According to the Social Insurance Law 2024, the compulsory social insurance contribution level is calculated based on the salary used as the basis for compulsory social insurance contribution.

Regarding salary as the basis for compulsory social insurance contributions, the Social Insurance Law 2024 and Decree 158/2025/ND-CP have clearly classified the determination method for each group of subjects, depending on the salary regime they are applying as follows:

In particular, for employees whose salary is decided by the employer, the salary used as the basis for social insurance payment includes:

- Salary according to job or position: Is the salary calculated by time (by month) of the job or position, built according to the salary scale and salary table established by the employer according to the provisions of Article 93 of the Labor Code and agreed upon in the labor contract.

- Salary allowances: These are intended to compensate for factors such as working conditions, the complexity of the job, living conditions, and the level of labor attraction that are not taken into account or are not sufficient in the salary. These allowances must also be agreed upon in the labor contract.

- Other additional payments: These are payments that can be determined in specific amounts along with the salary, agreed upon in the labor contract and paid regularly and stably in each pay period.

Decree 158/2025/ND-CP clearly states that the salary used as the basis for compulsory social insurance payment for subjects specified in Point 1, Clause 1, Article 2 of the Law on Social Insurance is the monthly salary calculated according to the agreement in the labor contract.

Meanwhile, Article 4 of Decree 293/2025/ND-CP (effective from January 1, 2026) guides the application of the monthly minimum wage as follows: The monthly minimum wage is the lowest wage that serves as the basis for negotiation and payment of wages to employees applying the monthly wage payment method, ensuring that the wage according to the job or position of the employee who works enough normal working hours in the month and completes the agreed labor norms or work must not be lower than the monthly minimum wage.

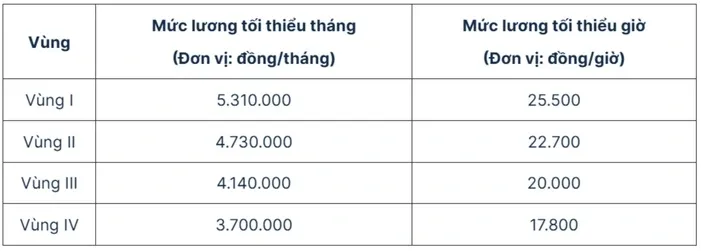

Minimum wages effective from January 1, 2026 are as follows:

Therefore, when the minimum wage is adjusted from January 1, 2026, the minimum wage used as the basis for social insurance contributions for employees implementing the salary regime decided by the employer will increase accordingly.

Specifically, the minimum salary for social insurance contribution in 2026 is as follows:

- In Region I is 5,310,000 VND;

- Region II: 4,730,000 VND;

- Region III: 4,140,000 VND;

- Region IV: 3,700,000 VND.

Source: https://vtv.vn/tang-luong-toi-thieu-tu-2026-muc-dong-bhxh-thay-doi-ra-sao-100251113085256655.htm

![[Photo] Deep sea sand deposits, ancient wooden ship An Bang faces the risk of being buried again](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/13/1763033175715_ndo_br_thuyen-1-jpg.webp)

![[Photo] General Secretary To Lam visits Long Thanh International Airport Project](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/11/13/1763008564398_vna-potal-tong-bi-thu-to-lam-tham-du-an-cang-hang-khong-quoc-te-long-thanh-8404600-1261-jpg.webp)

![[Photo] Panorama of the 2nd Vietnam-Cambodia Border Defense Friendship Exchange](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/11/13/1763033233033_image.jpeg)

![Dong Nai OCOP transition: [Article 3] Linking tourism with OCOP product consumption](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/11/10/1762739199309_1324-2740-7_n-162543_981.jpeg)

Comment (0)