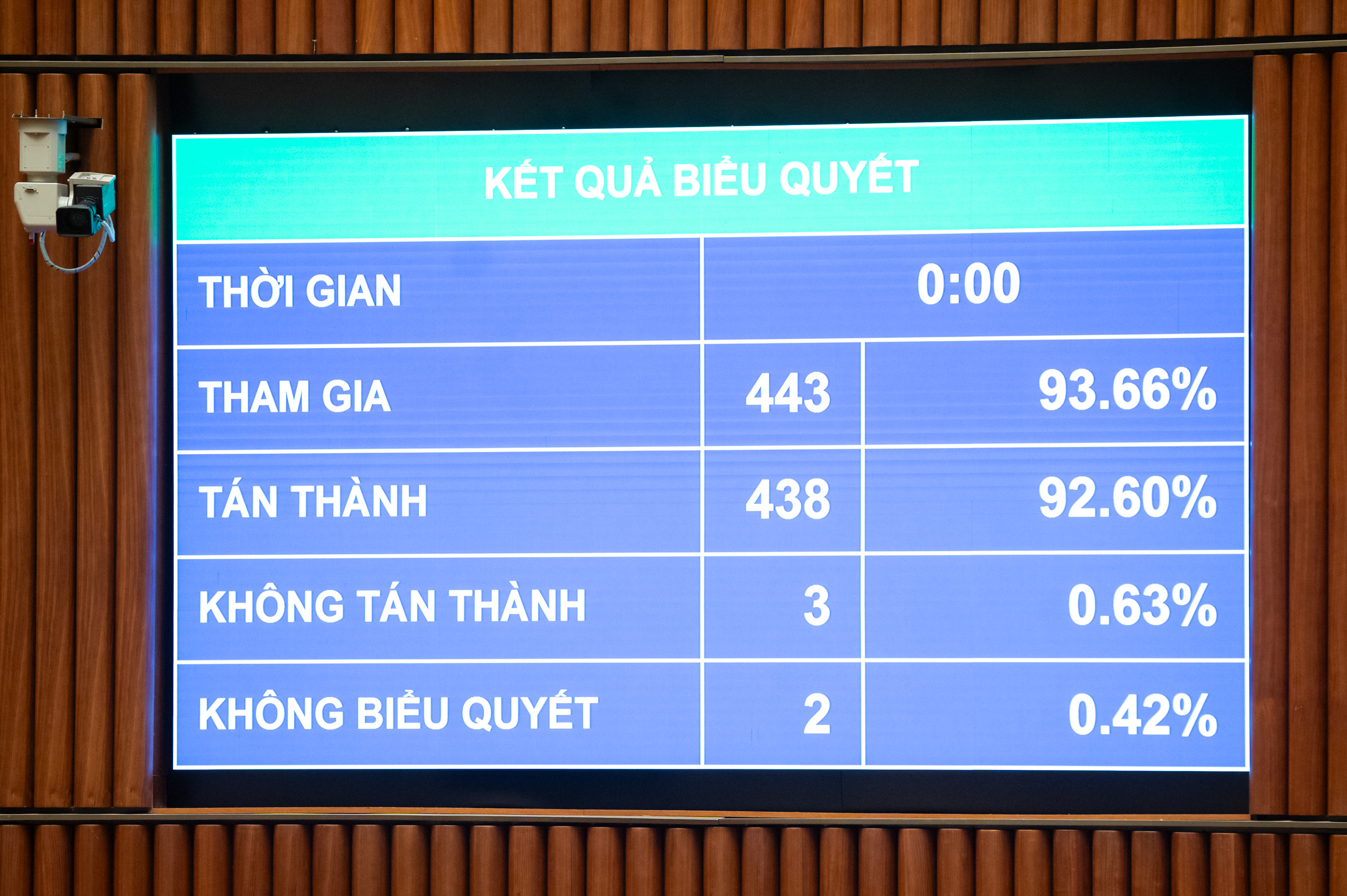

Voting to pass the Law on Personal Income Tax - Photo: P.THANG

The law, passed with 30 articles and effective from July 1, 2026, regulates taxpayers and taxable income of individuals, including income from business activities, salaries, wages, capital investments, capital transfers, real estate transfers, lottery winnings, royalties, franchise fees, inheritance, gifts of securities and capital shares, and other income such as transfers of digital assets and gold bars.

In which cases is tax-exempt?

Tax exemptions apply to the following cases: income from the transfer, inheritance, or gift of real estate; transfer of housing, land use rights, and assets attached to residential land by individuals in cases where the individual owns only one house and one plot of land; and income from the value of land use rights granted to individuals by the State.

Income of households and individuals directly engaged in the production of crops, planted forests, livestock, aquaculture, and fishing products that have not been processed into other products or have only undergone basic processing; salt production; conversion of agricultural land allocated by the State; interest on government bonds, local government bonds, and deposits; remittances; night shift and overtime pay; pensions; scholarships, etc.

It is noteworthy that the law passed specifically stipulates personal income tax for business income with annual revenue of 500 million VND or less, which is not subject to tax.

In case an individual business has an annual revenue of over 500 million to 3 billion VND, the tax rate will be 15%; from over 3 billion VND to 50 billion VND, the tax rate will be 17% and revenue over 50 billion VND will be subject to a tax rate of 20%.

Before the law was passed, Minister of Finance Nguyen Van Thang said that he had accepted the opinions of National Assembly deputies and adjusted the tax-free revenue of business households and individuals from 200 million VND/year to 500 million VND/year and deducted this amount before calculating tax based on the revenue rate. At the same time, he adjusted the revenue not subject to value added tax to 500 million VND.

In addition, add a method of calculating tax on income (revenue - expenses) for households and individuals doing business with revenue from over 500 million VND/year to 3 billion VND and apply a tax rate of 15% (similar to the corporate income tax rate for businesses with revenue under 3 billion VND/year); stipulate that these individuals can choose the method of calculating tax based on the rate on revenue.

Minister of Finance Nguyen Van Thang - Photo: P.THANG

Tax on real estate transfers and gold bars

Regarding the family deduction for taxpayers, it is adjusted to 15.5 million VND/month (equivalent to 186 million VND/year); the deduction for each dependent is 6.2 million VND/month. Accordingly, based on fluctuations in prices and income, the Government will submit to the National Assembly Standing Committee to prescribe the family deduction level in accordance with the socio -economic situation in each period.

Determining the personal allowance for dependents follows the principle that each dependent can only be claimed as a deduction once by one taxpayer.

Resident individuals are entitled to deductions from taxable income before calculating tax on income from salaries, wages, charitable and humanitarian contributions; and expenses for health care, education and training of taxpayers and dependents.

In addition, the passed law also specifically stipulates personal income tax on income from real estate transfers. Specifically, this tax rate is determined by multiplying the transfer price (x) by the tax rate of 2%. The time to determine taxable income from real estate transfers is the time the transfer contract takes effect according to the provisions of law or the time of registration of the right to use or own the real estate.

Regarding the proposal to collect tax on gold transfers, the Minister of Finance said that this content has been carefully reviewed and researched, based on synthesizing opinions from agencies, and absorbing opinions.

Accordingly, the law stipulates a tax on gold bars at a rate of 0.1% on the transfer price for each transaction. The government is tasked with setting the tax threshold, the timing of collection, and adjusting the tax rate in accordance with the roadmap for managing the gold market.

According to Mr. Thang, the government's role in regulating gold aims to exclude individuals who buy and sell gold for savings and safekeeping purposes (not for business). Because this is a new regulation with a wide impact, it is a necessary step to implement the Party and State's directive on strictly managing gold trading activities, contributing to limiting gold speculation and attracting social resources to participate in the economy.

Source: https://tuoitre.vn/chinh-thuc-ap-thue-giao-dich-bat-dong-san-vang-mieng-nguong-chiu-thue-ho-kinh-doanh-la-500-trieu-20251210093257967.htm#content-1

![[Photo] Closing Ceremony of the 10th Session of the 15th National Assembly](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F11%2F1765448959967_image-1437-jpg.webp&w=3840&q=75)

![[OFFICIAL] MISA GROUP ANNOUNCES ITS PIONEERING BRAND POSITIONING IN BUILDING AGENTIC AI FOR BUSINESSES, HOUSEHOLDS, AND THE GOVERNMENT](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/11/1765444754256_agentic-ai_postfb-scaled.png)

Comment (0)