In Ho Chi Minh City, projects such as the International Financial Center, the metro, and the Ben Luc - Long Thanh expressway are creating a major impetus for the development of satellite cities.

Recovery but strong differentiation

The period 2022–2025 clearly shows the market's lag in response to interest rate shocks. In 2022, the real estate market was volatile, and liquidity declined. By 2025, although interest rates edged up towards the end of the year, the picture had brightened: transactions stabilized, prices increased in areas with genuine housing demand, and real estate was benefiting from infrastructure development.

This information was presented at the Vietnam Real Estate Conference – VRES 2025, organized by PropertyGuru Vietnam in Ho Chi Minh City on December 11-12. In an interview with VTV Times on the sidelines of the conference, experts stated that in 2026, Vietnam is projected to become a destination for FDI capital and a new manufacturing hub in the region. Residential real estate, especially that serving genuine housing needs, will become a crucial part of the "soft infrastructure" in the supply chain. If factories and industrial parks are the engine of production, then housing is what retains the workforce and experts.

Money is flowing back into products that meet genuine housing needs, aligning with the expansion of the middle class.

Mr. Dinh Minh Tuan, Director of PropertyGuru Vietnam's Southern Region, believes that the market will enter a recovery phase in 2025, but with strong differentiation. Data from PropertyGuru Vietnam shows that interest levels in Q4 2025 nationwide increased compared to Q1 2023, especially in areas with good infrastructure connectivity. This indicates that capital flows are becoming more selective and directed towards areas that meet sustainable development criteria, a strategy also used by multinational corporations when expanding their supply chains.

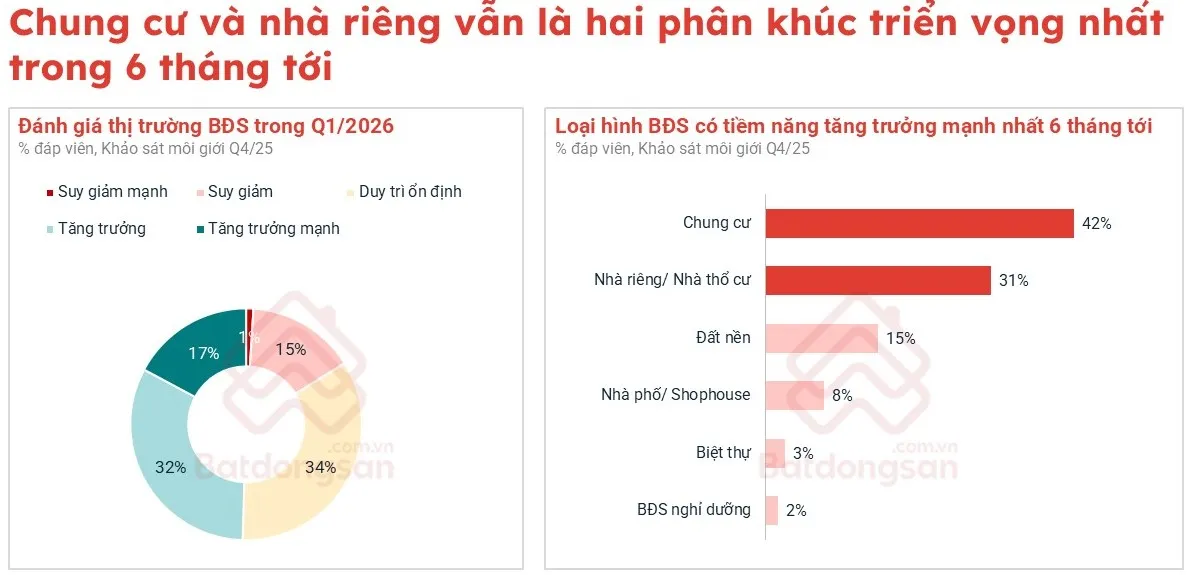

The Q4 2025 real estate brokerage survey reflects a clear divergence: 48% reported a decrease in transactions, 14% an increase, and 35% remained stable. However, apartments emerged as a strong performer, with 37% of brokers reporting an increase in transactions; detached houses also maintained momentum, with 26% reporting an increase and over half the market remaining stable. Conversely, land plots and villas, which are often considered speculative, both cooled down, while townhouses experienced a slowdown.

These figures indicate that capital is flowing back into products that meet genuine housing needs, aligning with the expansion of the middle class and the demand for stable settlements associated with new production hubs. Most brokers believe that in the next six months of 2026, apartments and detached houses will continue to lead the market. This forecast is consistent with Vietnam's development trends within the global supply chain.

Bright doors for apartments and townhouses.

In Hanoi , infrastructure, particularly the ring road system and river bridges, is reshaping the real estate landscape. According to PropertyGuru Vietnam, the number of apartment projects along the ring roads has increased from 269 projects before 2015 to nearly 700 projects currently, a nearly 2.6-fold increase. The focus is shifting towards ring roads 2 and 3. In the first 11 months of 2025, Nam Tu Liem (formerly) led in terms of interest in apartments, followed by Ha Dong, Cau Giay, and Hoang Mai.

Prices also saw impressive surges in areas benefiting from infrastructure development. Thanh Tri (formerly) reached VND 74 million/m2, a 158% increase compared to Q1 2023; Gia Lam (formerly) reached VND 80 million/m2 and Ha Dong (formerly) reached VND 75 million/m2, both increasing by 143%; Hoai Duc (formerly) increased by 139%. This increase far surpasses that of central districts like Ba Dinh or Hai Ba Trung (formerly), which only increased by 69–92%. This reflects the market trend towards new mega-cities with convenient regional connectivity, important "transit hubs" for the supply chain in the northern region.

Despite decreased interest in the private housing segment in Hanoi, prices increased in most districts, especially Ha Dong, Hoang Mai, Bac Tu Liem, and Long Bien (formerly), where asking prices rose by over 110% compared to Q1 2023. This demonstrates the resilience of land-attached properties in gateway areas that connect industrial and urban hubs.

Another notable signal is the shift in demand. The percentage of Hanoi residents searching for real estate within the capital city decreased from 81% (Q1 2023) to 59% (Q4 2025), while interest in Ho Chi Minh City increased from 6% to 20%. Provinces such as Hung Yen, Bac Ninh , and Quang Ninh also saw significant increases. This represents a "multipolarization" trend in living spaces, aligning with the shift in the workforce within the expanding supply chain model.

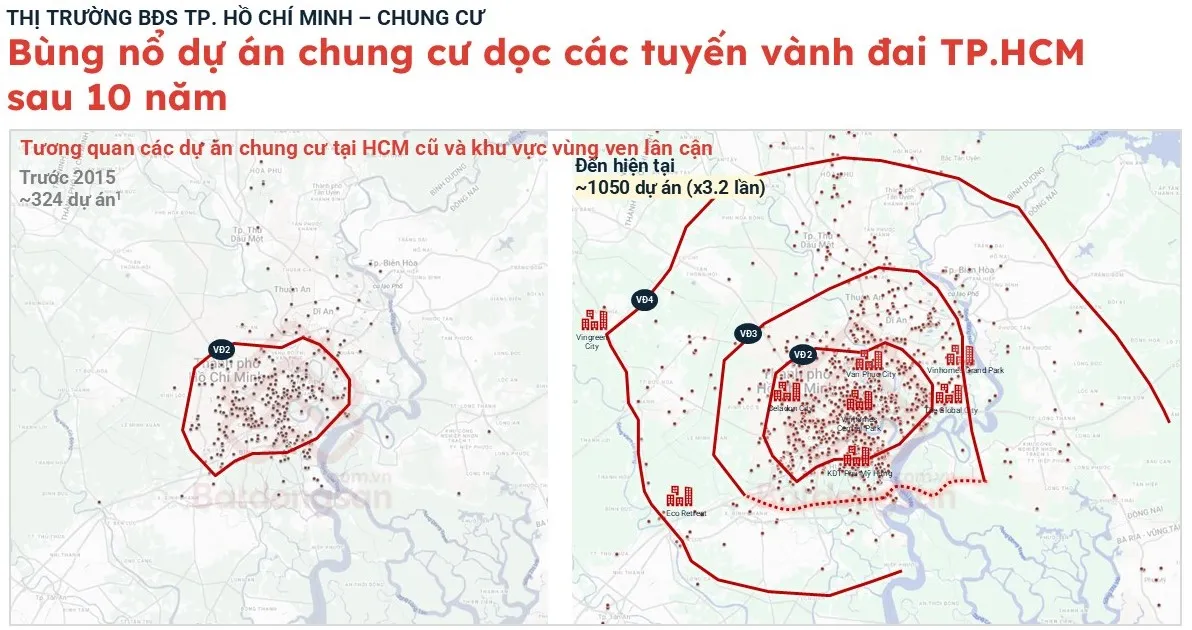

The supply of apartments in Ho Chi Minh City has boomed: from 324 projects before 2015 to approximately 1,050 projects currently, a 3.2-fold increase.

In Ho Chi Minh City, inter-regional infrastructure, the metro, the Ben Luc - Long Thanh expressway, and the bridge to Dong Nai are strongly promoting the rise of satellite cities such as Thuan An, Di An, and Vung Tau (formerly). The eastern area and the area bordering Binh Duong (formerly) are becoming focal points for recovery.

The supply of apartments in Ho Chi Minh City has boomed: from 324 projects before 2015 to approximately 1,050 projects currently, a 3.2-fold increase, and a strong shift towards the Northeast. Many areas have recorded price increases of 32–48% compared to Q1/2023.

The demand for apartments in Thuan An, Di An, and Thu Dau Mot (formerly Binh Duong) increased by 129%, 103%, and 65% respectively in the first 11 months of 2025, demonstrating the strong appeal of these border areas. As Mr. Dinh Minh Tuan noted: "The city center no longer holds the sole central role," as the ring roads create new development hubs such as Thu Duc, Nha Be, Thuan An, and Di An…

The private housing segment in Ho Chi Minh City remains stable, with prices in the central area reaching 210 to 286 million VND/m2, 1.4–2.2 times higher than apartments. In Binh Thanh, Phu Nhuan, District 11, and District 7 (formerly), prices have decreased to 125–204 million VND/m2. In suburban areas and Thu Duc City (formerly), private houses are only 1.1–1.8 times more expensive than apartments, creating room for price increases in the next cycle.

Street-front properties saw a slight recovery in sales, although interest decreased by 5%. District 2 (formerly) emerged as a bright spot thanks to competitive pricing and better yields compared to traditional central districts.

All the data above suggests that 2026 will be a period of selective recovery, where apartments and townhouses in growth poles, where infrastructure converges, meeting genuine housing demand and providing quality supply, will play a leading role. In a cycle where Vietnam is leaping up the global supply chain map, real estate is no longer a "speculative game," but a strategic equation concerning living and production spaces. Only those who correctly interpret the data and understand the role of apartments and townhouses in this new development structure will be able to "win" the market.

Source: https://vtv.vn/thi-truong-bds-2026-chung-cu-nha-lien-tho-dan-song-100251211161709143.htm

![[Photo] Closing Ceremony of the 10th Session of the 15th National Assembly](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F11%2F1765448959967_image-1437-jpg.webp&w=3840&q=75)

![[Photo] Prime Minister Pham Minh Chinh holds a phone call with the CEO of Russia's Rosatom Corporation.](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F11%2F1765464552365_dsc-5295-jpg.webp&w=3840&q=75)

![[OFFICIAL] MISA GROUP ANNOUNCES ITS PIONEERING BRAND POSITIONING IN BUILDING AGENTIC AI FOR BUSINESSES, HOUSEHOLDS, AND THE GOVERNMENT](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/11/1765444754256_agentic-ai_postfb-scaled.png)

Comment (0)