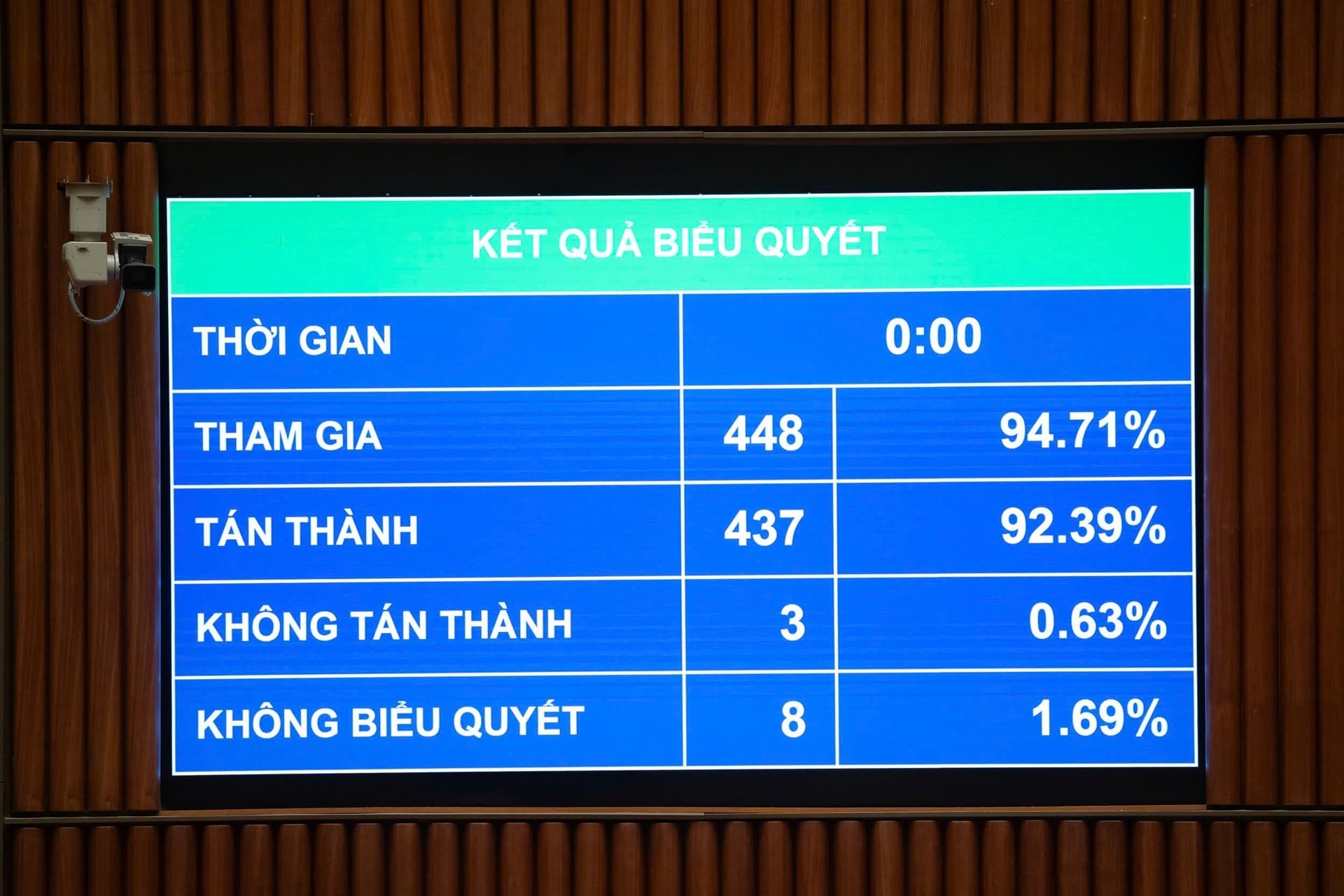

This morning, December 10, at the Hall, the National Assembly voted to pass the amended Law on Tax Administration. With 437/448 delegates participating in the vote in agreement (accounting for 92.39%), the National Assembly voted to pass the amended Law on Tax Administration.

Previously, presenting the report on Receiving, explaining, revising and perfecting the draft Law on Tax Administration (amended), Minister of Finance Nguyen Van Thang raised a number of contents in Clause 5, Article 9 of the draft Law when many opinions of National Assembly deputies suggested reviewing the regulation allowing a portion of the additional revenue from anti-fraud and collection to be used for rewards.

In addition, it is recommended to review the reasonableness in the context of the new salary reform, clearly stipulate the principles of calculating bonuses, funding sources and ensure compliance with the State Budget Law. Agree to reward when excellently completing the revenue target according to the Resolution of the National Assembly/People's Council; or oppose the provisions on the special income mechanism in the Law, and propose that tax officials only enjoy the general regime of state officials.

In addition, many opinions also requested to ensure the uniformity of income levels among sectors, in line with the policy of abolishing the special income regime in salary reform. In addition, there were opinions suggesting to clarify the concept of "over-revenue", add the rate of deduction from over-revenue and assign the Government to regulate the allocation and use of funds.

The Minister of Finance informed: In response to the review comments, the National Assembly Deputies and the Government Party Committee assigned the Ministry of Finance Party Committee to report to the Politburo on the content of supplementing income for tax management officials. Up to now, the Standing Secretariat has given opinions as reported in Point a, Part A, Section III above. Accordingly, the Government has accepted and removed the content of Clause 5, Article 9.

Regarding the opinion of the Deputy Secretary General of the Vietnam Confederation of Commerce and Industry (VCCI): Propose to remove the regulation on temporary suspension of exit for beneficial owners if the enterprise has not fulfilled its tax obligations. According to the representative of VCCI, this regulation is too broad and unreasonable, because according to the Enterprise Law, only needing to own 25% or more of capital is considered a beneficial owner without having to directly manage the enterprise.

On behalf of the Government, Minister of Finance Nguyen Van Thang affirmed: The regulation on temporary suspension of exit for legal representatives in Clause 5, Article 17 of the draft Law inherits the regulation in Clause 1, Article 66 of the current Law on Tax Administration and in practice has been effective in collecting tax debts.

However, in reality, there are many cases where the legal representative of the enterprise is simply a person hired to avoid the temporary suspension of the business owner's exit from the country. Therefore, it is necessary to add the subject "is the beneficial owner of the enterprise" to overcome this situation.

The Minister of Finance explained that the law on enterprises clearly stipulates the criteria for determining beneficial owners of enterprises and that enterprises must notify the provincial business registration authority of information about the beneficial owners of the enterprise.

Accordingly, the beneficial owner of an enterprise is the individual who actually controls the enterprise, has actual ownership of the charter capital or has control over the enterprise even though his/her name is not necessarily on the business registration documents.

Clause 7, Article 17 of the draft Law assigns the Government to detail this Article. Therefore, the application of temporary exit suspension measures for individuals who are beneficial owners of enterprises will be specifically regulated in the Decree to be consistent with the law on enterprises, ensuring transparency in law enforcement.

The Law on Tax Administration passed by the National Assembly today stipulates: At Point a, Point b, Clause 5, Article 17 on completing tax payment obligations, cases must complete tax payment obligations before leaving the country. The Law on Tax Administration amends and supplements cases where enterprises must complete tax obligations before leaving the country.

Including business individuals, business household owners, individuals who are beneficial owners of enterprises, individuals who are legal representatives of enterprises, cooperatives, and cooperative unions who are subject to compulsory enforcement of administrative decisions on tax management and have not fulfilled their tax payment obligations;

Business individuals, business household owners, individuals who are beneficial owners of enterprises, individuals who are legal representatives of enterprises, cooperatives, and cooperative unions that are no longer operating at the registered address and have not fulfilled their tax payment obligations;

Individuals are Vietnamese people leaving the country to settle abroad, Vietnamese people settling abroad, foreigners who have not fulfilled their tax obligations.

The Government prescribes the amount of tax arrears and the debt period according to the threshold for applying the measure of temporary suspension of exit according to the provisions of the law on exit and entry.

Source: https://baohaiphong.vn/bo-sung-doi-tuong-bi-tam-hoan-xuat-canh-neu-doanh-nghiep-vi-pham-thue-529173.html

![[Video] The craft of making Dong Ho folk paintings has been inscribed by UNESCO on the List of Crafts in Need of Urgent Safeguarding.](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/10/1765350246533_tranh-dong-ho-734-jpg.webp)

Comment (0)