Following the success of TCBS Securities' initial public offering (IPO), these days, investors are looking forward to the IPO of VPS Securities - the leading enterprise in the securities brokerage market share in Vietnam.

During the period from October 16 to November 6, VPS will accept registrations to buy IPO shares from investors with a minimum offering price of no less than VND60,000/share. The total offering volume is 202.3 million shares, expected to raise at least VND12,138 billion. If successful, this scale will exceed the record of VND10,800 billion that TCBS has just raised.

It should be emphasized that the registration to buy and deposit payment is only the first step in the IPO and listing process of VPS. After this stage, the company will: (1) Announce the results of the stock allocation; (2) investors pay the allocated amount; (3) announce the results of the stock purchase; (4) refund if any issues arise.

The most interested question today is: What will be the closing price for the next "blockbuster" IPO of the stock market in 2025?

On forums, investors are discussing enthusiastically around the question: Why doesn't VPS set a pre-set offering price and why is the minimum price not lower than 60,000 VND/share?

Examine the expensive/cheap level from the perspective of business model and efficiency

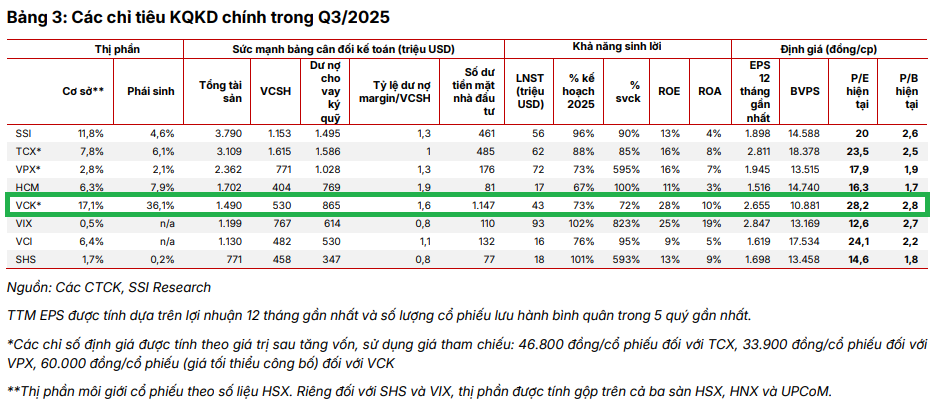

From its current position, VPS owns total assets of more than VND 39,000 billion, ranking among the leading groups in the securities industry in terms of scale. This figure is created by a charter capital of only VND 12,800 billion (as of the end of the third quarter of 2025) - lower than the leading groups such as VPBankS, VIX, SSI or TCBS (all over VND 15,000 billion).

From a business perspective, VPS reported a profit after tax in the third quarter of 2025 of VND 1,126 billion, up 72% over the same period, bringing the accumulated 9-month figure to VND 2,564 billion, up 52% YoY. This growth mark reflects the effectiveness of the strategy of focusing on the core segment - brokerage and margin lending (over VND 22,000 billion); not participating in stock trading helps VPS eliminate risks when the market fluctuates.

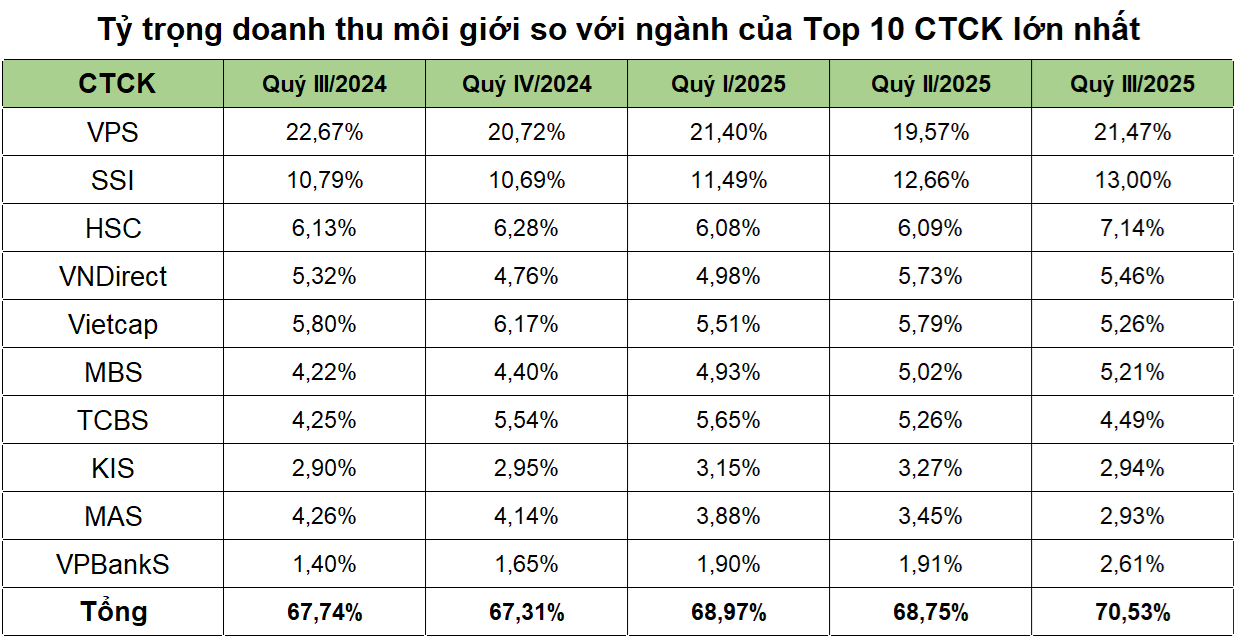

If TCBS leads the bond issuance consulting segment, VPS has just set a record for brokerage revenue in the third quarter, reaching VND 1,500 billion - accounting for more than 20% of the total brokerage revenue of the entire industry (VND 7,000 billion, source Wichart). VPS is also the first company in the history of the Vietnamese securities industry to achieve brokerage revenue of thousands of billions of VND/quarter, a figure realized by maintaining the No. 1 position in brokerage market share on HoSE, HNX, UPCoM and derivatives from the first quarter of 2021 to present - an unprecedented record.

(Source: General data)

Thanks to that, the return on equity (ROE) in the third quarter of 2025 reached 24.4%, among the highest in the industry.

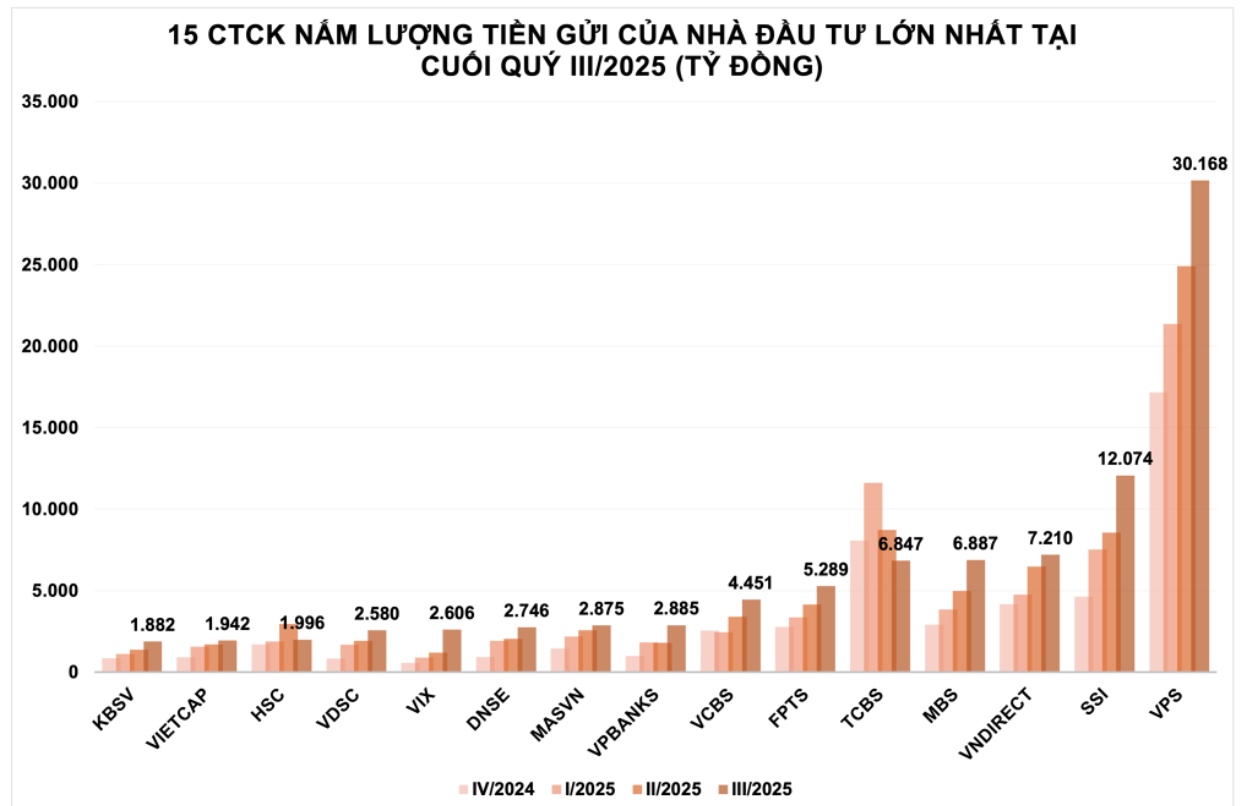

Along with the brokerage segment, strong financial resources help VPS continue to expand margin operations. By the end of September 2025, the company is leading the industry with 30,200 billion VND in investor deposits, more than twice as much as the next company, SSI, and accounting for 27% of the entire industry (synthesized from Wichart data).

(Source: Data compiled from Wichart)

FTSE Russell's official upgrade of Vietnam to emerging market status is expected to open a new wave of capital flows, leading to a surge in liquidity - a factor that directly impacts VPS's brokerage revenue and margin profits.

In particular, liquidity is expected to explode even more when a series of new mechanisms come into operation such as trading through noon, extending the order matching time, selling securities waiting to return or T+0. These changes are expected to speed up investors' capital turnover, leading to a surge in order matching volume.

In fact, the average liquidity in the first 9 months of 2025 reached VND 29,200 billion/session, an increase of nearly 40% compared to 2024, with many sessions exceeding 2-3 billion USD. International experience also shows a similar effect: in Taiwan (China), T+0 helped liquidity increase by 45%; in Korea, the EXTURE system launched in 2009 tripled transactions.

Thanks to its leading market share and abundant financial resources, VPS is in a rare position to directly benefit from the new growth wave of the Vietnamese stock market.

From the operating model perspective, VPS owns an internal technology team of hundreds of engineers, self-developed high-speed trading infrastructure and data platform serving millions of users, thereby positioning itself as a leading FinTech institution in the securities industry.

"Scoring" in both operating model and business efficiency, the question "why VPS does not announce a fixed offering price?" is increasingly of interest to investors. In fact, the answer lies in the IPO mechanism that VPS is implementing: The offering price is decided by the participating investors - those who directly "score" the value of the company.

Who are the "customers" participating in VPS's IPO?

First of all, we can mention the group of foreign investors, in which more than 50 international investment funds have expressed interest in the investment promotion sessions that VPS leaders recently shared.

The presence of this "foreign" cash flow is almost certain, especially when VPS appointed Mr. John Desmond Sheehy - an expert with many years of senior consulting experience - to the Board of Directors, demonstrating the direction of expanding influence outside of Vietnam.

Along with foreign investors, "VPS investors" can also be part of the approximately 1.6 million customers trading at VPS, and more broadly, the 11 million domestic securities accounts, including other organizations and securities companies.

So, the picture of the potential investor group of VPS IPO has somewhat appeared. The remaining question is: How much are they willing to pay to buy in?

According to the allocation principle, valid purchase orders are orders with a purchase price ≥ 60,000 VND/share. If the total purchase order ≤ the offering amount, investors will be able to buy the exact number of registered shares. Conversely, if the total purchase order > the offering amount, orders with higher prices will be given priority for distribution until all the offered shares are sold. The remaining shares will be allocated proportionally to orders with prices equal to the offering price, according to the formula: Allocation ratio is equal to the number of remaining shares divided by the total number of shares registered to buy at the offering price.

However, the final price of this IPO will only be determined after the IPO closes. In the market, there are groups of investors who are cautiously waiting, but there are also groups that have entered the market early, ready to "put down money" to ensure a purchase position.

Investing in stocks is always about expectations. Therefore, the level of 60,000 VND or higher does not determine the expensive/cheap position of the stock. It all depends on the vision and belief of investors in VPS's journey in the new era.

Source: https://vtv.vn/cuoc-dua-gianh-suat-ipo-vps-tiep-tuc-nong-100251031144625674.htm

Comment (0)