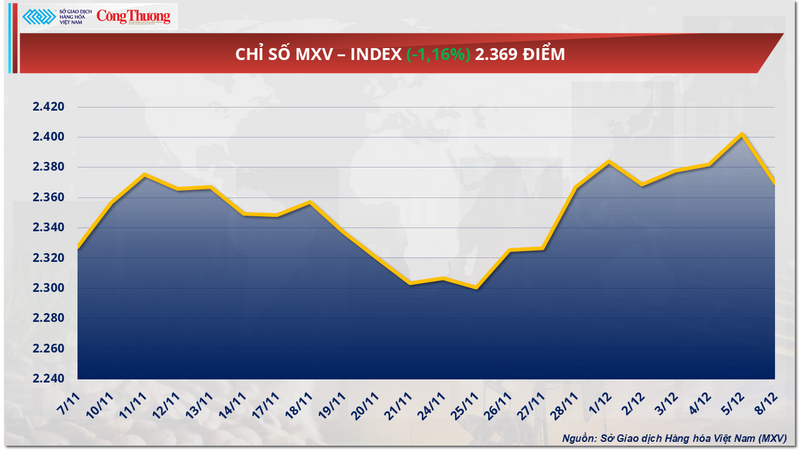

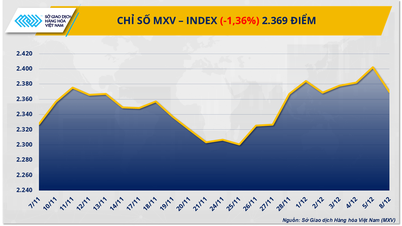

The global commodities market opened the week in the red as selling pressure spread across many sectors. At the close, the MXV-Index fell nearly 1.4% to 2,369 points. In the metals sector, iron ore prices fell for the second consecutive session to $106 per ton, while in the industrial raw materials market, Malaysian palm oil prices also dropped nearly 1.5%.

MXV-Index

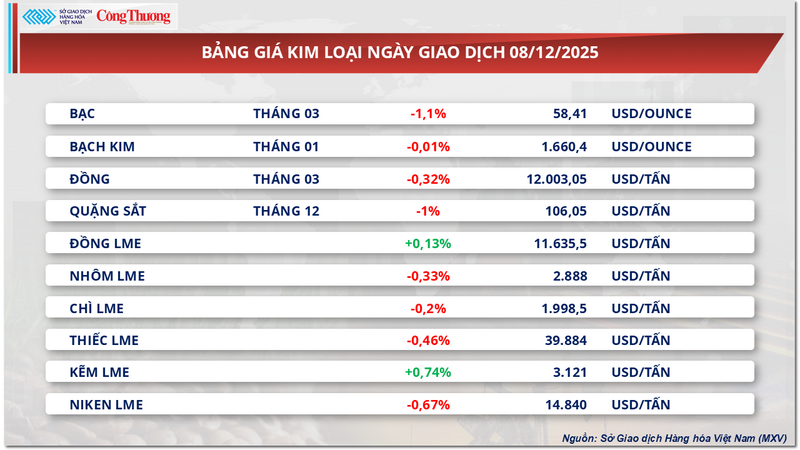

Iron ore prices down 1%

Not outside the general downward trend of the market, the metal group continued to face selling pressure yesterday when iron ore prices fell another 1% to 106.05 USD/ton - the second consecutive session of weakness. This decline occurred right after prices hit a more than one-month high last week. This shows that the previous increase was mainly short-term and was quickly erased when supply and demand signals were less positive.

Metal price list

According to the Vietnam Commodity Exchange (MXV), the easing of concerns about supply shortages is the main factor driving down iron ore prices. The first shipment of 200,000 tons of high-quality ore from the Simandou mine (Guinea) is expected to arrive at Zhejiang port in mid-January next year, and the prospect of the project potentially adding up to 120 million tons per year when fully operational has fueled market expectations of a more abundant supply. In this context, profit-taking following last week's price surge is putting further pressure on prices.

In addition, demand in China - the world's largest consumer market - has not improved. Ore inventories at ports increased to 142.4 million tons, reflecting a slowing consumption pace of steel mills. Crude steel output in October decreased by 12% compared to the same period, pig iron decreased by nearly 7%, while the steel industry PMI index continued to remain below the 50-point threshold, indicating a contraction in production. As the market enters the low consumption period at the end of the year, the prospect of demand recovery in the short term is even more limited.

Export output was also weak, with China’s finished steel output falling 6.5% month-on-month in October and more than 12% year-on-year, as more countries imposed trade barriers, making it harder for the industry to offset weaker domestic demand.

The combination of easing supply, rising inventories and persistently weak downstream demand is putting double pressure on the iron ore market, leaving prices likely to remain at risk of correction in the near term.

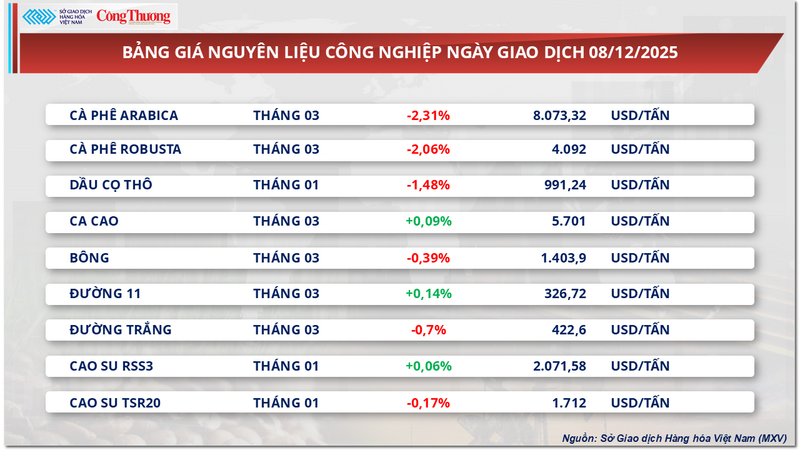

Supply pressure pushes palm oil prices down

At the end of yesterday's trading session, the industrial raw materials group recorded dominant selling pressure with 6 out of 9 items simultaneously weakening. In particular, the price of Malaysian palm oil for January contract lost nearly 1.5%, down to 991.2 USD/ton. MXV commented that the downward pressure on prices mainly came from concerns about excess supply when both production and inventory in Malaysia increased sharply.

Industrial raw material price list

According to data from the Malaysian Palm Oil Association (MPOA), the country’s palm oil production in the period from November 1 to 20 is estimated to have increased by 3.24% compared to the previous month, contrary to the seasonal pattern where output usually declines in November due to the onset of the rainy season. The unexpected increase in supply, amid slowing exports, has pushed inventories to a worrying level as palm oil stocks in October reached 2.46 million tonnes, a record high compared to the same period in many years.

Data from SunSirs also showed that in the first 20 days of November, Malaysia’s palm oil exports fell sharply from 14.1% to 20.5% compared to the previous month. With this weakening momentum, inventories are forecast to continue to expand in November, possibly reaching 2.60–2.70 million tonnes, putting great pressure on prices as supply increases but output shrinks.

In China, weakening import demand for palm oil is limiting the market's recovery potential. SunSirs notes that buying activity for the December contract remains very low, mainly due to unattractive import margins, keeping Chinese importers cautious.

On the other hand, India has emerged as a key support for palm oil prices. The country has sharply cut imports of other vegetable oils due to high prices, with soybean oil imports falling 12% to 400,000 tonnes and sunflower oil falling 44% to a two-year low of 145,000 tonnes. However, palm oil imports in November rose to 630,000 tonnes, 4.6% higher than October, thanks to price competitiveness.

In addition, on the supply side from Indonesia, the market received a reassuring signal from natural disaster concerns. The Indonesian Palm Oil Association (GAPKI) affirmed that the recent severe floods and landslides on Sumatra island will not have a significant impact on the country's palm oil production in 2025. GAPKI Chairman Eddy Martono said that so far only one company in Aceh Tamiang had to temporarily stop production to repair a tank, while key areas such as West Sumatra and North Sumatra have not recorded any disruptions at plantations, although transport infrastructure to Aceh port is still being repaired. This information helps to ease concerns about the risk of disruption to the supply chain from the world's largest palm oil producer.

Price list of some other goods

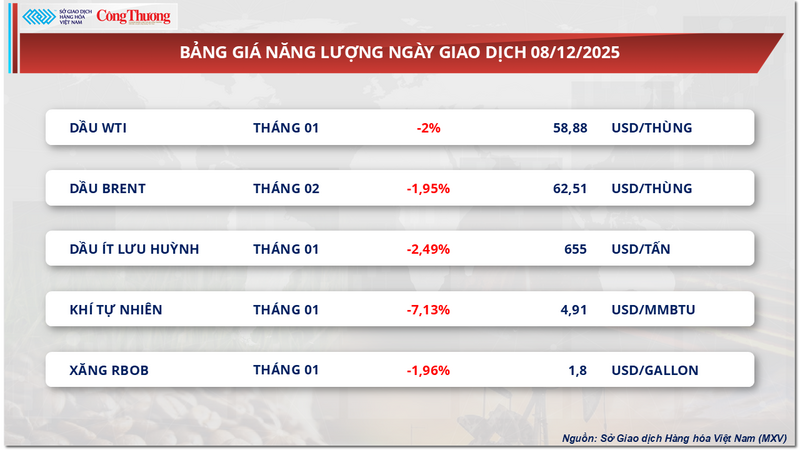

Energy price list

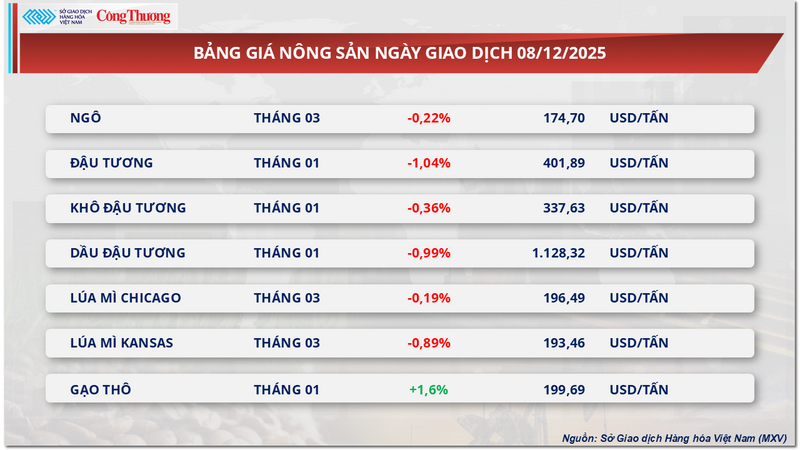

Agricultural product price list

Source: https://congthuong.vn/gia-quang-sat-buoc-sang-phien-giam-thu-hai-lien-tiep-433941.html

![[Video] The craft of making Dong Ho folk paintings has been inscribed by UNESCO on the List of Crafts in Need of Urgent Safeguarding.](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/10/1765350246533_tranh-dong-ho-734-jpg.webp)

Comment (0)