.4 times in the 2017-2022 period, highlighting VPBank's efforts to expand its ecosystem, but cannot overshadow the fact that VPBank is the best bank in higher-risk segments but at the same time also expects to create stronger momentum such as consumer credit. Although steadfast in its "segment coverage" strategy, it cannot be denied that the momentum from the two strategic blocks of KHCN and SME has helped VPBank's performance and profit record impressive numbers. VPBank's pre-tax profit compound annual growth rate (CAGR) in the 2016-2022 period reached 28%/year. NIM index of 7.61% ranked No. 1 in the whole system, while return on equity (ROE) remained high, reaching 17.82% (2022) under the condition that equity had a breakthrough in the period 2016-2022 (CAGR growth of 35%/year).

Source: Fiinpro

With the efficiency indicators now at the top of the system, the question is what basis helps VPBank continue to grow faster and stronger to realize the ambitious 2022-2026 strategy? The key to this question is the strategic partner in the historic deal of nearly 36,000 billion that VPBank reached an agreement to sell 15% of its capital in the last days of March: SMBC bank.

VPBank and SMBC: When we come home together

SMBC is no stranger to the Vietnamese financial and banking market. It has invested in Eximbank since 2007 and recently divested to enter into a strategic cooperation agreement with VPBank. SMBC is a member of SMFG, Japan’s second largest group in terms of total assets with over 2.1 trillion USD - bringing with it experience and expertise in the financial sector with a multi-layered expansion strategy to exploit the growth potential of emerging markets in Asia.

For VPBank, the bank pursuing a retail banking strategy with wide coverage, being the leader in the consumer credit segment that can create strong momentum is a very reasonable strategy in the context of retail credit in general, in which consumer credit is the growth driver of the entire system's credit over the past many years with high profit margins and attractive risk dispersion; this market currently has a lot of potential for development and this stage is not the time to be cautious in growth as when the market is saturated.

This vision is shared by SMBC Bank when, since mid-2021, a subsidiary of this bank has acquired 49% of FE Credit's capital in a $1.4 billion deal, paving the way for the recent historic cooperation agreement in the banking industry (in terms of deal value). In addition to capital increase or sharing of experience and know-how from this leading financial group, this agreement also expects to have an understanding and shared vision of the parties who have experience in the Vietnamese banking and financial market as well as experience in finding strategic partners who "sound the same, draw the same breath", find a common voice to agree to develop together and go together on the long road ahead.

Thus, it can be seen that with its attractiveness, the potential retail “pie” will be focused on by banks to develop in the coming time. In particular, banks with the advantage of being the first mover with a high retail ratio will benefit, especially VPBank with high coverage and a leading customer base along with a strategic partner who understands and shares, have a solid foundation to realize the vision of being in the top 3 largest banks in Vietnam and the top 100 largest banks in Asia, thereby bringing sweet fruits to the bank's steadfast shareholders.

Source

![[Photo] Vietnamese and Hungarian leaders attend the opening of the exhibition by photographer Bozoky Dezso](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/28/b478be84f13042aebc74e077c4756e4b)

![[Photo] Prime Minister Pham Minh Chinh receives a bipartisan delegation of US House of Representatives](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/28/468e61546b664d3f98dc75f6a3c2c880)

![[Photo] General Secretary To Lam works with the Central Policy and Strategy Committee](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/28/7b31a656d8a148d4b7e7ca66463a6894)

![[Photo] 12th grade students say goodbye at the closing ceremony, preparing to embark on a new journey](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/28/42ac3d300d214e7b8db4a03feeed3f6a)

Comment (0)