According to the Vietnam Commodity Exchange (MXV), the global commodity market last week (December 8-14, 2025) saw mixed developments, with supply and demand continuing to be the main driving factors. Crude oil prices fell sharply due to oversupply pressure, while sugar prices recovered significantly.

Oil prices plummet amid oversupply pressures.

The energy market was in the red as WTI crude oil prices lost nearly 4.4% of their value compared to last week, falling to $57.4 per barrel. Similarly, Brent crude oil prices also dropped by more than 4.1%, retreating to $61.1 per barrel. The main reason identified is growing concerns about oversupply in the global market.

Major reports all point to the imbalance.

December reports from several leading energy organizations reinforced this assessment:

- The International Energy Agency (IEA) forecasts an oil surplus of 3.84 million barrels per day in 2026, equivalent to nearly 4% of global demand. The IEA emphasizes that supply from outside OPEC+, particularly from the US, is growing faster than demand.

- The Organization of Petroleum Exporting Countries (OPEC) argues that the market could balance by 2026 if OPEC+ maintains production discipline. However, this argument is not convincing enough for investors, as the bloc has already increased quotas and will only temporarily halt them in the first quarter of 2026.

- The U.S. Energy Information Agency (EIA) has raised its forecast for U.S. crude oil production in 2025 to a record 13.61 million barrels per day and predicts demand will remain relatively flat in 2026.

In addition, recent data shows that US crude oil inventories decreased less than expected, while gasoline and distillate inventories increased sharply, reflecting that actual fuel consumption demand remains weak.

In Asia, downward pressure on prices is becoming more pronounced as supplies from Russia, Iran, Venezuela, and the Middle East compete fiercely, forcing Saudi Arabia to lower its official selling prices. At the same time, demand from China is showing signs of slowing down. According to MXV, with the prevailing oversupply picture, oil prices are likely to continue facing downward pressure next week.

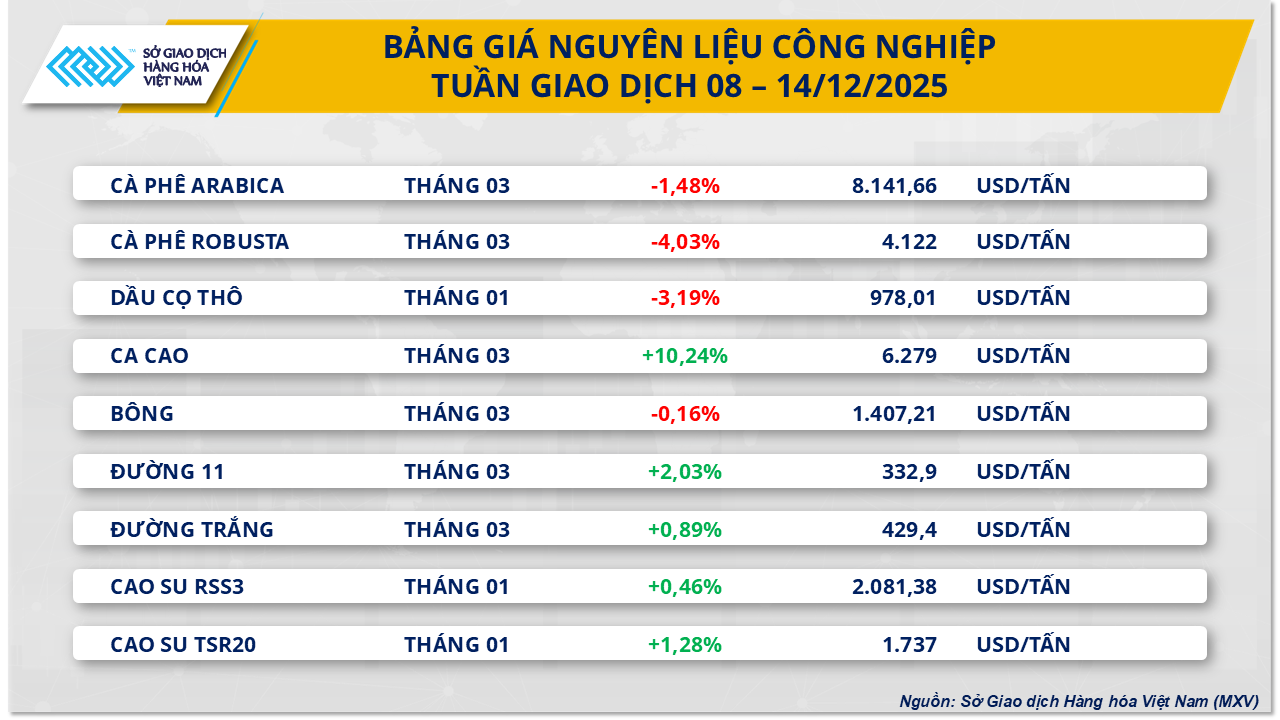

Sugar market recovers amid supply concerns.

In contrast to the energy sector, the industrial raw materials sector saw overwhelming buying pressure, particularly in the sugar market. At the close of trading on Friday (December 12th), raw sugar prices rose 2.03% to $332.9 per ton; white sugar prices also increased by nearly 1%, trading around $429 per ton.

The cost paradox in India

In India, the world's second-largest sugar producer, the sugar industry is facing serious financial problems as production costs far exceed selling prices. Factory production costs are around $430 per ton, while domestic sugar prices are only about $397 per ton. This situation may force the government to intervene to stabilize the supply chain.

Technical and competitive factors from ethanol

The market is being heavily impacted by record-high short positions held by investment funds, which could lead to technical rallies. Furthermore, ethanol prices are currently $33 to $55 per ton higher than sugar prices. This encourages Brazilian mills to prioritize ethanol production, thereby reducing the supply of sugar for export and creating a solid price support level in the near future.

Source: https://baolamdong.vn/gia-dau-wti-giam-gan-44-do-lo-ngai-du-cung-toan-cau-410455.html

![[Photo] Two flights successfully landed and took off at Long Thanh Airport.](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F15%2F1765808718882_ndo_br_img-8897-resize-5807-jpg.webp&w=3840&q=75)

Comment (0)