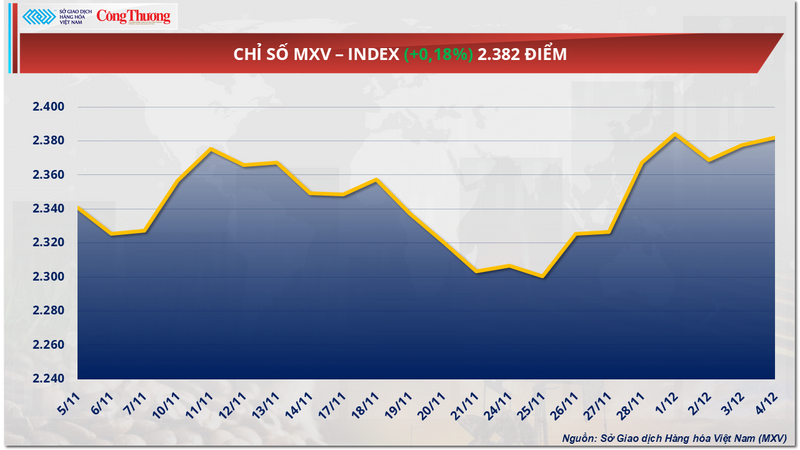

Green continued to prevail in the world raw material market in yesterday's trading session (December 4). The market's focus was on coffee and crude oil as prices of these commodities increased sharply. At the close, the MXV-Index increased by nearly 0.2% to 2,382 points.

MXV-Index

Coffee prices recover strongly

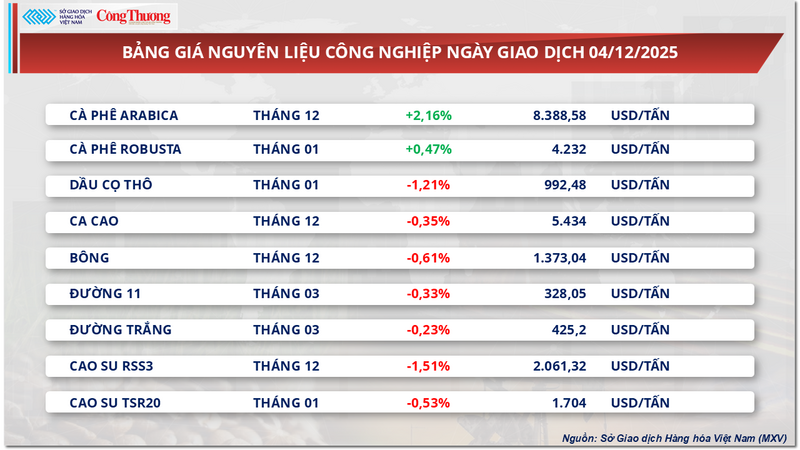

Closing yesterday's trading session, the industrial raw materials market witnessed red covering most of the commodities in the group. In particular, two coffee commodities became bright spots when going against the general trend of the whole group. Specifically, the price of Arabica coffee recorded an impressive increase of more than 2.1% to 8,388 USD/ton, while the price of Robusta coffee also increased by nearly 0.5% to 4,232 USD/ton.

Industrial raw material price list

According to the Vietnam Commodity Exchange (MXV), the rise in Arabica coffee prices is strongly supported by the shortage of supply from Brazil. The country's export increase in 2024 to a record 50.5 million bags has put the country's domestic inventories in a significantly limited state. Data from the Ministry of Development, Industry, Trade and Services (MDIC) shows that in the first 10 months of the year, Brazil exported only about 34.2 million bags, down 17.8% compared to the same period in 2024, further strengthening the price increase.

Meanwhile, Conab said that after the harvest in Brazil ended in September, Minas Gerais, the largest coffee-producing state, recorded 25.17 million bags of Arabica, down 9.2% from the previous season, due to the unfavorable biennial cycle and a long period of drought before flowering. In São Paulo, production fell 12.9% to an estimated 4.7 million bags, due to the biological impact of the low cycle and adverse climatic conditions such as drought and high temperatures.

Arabica coffee prices increased by an impressive 2.1% to $8,388/ton, while Robusta coffee prices also increased by nearly 0.5% to $4,232/ton. Illustrative photo

Climatempo forecasts that drought and high temperatures will continue to grip Brazil’s main coffee growing regions next week. Farmer Rafael Stefani in the Alta Mogiana region expressed concern that the combination of lack of rain and intense heat will negatively impact the ripening process of the fruit, threatening the quality of the 2026 crop.

In addition, the global Robusta supply picture is still full of concerns as the weather situation in Vietnam remains extremely complicated. Prolonged heavy rains causing widespread flooding in the Central Highlands are seriously affecting the progress and quality of the crop. Although farmers have harvested 50%-60% of the output, storms and rains have made drying difficult and many fruits have fallen. Market sources estimate that storms and floods could reduce Vietnam's coffee output by about 5% to 10%.

In the domestic market on December 4, 2025, the finished coffee market recorded a price decline, in line with the general trend of the whole market. The main reason comes from the increase in supply thanks to the new harvest, while purchasing power is still quite weak and scattered. The price of R2 coffee (screen 13, black and broken rate 5%) has decreased sharply, currently trading around 104,000 - 104,500 VND/kg.

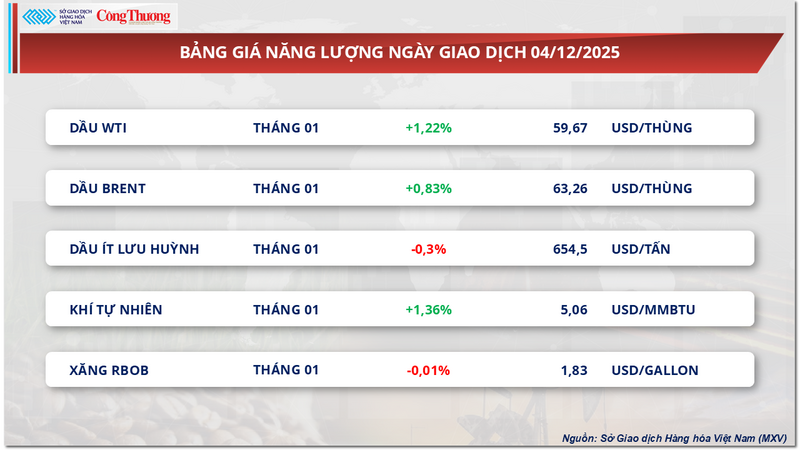

Oil prices continue to recover on expectations that the Fed will cut interest rates.

Meanwhile, according to MXV, yesterday's energy market recorded a dominant buying force with 3 out of 5 commodities increasing in price. Of which, WTI oil price increased by more than 1.2% to 59.6 USD/barrel; Brent oil price also increased by more than 0.8% to 63.2 USD/barrel.

Energy price list

The bullish sentiment in the oil market emerged as US economic data showed the country's labor market continued to weaken, thereby raising expectations of the US Federal Reserve (Fed) to cut interest rates in the near future. The US dollar's 10th consecutive decline - the longest losing streak in years - made oil cheaper for buyers using other currencies, thereby supporting demand for the commodity.

On the geopolitical front, unfavorable news from Russia continues to have a strong impact on the world oil market. In that context, Ukraine has continuously attacked Russian oil and gas facilities, including the Druzhba pipeline and the infrastructure of the Caspian Pipeline Consortium (CPC), raising concerns about the possibility of supply disruption from the Black Sea region.

The Ukrainian drone attack on the CPC loading facility in the Black Sea had immediate consequences. Kazakhstan’s oil and condensate production fell by 6% in the first two days of December, to 1.9 million barrels per day. The decline was particularly worrying because CPC handles more than 80% of Kazakhstan’s total oil exports, or more than 1% of global supply. Although operations have since resumed with one anchor point instead of the usual two, the incident still poses a significant risk of supply disruption to the global oil market.

In addition, information from the two groups, OPEC and OPEC+, also supported oil prices when investors said that OPEC production in November decreased slightly to 28.40 million barrels/day. Although the OPEC+ group agreed to increase production, many members of the group encountered problems, causing actual production to increase by only 40,000 barrels/day, much lower than the expected level of 85,000 barrels/day. This reflects the limitations in production capacity of many countries and the complexity in offsetting production. Meanwhile, Saudi Arabia lowered the official selling price of Arab Light in January to a five-year low, showing that OPEC is well aware of competitive pressure and weakening demand in the market.

However, concerns about global oversupply continue to restrain oil prices. The US Energy Information Administration (EIA) reported that US crude oil inventories increased by 574,000 barrels in the week ending November 28, contrary to forecasts for a decrease. Notably, gasoline and distillate inventories also recorded a sharp increase, in the context of US oil refining capacity reaching 94.1%, indicating continued expansion of supply. At the same time, seasonal demand has shown signs of cooling, creating a mismatch between supply and demand. Fitch Ratings has lowered its oil price forecast for the period 2025-2027, emphasizing that the prospect of global oversupply remains the main risk to oil prices in the near term.

Price list of some other goods

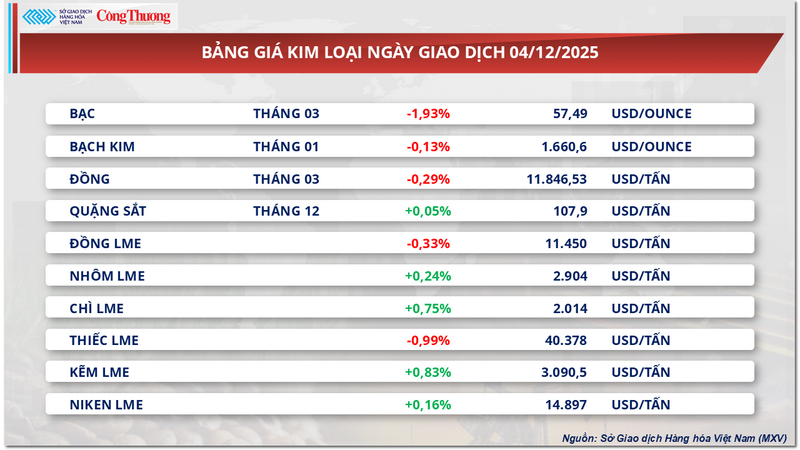

Metal price list

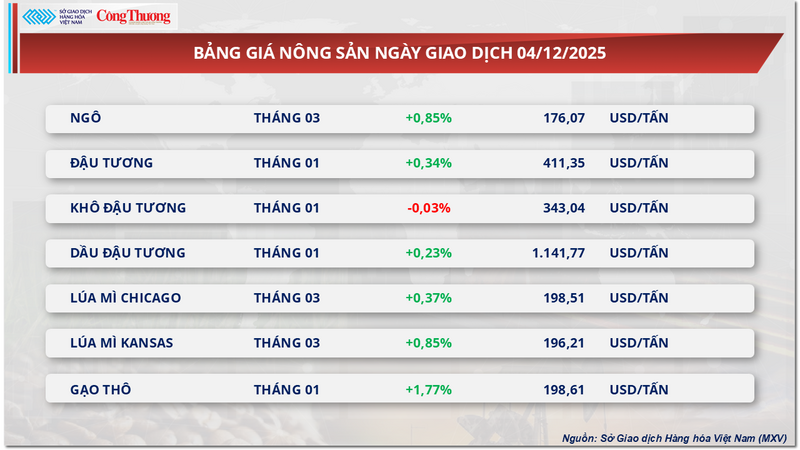

Agricultural product price list

Source: https://congthuong.vn/the-gioi-ca-phe-giao-chieu-tang-khi-nguon-cung-tu-brazil-suy-giam-433438.html

![[Photo] National Assembly Chairman Tran Thanh Man attends the VinFuture 2025 Award Ceremony](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F05%2F1764951162416_2628509768338816493-6995-jpg.webp&w=3840&q=75)

![[Photo] 60th Anniversary of the Founding of the Vietnam Association of Photographic Artists](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F05%2F1764935864512_a1-bnd-0841-9740-jpg.webp&w=3840&q=75)

Comment (0)