At the close of trading on July 3rd, the VN-Index stood at 1,381.96 points, down 2.63 points (equivalent to 0.19%).

The upward momentum comes from large-cap stocks.

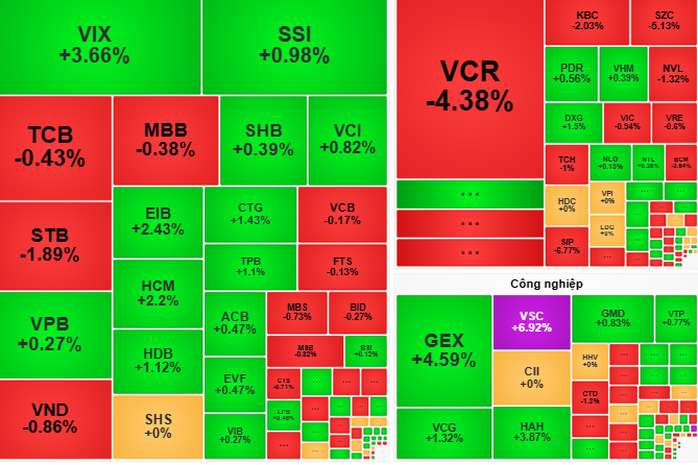

The Vietnamese stock market opened the trading session on July 3rd with a slight downward trend below the reference level, influenced by information related to tariff negotiations between Vietnam and the US. However, the VN-Index quickly recovered its positive momentum thanks to the pull from large-cap stocks such as MWG, HPG, and the banking sector with prominent stocks like VCB, CTG, and TCB.

Conversely, GVR and VIC continued to put pressure on the VN-Index. The securities sector (VIX, HCM) and shipping sector (VOS, VSC) attracted strong capital inflows in the morning session, boosting liquidity by 40% compared to the previous morning. This reflects the gradually improving investor sentiment after the VN-Index surpassed the 1,390 point mark.

In the afternoon session, increased selling pressure caused the VN-Index to narrow its gains and end the session in the red. Mid-cap stocks, along with securities and real estate sectors, maintained good demand. However, profit-taking pressure on banking stocks and sharp corrections in the industrial park (BCM) and rubber (GVR) sectors put pressure on the overall index.

At the close of trading, the VN-Index stood at 1,381.96 points, down 2.63 points (equivalent to 0.19%).

Foreign investors continued to be strong net buyers on the HOSE exchange with a total value of VND 2,276.41 billion, focusing on stocks such as SSI (+VND 431.6 billion), MWG (+VND 294.3 billion), CTG (+VND 146.9 billion), HCM (+VND 133.2 billion), and VCI (+VND 125.7 billion).

Cash flow is clearly differentiated.

According to VCBS Securities Company, the correction on July 3rd was normal after the previous strong rally, when the VN-Index approached the resistance level of 1,392 points. The market is currently in a supply-demand testing phase in the 1,380-1,390 point range, with clearly differentiated capital flows, prioritizing stocks with positive Q2/2025 business results or those with unique growth stories. The retail, steel, and securities sectors maintained their gains, while the industrial park, seafood, and rubber sectors recorded significant corrections.

Rong Viet Securities (VDSC) noted that increased liquidity compared to the previous session indicates that capital flows remain the driving force supporting the market, despite increased profit-taking pressure as the index reached new highs. It is expected that selling pressure may continue to exert pressure in the trading session on July 4th, but the correction trend will only be short-term.

What should investors do?

Given the volatile market conditions, VDSC recommends that investors carefully observe supply and demand, and consider taking partial profits to protect gains, especially on stocks that have recently seen significant price increases.

Meanwhile, VCBS Securities Company suggests that investors can take advantage of corrections to invest in stocks with good growth patterns in sectors such as securities (SSI, HCM, VCI), steel (HPG), and retail (MWG), prioritizing stocks with positive business results.

Some securities firms predict that the market on July 4th will continue its divergent trend, with opportunities focusing on stocks with strong fundamentals and clear growth stories. Investors need to closely monitor market signals to make appropriate trading decisions.

Source: https://nld.com.vn/chung-khoan-ngay-mai-4-7-dong-tien-se-don-vao-co-phieu-co-ket-qua-kinh-doanh-tich-cuc-196250703173553197.htm

![[Image] Vietnam's colorful journey of innovation](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F14%2F1765703036409_image-1.jpeg&w=3840&q=75)

![[Image] Vietnam's colorful journey of innovation](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/14/1765703036409_image-1.jpeg)

Comment (0)