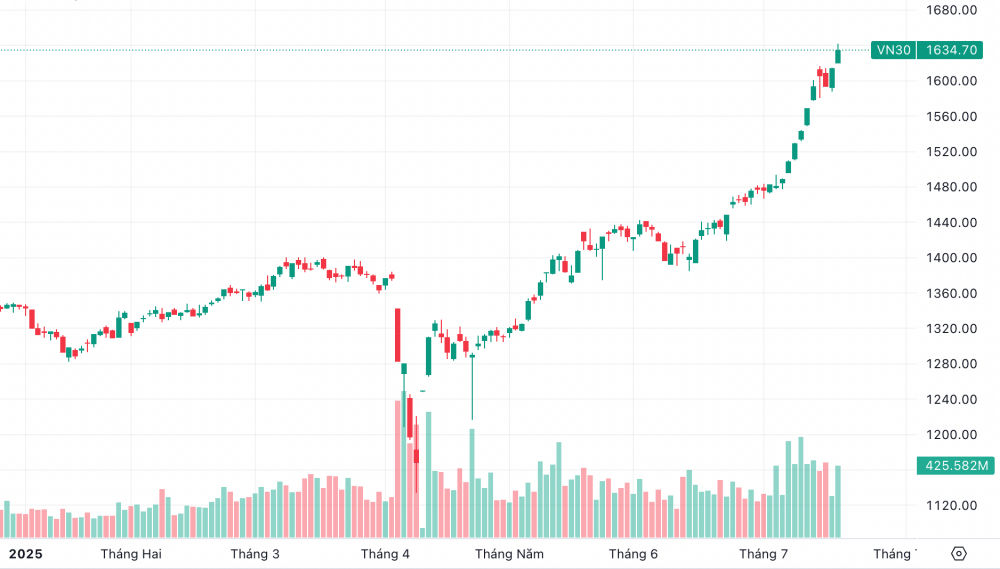

On July 17th, the VN30 index closed at 1,634.7 points, up more than 20 points, equivalent to 1.26%, while the VN-Index reached 1,490 points, up 0.99%. This is the highest point in the history of the VN30.

The top 30 stocks in this market consistently attract buying interest from both domestic and foreign investors.

|

| The VN30 index reached a new peak during the trading session on July 17th. |

Previously, in the first six months of 2025, the growth of the VN-Index was also supported by a number of large-cap stocks.

MB Securities Joint Stock Company (MBS) stated that, as of July 4, 2025, although the VN-Index recovered strongly by more than 300 points since the event on April 2nd, the upward momentum has not spread to all stock classes. Mid-cap and small-cap stocks continue to grow slowly, or even decline in price compared to the increase of the main index.

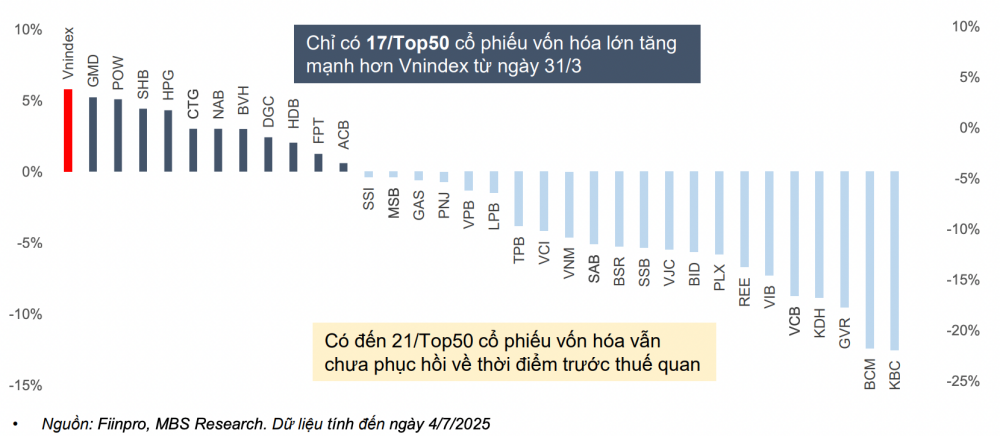

In the large-cap stock group, the biggest contribution mainly comes from the Vingroup group of stocks. Only 12 out of the 50 largest market capitalization stocks have increased more strongly than the VN-Index since March 31, 2025, while about 9 stocks have increased less than the VN-Index. Even nearly half of the Top 50 stocks have not yet recovered to their pre-tariff levels.

|

| Price fluctuations of Top 50 large-cap stocks from March 31 (before the tariff shock) to July 4, 2025. |

According to MBS's assessment, in the context of the announced US tariff policy for Vietnam being more favorable than that of competing countries, and with the prospect of upgrading the Vietnamese stock market becoming clearer, the net selling trend of foreign investors is expected to be strongly reversed in the second half of 2025. The destination of foreign capital will mainly be large-cap stocks with sufficient foreign ownership limits.

As of July 4, 2025, the VN-Index is trading at a P/E ratio of 14 times, higher than the average of the last 3 years (13.5x), but still 17% lower than the 3-year peak (16.9 times in Q4/2021).

The valuation of the VN30 group (with the majority of its market capitalization being in the banking sector) is 12.7 times P/E, approximately 3% higher than the 3-year average of 12.3 times, but still lower than the peak of 15 times in Q4 2021. This indicates that the valuation of the market in general, and large-cap stocks in particular, remains attractive compared to profit growth and expectations of market upgrade.

In the second half of 2025, MBS believes that capital will flow into large-cap stocks that have not seen significant price increases recently, thanks to attractive valuations and potential for profit growth.

In the base scenario, with a 17% increase in profits for listed companies and a P/E ratio of 13.5-13.8 times, this securities firm expects the VN-Index to reach 1,500-1,540 points in the final months of the year.

In a more optimistic scenario, the impact of US tariff policies is less than expected, foreign capital flows strongly into the Vietnamese market thanks to the prospect of an upgrade, market profit growth is expected to reach 19%, the expected P/E ratio is 13.5-14 times, and the VN-Index could advance to the 1,580 point range by the end of the year.

Source: https://baodautu.vn/co-phieu-bluechips---dich-den-cua-dong-tien-ngoai-d334260.html

Comment (0)