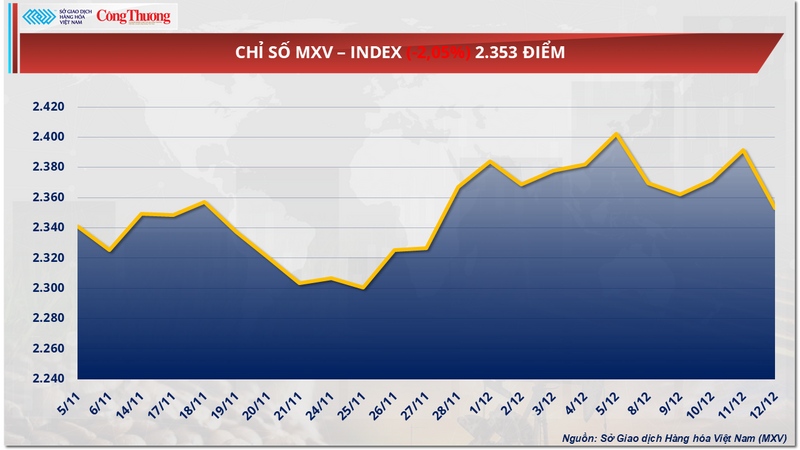

The supply-demand dynamic continued to drive global commodity markets last week (December 8-14, 2025), with contrasting movements across different product groups. This was evident as crude oil prices fell sharply due to oversupply pressure, while the sugar market recovered thanks to concerns about production costs and medium-term supply. Selling pressure dominated, dragging the MXV-Index down by more than 2%, to 2,353 points.

MXV-Index

Oversupply weighs heavily, causing oil prices to fall sharply.

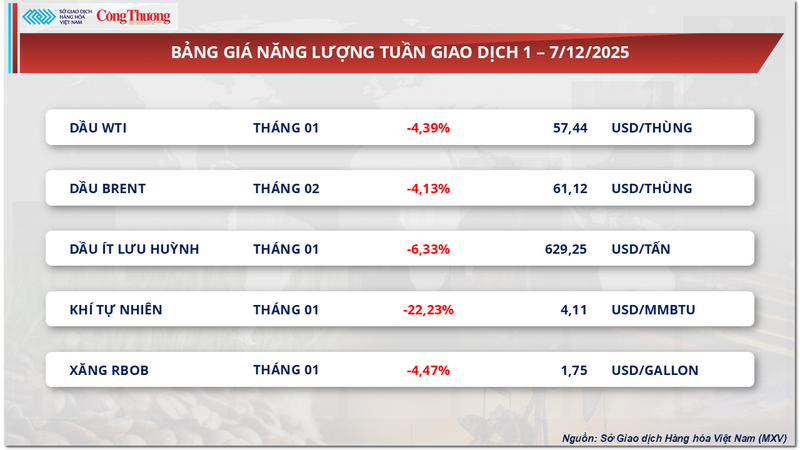

According to the Vietnam Commodity Exchange (MXV), the energy market plunged into the red last week as all five commodities in the group simultaneously declined. Specifically, WTI crude oil lost nearly 4.4% compared to the previous week, falling to $57.4 per barrel; Brent crude oil also retreated to $61.1 per barrel, a decrease of over 4.1%.

Energy price list

According to the Vietnam Commodity Exchange (MXV), the main reason for the weakening oil prices last week stemmed from growing concerns about oversupply in the global market. The latest reports from the International Energy Agency (IEA), the Organization of Petroleum Exporting Countries (OPEC), and the US Energy Information Agency (EIA) all show an increasingly clear imbalance between supply and demand.

In its December report, the International Energy Agency (IEA) slightly lowered its forecast for the oil surplus in 2026 to 3.84 million barrels per day, but this level is still equivalent to nearly 4% of global demand, which is considered very high compared to previous periods. The IEA emphasized that supply from outside OPEC+, particularly from the US and the Americas, continues to grow faster than demand growth.

Contrary to the IEA, the Organization of Petroleum Exporting Countries (OPEC) believes the market is likely to reach equilibrium in 2026 if OPEC+ maintains strict production discipline. However, this argument has not convinced investors, as the bloc has already increased its quota by more than 2.7 million barrels per day in 2025 and has only temporarily halted production increases in the first quarter of 2026. This development raises concerns that OPEC+ is prioritizing market share protection over price support.

Meanwhile, the EIA continued to increase pressure by raising its forecast for US crude oil production in 2025 to a record 13.61 million barrels per day, while assessing that oil demand in the US economy will remain virtually flat in 2026. The prospect of "increasing supply - slowing demand" in the world's largest oil consumer has significantly weakened expectations of a price recovery in the medium term. In addition, recent inventory data showed that US crude oil inventories decreased less than expected, while gasoline and distillate inventories increased sharply, reflecting that actual fuel consumption demand remains weak.

In Asia, the downward price trend is even more pronounced as buyers demand increasingly deeper discounts compared to the Brent benchmark price. Intense competition from oil sources such as Russia, Iran, Venezuela, and the Middle East has forced Saudi Arabia to lower its official selling price to the Asian market to its lowest level in years. At the same time, China's energy demand continues to disappoint, with CNPC studies showing that its oil consumption is gradually entering a plateau phase between 2025 and 2030.

In this context, geopolitical factors such as tensions in Venezuela or the Black Sea region have only had short-term impacts. The actual flow of oil has been minimally disrupted, while competitive pressure has forced exporting countries to adjust their selling prices downwards. With the oversupply picture still prevailing, MXV believes that world oil prices next week are likely to continue to face downward pressure or fluctuate at low levels, as the oversupply issue remains the dominant factor influencing market sentiment.

Sugar prices surged amid cost pressures and large short positions.

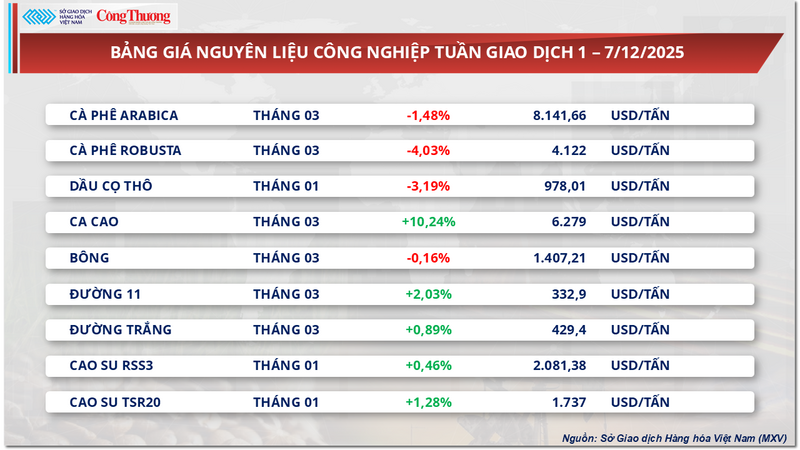

Conversely, the industrial raw materials market last week saw overwhelming buying pressure as prices of many commodities rose sharply. In particular, attention was focused on the global sugar market, where the prices of both white sugar and refined sugar showed positive recovery.

At the close of trading on Friday (December 12), raw sugar prices surged 2.03%, reaching $332.9 per ton; white sugar prices also increased by nearly 1%, trading around $429 per ton.

Industrial raw material price list

In India, the world's second-largest sugar producer, the sugarcane crushing season has returned to a stable trajectory after being disrupted by farmer protests. While crushing is being accelerated with expectations of reaching 35 million tons, the country's sugar industry is facing a serious financial paradox: actual production costs far exceed selling prices. Farmers are demanding a minimum sugarcane price equivalent to approximately $375 per ton of sugar equivalent, about $44 per ton higher than international market prices.

Meanwhile, factory production costs have risen to around $430 per ton, but domestic sugar prices are only around $397 per ton. This negative difference, coupled with many factories having to pay higher raw material prices than the regulated floor, is putting pressure on the Indian government to consider adjusting the minimum selling price (MSP). Without timely intervention, the risk of outstanding sugarcane payments is predicted to erupt as early as February, threatening the stability of the global sugar supply chain.

However, current sugar price movements are heavily influenced by the New York market, as investment funds hold high levels of short positions. According to data from the US Commodity Futures Trading Commission (CFTC), short positions have exceeded 207,000 lots, accounting for approximately 22% of total open contracts. In the past, such periods have often been accompanied by technical rallies, when funds buy back to close their positions. Analysts note that if sugar prices remain in the low range of $320-$342 per ton for an extended period, medium-term supply could be affected due to sugarcane growers limiting investment.

Furthermore, another key factor supporting the market is competition from ethanol. Currently, ethanol prices are $33 to $55 per ton higher than sugar traded on the New York exchange, indicating that sugar is undervalued relative to its economic value. With ethanol inventories at record lows during the transition period, Brazilian mills are likely to prioritize sugarcane production for biofuels at the start of the next season to maximize profits. This shift in production structure will reduce the supply of sugar for export, creating a relatively stable support level for prices and limiting the potential for further declines in the near future.

In the domestic market, imported sugar reached over 41,000 tons last week, driven by an increase in supplies from Thailand, while informal sugar imports were scarce due to strict border controls. This kept retail prices high, around 16,600 – 16,800 VND/kg. Domestic supply is in the transition period between seasons, with low inventory of old stock and declining quality, and limited availability of new crop sugar, resulting in sluggish market activity. Factory prices for RS sugar remained stable at around 17,500 - 17,550 VND/kg, but demand was weak as traders tended to wait for better quality new crop sugar before increasing their purchasing activities.

Price list for some other types of goods

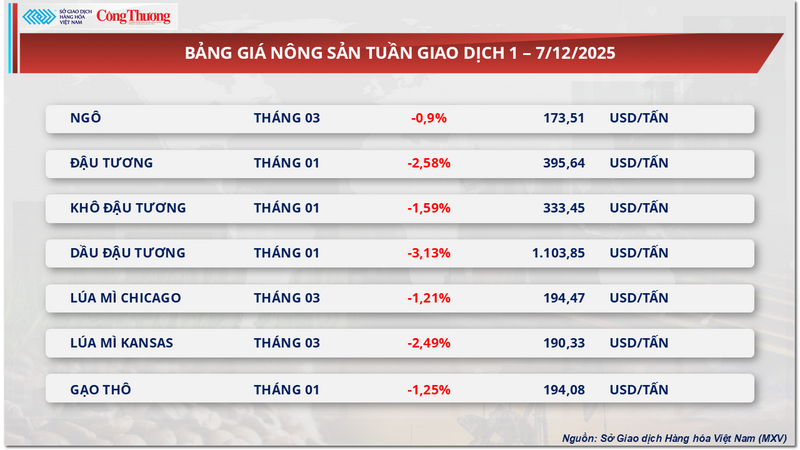

Agricultural product price list

Metal price list

Source: https://congthuong.vn/gia-dau-the-gioi-suy-yeu-trong-tuan-qua-do-lo-ngai-du-cung-434804.html

![[Photo] Two flights successfully landed and took off at Long Thanh Airport.](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F15%2F1765808718882_ndo_br_img-8897-resize-5807-jpg.webp&w=3840&q=75)

Comment (0)