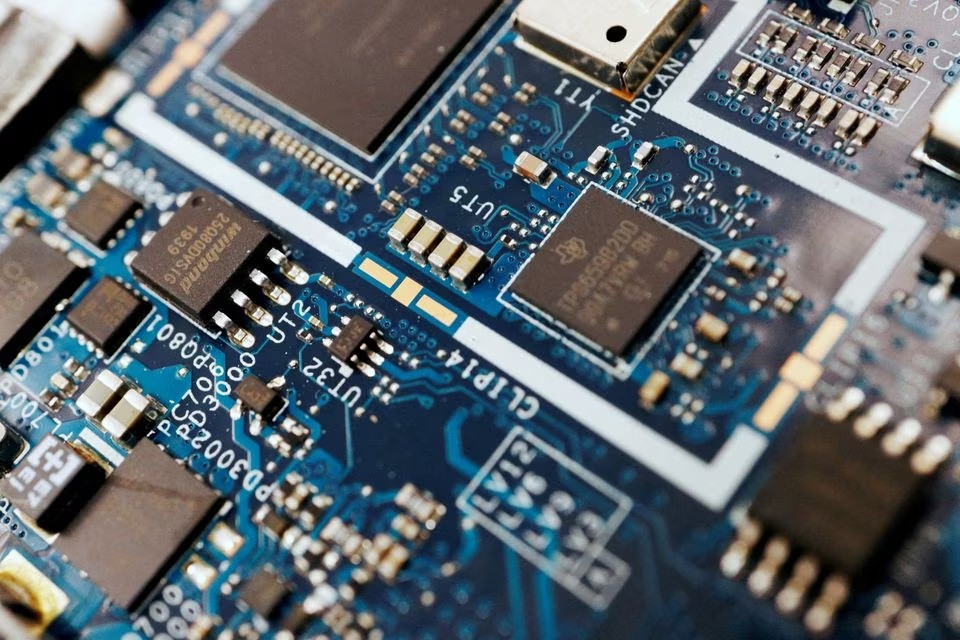

In 2023, all major chip markets, such as smartphones, PCs and data centers, will shrink significantly as business and consumer customers cut spending amid a weakening global economy , runaway inflation and rising interest rates.

The negative factors have created an unprecedented oversupply of consumer chips. In the first six months of 2023 alone, the world's two largest memory chipmakers, Samsung and SK Hynix, incurred operating losses of 15.2 trillion won ($12 billion).

Data from technology analyst Canalys shows that the semiconductor supply-demand balance has improved with production cuts and PC shipments falling only about 11% by June 2023, compared with 30% in the previous two quarters.

The smartphone market is also improving, with smartphone sales falling 8% in the last three months compared to a 14% decline in the first quarter of 2023, according to research firm Counterpoint.

“Demand is recovering but very slowly,” SK Hynix CFO Woohyun Kim said during the company’s earnings call. “The improvement in PC shipments is mainly due to promotions and low-end models, which means it has a limited impact on the overall recovery in chip demand.”

While demand for generative AI-powered chips has grown rapidly since OpenAI's ChatGPT launched in late 2022, the sector still accounts for only a small portion of overall chip demand, even reducing some companies' spending on servers as they shift investments to AI.

In addition, a slow recovery in China, the world's largest chip market, also dampens the overall industry outlook.

Both Samsung and SK Hynix said China's reopening did not meet expectations for a speedy smartphone market recovery, and said they were extending production cuts to NAND memory chips, which are widely used in handheld mobile devices to store digital data.

Similarly, Texas Instruments (TI), a chipmaker with close ties to the Chinese market, forecasts second-quarter 2023 revenue and profit below Wall Street expectations as slow demand recovery forces partners to cancel orders.

By the end of fiscal 2022, China will account for “half of TI’s sales,” according to Logan Purk, an analyst at investment firm Edward Jones.

AI is the bright spot

Foundry equipment makers KLA Corp and Lam Research are among the beneficiaries of the AI boom, with both companies forecasting quarterly revenue that beat Wall Street estimates.

“Advanced AI servers are significantly more efficient than traditional servers. Every 1% increase in AI servers and data centers drives an additional $1 billion to $1.5 billion in investment,” said Tim Archer, CEO at Lam Research.

Chipmakers are also ramping up production of high-end processors used to support AI chips.

SK Hynix said demand for AI server memory doubled in the second quarter of 2023 from the first three months of the year. On average, prices of DRAM chips, which store information for applications running on the system, increased compared to the first quarter of 2023.

According to TrendForce, the Korean manufacturer is also the market leader in high-bandwidth DRAM (HBM) used in artificial AI, with a 50% market share in 2022, followed by Samsung's 40% and Micron's 10%.

(According to Reuters)

Source

![[Photo] T&T 1 and Ho Chi Minh City 1 People's Police Teams won the men's and women's team championships](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/22/39db06ae67cb4001b7a556e8d9a56d07)

![[Podcast] Week introducing more than 500 OCOP products in Hanoi](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/5/22/d144aac2416744718388dbae3260e7fd)

Comment (0)