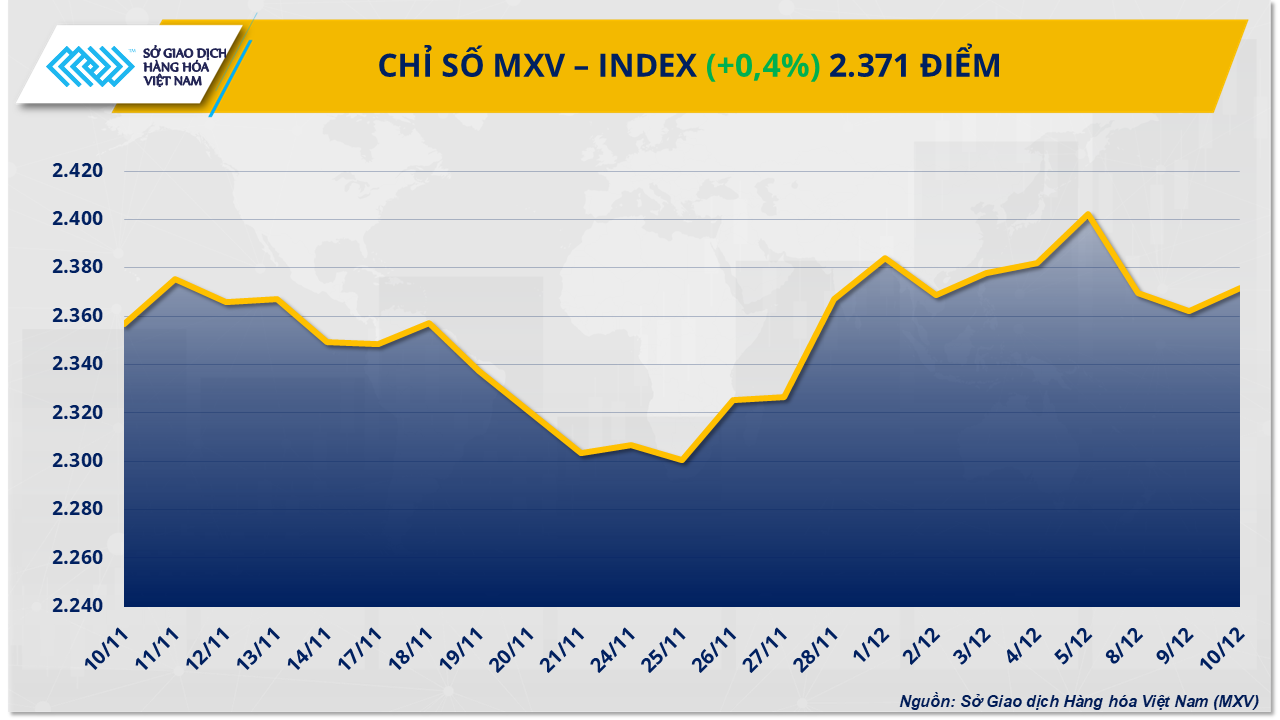

This move triggered investor optimism, bringing money back into the commodities market on December 10th. At closing, the MXV-Index rose 0.4% to 2,371 points.

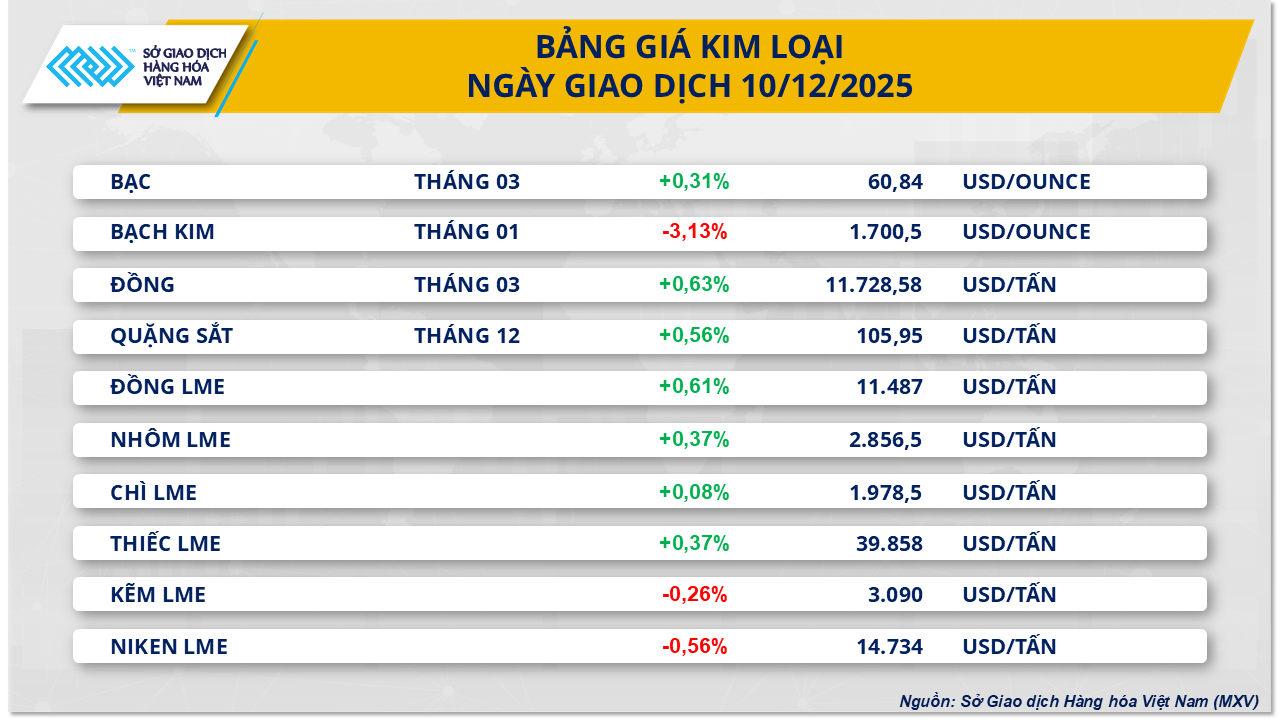

Copper prices recovered after two consecutive days of declines.

Closing yesterday's trading session, the metals market was dominated by green as 7 out of 10 commodities rose in price. Notably, after two consecutive sessions of weakness, the price of COMEX copper recovered by more than 0.6%, reaching $11,802 per ton.

This positive development comes shortly after the Federal Open Market Committee (FOMC) concluded its two-day policy meeting and decided to cut the benchmark interest rate by another 25 basis points. Accordingly, the federal funds rate was brought down to a range of 3.5-3.75%, the lowest level since November 2022. The Fed stated that job growth has slowed this year, while the unemployment rate has risen, thus reinforcing the rationale for easing monetary policy.

Lower interest rates weakened the US dollar, making dollar-denominated commodities, including copper, more attractive. The DXY index also ended its four-session winning streak yesterday, falling 0.6% to 98.66 points.

The recovery in copper prices is also being supported by policy signals from China. Beijing has reaffirmed its commitment to an active fiscal policy and a “slightly dovish” monetary stance amid a sluggish real estate market, slowing consumption, and excess capacity in some sectors. As the world's largest copper consumer, any commitment to macroeconomic support from China bolsters expectations for demand.

Earlier, in late November, news circulated in the market that China was considering a new package of measures for the real estate sector, including mortgage subsidies, easing income tax deductions, and reducing housing transaction costs. These policies would directly impact the construction industry – a sector that accounts for approximately 26% of global copper demand – and therefore become a crucial catalyst supporting prices.

Conversely, the market remains focused on the risk that the US may impose import tariffs on refined copper next year, which could fuel a surge in the metal's flow into the US. As of December 10th, the amount of copper held in COMEX's storage facilities had increased to over 403,000 tons, 4.8 times higher than at the beginning of the year. According to the US Geological Survey (USGS), the US will consume approximately 1.6 million tons of refined copper in 2024, with nearly half of that dependent on imports. The risk of tariffs therefore raises concerns about potential localized supply shortages in this market, further driving up copper prices.

Supply and demand factors pushed corn prices below $175 per ton.

Yesterday's agricultural market saw selling pressure prevail, with 5 out of 7 commodities closing in the red. Corn prices attracted particular attention, recording a drop of over 0.8%, falling below $175/ton and settling at $174.8/ton.

According to MXV's assessment, the downward pressure on corn prices yesterday mainly stemmed from a less positive supply and demand picture. The weekly report from the US Energy Information Agency (EIA) showed that in the week ending December 5th, US ethanol production reached just over 1.1 million barrels per day, a decrease of nearly 2% compared to the previous week. Although ethanol inventories decreased slightly by 1,000 barrels, ethanol input at refineries fell by 6,000 barrels per day to 851,000 barrels per day, while exports decreased by as much as 45,000 barrels per day to 125,000 barrels per day.

Corn demand has also been negatively impacted by data from the European Commission (EC). As of December 7th, EU corn imports for the 2025-2026 season totaled only 7.12 million tonnes, a decrease of over 20% compared to the same period last year. Conversely, EU soft wheat exports reached 10.16 million tonnes, nearly 3% lower than the same period, indicating a less than favorable picture for grain consumption in the region.

Pressure is further increasing from the supply side following a statement by Argentine Economy Minister Luis Caputo indicating that President Javier Milei's administration will cut export taxes on a range of agricultural products. Specifically, export taxes on wheat and barley will be reduced from 9.5% to 7.5%, while taxes on corn and sorghum will decrease from 9.5% to 8.5%. This move is expected to boost export supplies from Argentina – the world's third-largest corn exporter and one of the key wheat suppliers.

Overall, the global grain market is under significant pressure from abundant supply, particularly for wheat. At the close of trading yesterday, Chicago spring wheat futures for January 2026 delivery on the CBOT fell 0.94%, below $195 per ton; while Kansas winter wheat retreated to $192.3 per ton, its lowest level since early December, a decrease of over 0.7%.

The US Department of Agriculture 's (USDA) forecasts in its December report on global agricultural supply and demand (WASDE) continue to reinforce the view of many organizations and consulting firms regarding the abundant global wheat supply, thereby maintaining downward price pressure on the grain group.

Source: https://baotintuc.vn/kinh-te/fed-noi-long-chinh-sach-kich-hoat-luc-mua-tren-thi-truong-hang-hoa-20251211090426885.htm

![[Infographic] Many activities at the 96th anniversary commemoration of the death of Deputy Scholar Nguyen Sinh Sac](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/11/1765441454787_infographic-nhieu-hoat-dong-tai-le-gio-lan-thu-96-cua-cu-pho-bang-nguyen-sinh-sac20251211010322.webp)

Comment (0)