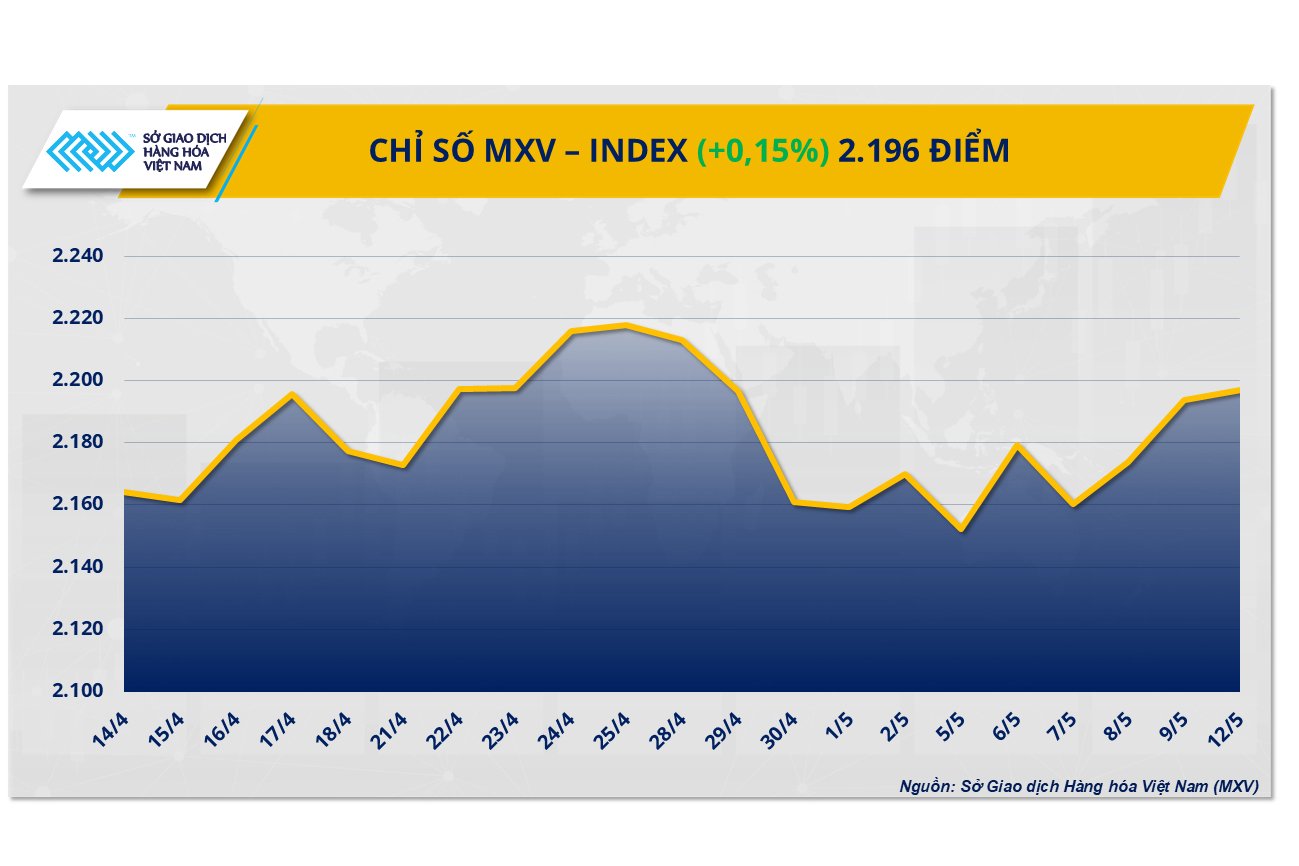

The dominant buying force supported the MXV-Index to increase by 0.15% to 2,196 points. Notably, the prices of soybeans and soybean products increased sharply. On the contrary, the stronger USD unintentionally put pressure on the coffee market.

|

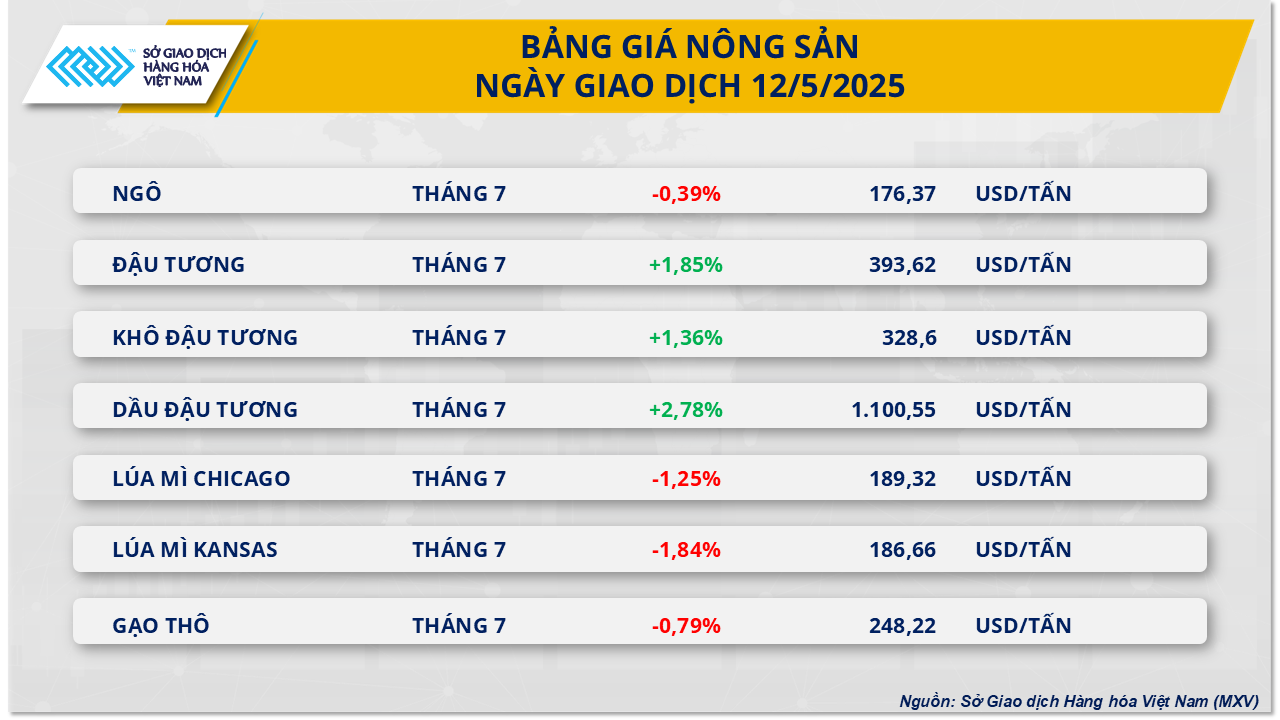

According to MXV, the agricultural market reacted quickly to the results of the tariff negotiations. In particular, soybean prices jumped sharply by 1.85% to 393 USD/ton in yesterday's session. Notably, two finished products, soybean meal and soybean oil, also increased sharply, respectively by 1.36% to 328 USD/ton and 2.78% to 1,100 USD/ton.

|

The focus of the market yesterday was none other than the outcome of the negotiations between the US and China that took place on Saturday, May 10 in Geneva, Switzerland. After months of trade tensions, the agreement of the world's two largest economies to reduce import tariffs for 90 days fueled optimism in the market.

According to the official announcement, the two largest economies have reached an agreement to reduce tariffs on imported goods from the other country. Currently, the US tariff on goods from China has been reduced from 145% to 30%; for China, the reduction is from 125% to 10%. This is a significant reduction, opening up great expectations for agricultural exports, especially soybeans, in the coming time.

The upward momentum in soybean prices was further reinforced after the US Department of Agriculture (USDA) released its May WASDE report with a series of positive figures. Accordingly, the old crop ending inventory decreased to more than 9.53 million tons, lower than market expectations, while the new crop inventory started at more than 8.03 million tons, down 16% compared to the previous year and significantly lower than the average forecast of analysts. Instead of sharply adjusting down exports as previously feared, USDA only slightly lowered the export forecast to 952,500 tons, while oil crushing consumption was raised by 1.9 million tons, reflecting a positive domestic consumption outlook. At the same time, the average selling price expected by farmers was also adjusted up by 30 cents, to $376.63/ton for the new crop.

Globally, the USDA continues to see Brazil's soybean output reach a record high of 175 million tons in the 2025-2026 crop year, cementing its position as the world's leading exporter. At the same time, China's soybean imports are forecast to increase to 112 million tons, reflecting strong demand in this market. However, global soybean inventories are forecast by the USDA to increase to 124.33 million tons, indicating that supply remains abundant and is a factor that needs to be monitored. Notably, China is accelerating its roadmap to reduce the use of soybean meal in animal feed, with the goal of reducing it to below 13% by 2025 and only 10% by 2030. This trend could reduce China's soybean import pressure in the coming crop years, thereby affecting the global supply-demand balance.

For the two finished products, soybean oil prices led the trend of the whole group when they increased sharply by 2.78% in the last session. This increase was mainly due to the information that the 45Z tax credit package for biofuels in the US is likely to be extended until 2031, thereby continuing to boost the demand for soybean oil as a feedstock for biodiesel production.

Coffee prices under great pressure due to exchange rates

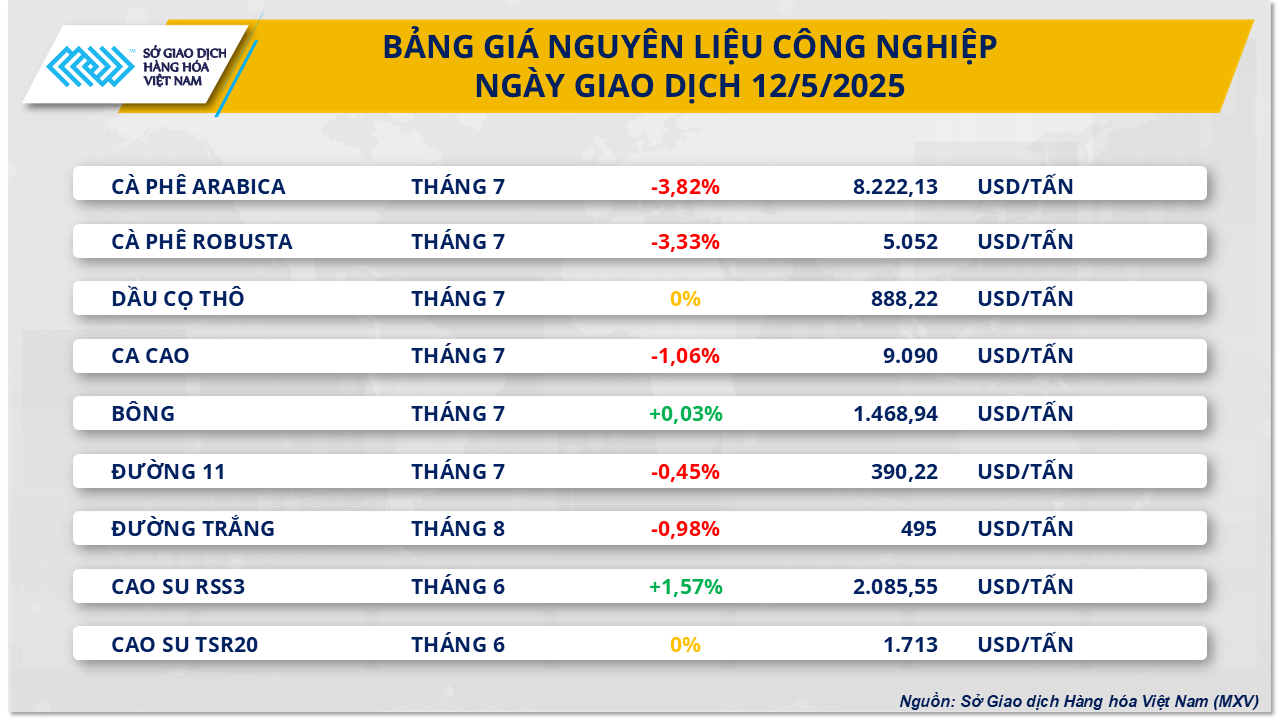

Contrary to the general market trend, the industrial raw material group experienced a less positive trading session when most of the key commodities in the group decreased in price. Of which, the price of Arabica coffee lost nearly 4% to 8,222 USD/ton, the price of Robusta coffee also decreased by more than 3% to 5,052 USD/ton.

According to MXV, coffee prices were under strong downward pressure in the last session, mainly due to the soaring USD after the US-China trade agreement, along with the prospect of continued positive supply.

|

The DXY index jumped sharply yesterday, reaching a one-month high, pushing the USD/BRL exchange rate up 0.26%, thereby boosting export activities in Brazil.

On the supply side, Safras & Mercado’s latest revised report released over the weekend raised its forecast for Brazil’s 2024-25 coffee production to 65.51 million 60-kg bags, up 4.9% from the 62.45 million bags forecast in December. Safras & Mercado said more favorable weather conditions in January and February were the main factor behind the upward adjustment. This forecast is also consistent with the organization's estimate in mid-April. Robusta coffee output is expected to reach about 25 million bags, up 4.16% compared to the December forecast, while Arabica output is raised to 40.46 million bags, up 1.15% compared to mid-April and up 5.5% compared to December. Previously, Conab also adjusted its forecast for Brazil's Arabica coffee output to 37 million bags from the 34.7 million bags forecast at the beginning of the year, while raising total coffee output to 55.7 million bags compared to 51.8 million bags in the January forecast.

In addition, according to Succafina, farmers in Brazil’s main Robusta growing regions began harvesting coffee for the 2025-2026 crop year in late April, slightly later than last year. Field surveys show that the two states of Espírito Santo and Bahia continue to lead in production, with this year’s harvest forecast to exceed previous seasons thanks to favorable weather conditions and high yields. To date, there have been no major disruptions in Brazil’s Robusta growing regions, with the country’s Robusta output expected to reach a record high.

In terms of weather, rains are expected to hit the Central Highlands coffee growing regions late last week and are forecast to continue in the coming days, creating favorable conditions for coffee plants to grow. In contrast, Brazil is expected to face drought conditions over the next 10 days, accompanied by higher-than-average temperatures, which could affect the progress and quality of the country’s coffee harvest.

According to VNA

Source: https://baoapbac.vn/kinh-te/202505/sau-cuoc-dam-phan-my-trung-tam-ly-lac-quan-lan-toa-tren-thi-truong-hang-hoa-the-gioi-1042358/

![[Photo] Prime Minister Pham Minh Chinh receives Rabbi Yoav Ben Tzur, Israeli Minister of Labor](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/511bf6664512413ca5a275cbf3fb2f65)

![[Photo] Prime Minister Pham Minh Chinh receives the President of Asia-Pacific region of PowerChina Group](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/0f4f3c2f997b4fdaa44b60aaac103d91)

![[Photo] Scientific workshop "Building a socialist model associated with socialist people in Hai Phong city in the period of 2025-2030 and the following years"](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/5098e06c813243b1bf5670f9dc20ad0a)

![[Photo] Coming to Son La, let's "show off" with the Wallflowers](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/21/627a654c41fc4e1a95f3e1c353d0426d)

Comment (0)