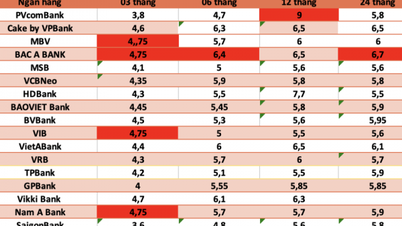

State Bank data shows that total system deposits by the end of September 2025 reached nearly VND16.2 million billion, of which deposits of

economic organizations increased sharply.

Specifically, the deposits of economic organizations (enterprises) by the end of September 2025 reached VND 8.35 million billion. Thus, after a sharp decrease in July 2025, corporate deposits increased to VND 374,000 billion in August and September. The growth of corporate deposits by the end of September 2025 reached 8.91%.

Residential deposits increased more slowly in August and September but still reached a new record: VND 7.83 trillion, up 10.9% compared to the beginning of the year. By the end of September 2025, residential deposits had increased by VND 767 trillion compared to the beginning of the year (August and September alone increased by VND 84 trillion compared to the end of July).

Total means of payment (money supply) also increased accordingly, reaching nearly 20 million billion VND at the end of September, an increase of 11.53% compared to the beginning of the year.

Also according to the State Bank of Vietnam, by the end of September 2025, the total credit of the whole system increased by 13.86%, reaching a scale of 17.78 million billion VND. Thus, in the first 9 months of the year, capital mobilization was lower than the outstanding credit balance by 1.6 million billion VND.

The fact that credit is growing faster than capital mobilization is causing some concerns in the context that

the Prime Minister has directed the State Bank to pilot removing the credit growth ceiling from 2026.

Sharing with the Investment Electronic Newspaper - Baodautu.vn, Prof. Dr. Tran Ngoc Tho (Ho Chi Minh City University of Economics) raised three questions: First, to what extent do we accept the dependence on bank credit in exchange for nominal growth? Second, is the current credit allocation structure supporting or eroding the long-term productivity foundation? Third: Should the increasing dependence on long-term OMO and the interbank market be considered the new normal or a sign of adjustment?

According to Prof. Dr. Tran Ngoc Tho, on the surface, the increase in credit, the increase in LDR ( credit balance ratio to mobilized capital of banks) , the improvement in bank profits, flexible OMO and high GDP growth are a positive picture. But on a deeper level, this picture also shows that the capital base is thinner than the credit scale, the allocation structure is still inclined towards real estate assets and the role of the State Bank in supporting medium-term liquidity is increasing.

This is not a warning, nor is it a statement that the risk is close to breaking point. It is a suggestion that, rather than arguing further about whether credit should increase by 15% or 18%, perhaps the more important question is how much real productivity each new dollar of credit is actually buying for the economy and how much is being used quietly to buy time to deal with old bottlenecks.

If the answer in the next few years is the latter, then today’s liquidity pressure may just be an early sign of a larger problem with the quality of growth. If the system takes advantage of this credit boom to re-allocate capital and boost productivity, then the current numbers will be seen as a necessary shift. It depends on how we choose to use the credit channel as a temporary bridge to overcome a short-term difficulty, or as a long-term foundation for the growth path ahead.

Source: https://baodautu.vn/chenh-lech-huy-dong-va-cho-vay-da-vuot-16-trieu-ty-dong-d444642.html

![[Photo] Cat Ba - Green island paradise](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F04%2F1764821844074_ndo_br_1-dcbthienduongxanh638-jpg.webp&w=3840&q=75)

![[VIMC 40 days of lightning speed] Da Nang Port: Unity - Lightning speed - Breakthrough to the finish line](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/04/1764833540882_cdn_4-12-25.jpeg)

Comment (0)