The US economy is growing faster than expected.

On October 26, the US Department of Commerce announced that gross domestic product (GDP) grew by 4.9% in the third quarter of 2023, higher than the 4.7% forecast by experts participating in a Dow Jones survey and also higher than the 2.1% growth in the second quarter.

This is the sharpest increase since the fourth quarter of 2021, despite soaring interest rates and other headwinds. Since March 2022, the US Federal Reserve (Fed) has raised its benchmark interest rate 11 times, bringing the federal funds rate to a 22-year high of 5.25%-5.5%. Surprisingly, the US economy continues to grow quite strongly.

The main drivers of economic growth in the third quarter of 2023 came from consumer spending, exports, household investment, and government spending. Consumer spending on goods increased by 4.8%, while spending on services increased by 3.6%. This was the strongest increase in consumer spending since 2021.

The US economic growth was a surprise, as many economists had previously predicted that the US could face at least a mild recession given the dwindling government aid from the Covid era and soaring interest rates over the past year.

The US economy continues to grow even though the Fed is not only raising interest rates at a very rapid pace but also signaling that it will keep interest rates high for an extended period.

With impressive economic growth and a sharp rise in US core inflation in September (+0.3%), the Fed is highly likely to raise interest rates for the 12th time at its meeting next week.

Earlier, at a meeting in mid-October, Chairman Jerome Powell said the Fed was ready to raise interest rates again if the economy overheated. This statement came as the yield on 10-year US Treasury bonds exceeded 5%.

Not only the US, but Europe is also maintaining a tough stance on monetary policy. Some experts told Reuters that the European Central Bank (ECB) is unlikely to ease monetary policy anytime soon. At the earliest, the ECB might reverse its policy in July 2024.

Inflation in the Eurozone remains at double the target. Meanwhile, the Israel-Hamas conflict risks driving up energy prices. The crisis in the region's bond markets will also make EU policymakers cautious.

The strengthening USD is putting significant pressure on most Asian currencies. On October 26th, the Japanese yen crossed the 150 yen/USD warning threshold, its lowest level in over a year. This is considered a "dangerous" zone that could trigger intervention from the Japanese government.

Significant pressure on the Vietnamese economy.

It can be seen that whenever the US faces difficulties, it tends to inject a large amount of USD into the market. To revive the economy after the Covid period, the US injected a large amount of money through quantitative easing (EQ) policy.

This is also a general trend in many countries. Countries are also injecting a large amount of money into the economy. Along with geopolitical conflicts, inflation has risen sharply. This is also when countries are forced to withdraw money to control inflation and exchange rates.

For the US, high economic growth and a robust labor market provide the basis for the Fed to continue tightening monetary policy.

Meanwhile, many Asian economies, including Vietnam, are facing difficulties as there is little room left for loose monetary policy, while the USD/VND exchange rate continues to rise.

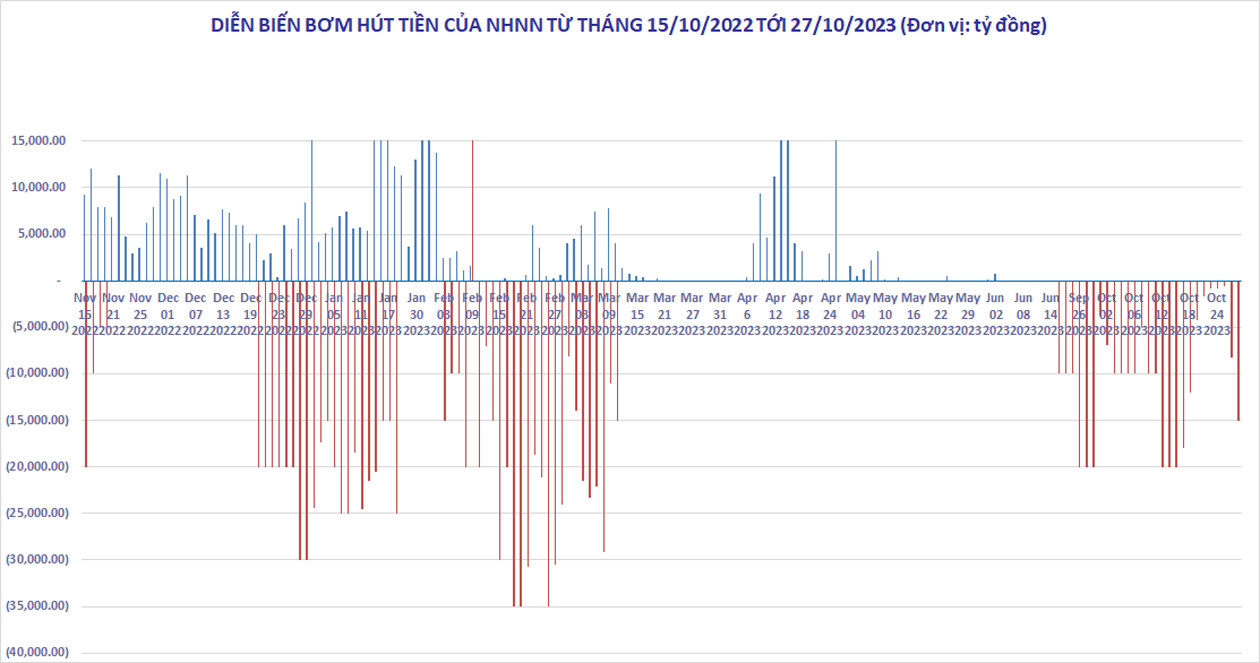

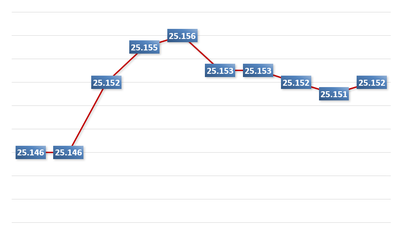

Since mid-October, the USD/VND exchange rate has risen sharply and shows no signs of falling, even though the State Bank of Vietnam has aggressively withdrawn money from the open market for five weeks. As of October 27th, the central exchange rate was 24,107 VND, only 3 VND lower than the historical peak of 24,110 VND/USD recorded on October 20th.

Most banks are currently quoting the USD selling price at 24,730-24,760 VND/USD. This is the highest level since the beginning of the year and only slightly lower than the historical peak of 24,888 VND/USD recorded on October 25, 2022.

On October 27th, the State Bank of Vietnam (SBV) withdrew nearly 11,200 billion VND from the open market to prevent the USD/VND exchange rate from rising. Since September 21st, the SBV has withdrawn a total of approximately 193,000 billion VND.

Withdrawal of money is inevitable as the US continues to tighten monetary policy and Europe continues to aggressively combat inflation. However, if the State Bank of Vietnam continues to aggressively withdraw money to control exchange rates and inflation, commercial interest rates will rise again. This could affect the government's efforts to revive economic growth and real estate businesses, which have yet to recover from the shock of 2022.

Agriseco Securities and ACB Securities have recently both suggested that the USD/VND exchange rate will face upward pressure in the coming period as the Fed forecasts an interest rate hike in November while Vietnam maintains low interest rates. It is highly likely that the State Bank of Vietnam will have to implement additional measures such as selling forward USD contracts to banks.

For now, the USD is still edged up. On October 27th, the DXY index rose to 106.6 points, up 0.4% over the past week, after the US announced strong economic growth.

The recent Israel-Hamas conflict could cause global inflation to rise in line with oil prices. Continuing high inflation could lead the US to prolong its tight monetary policy. The USD will remain a safe haven and continue to appreciate. The US dollar is expected to remain overbought, negatively impacting global financial markets, including Vietnam.

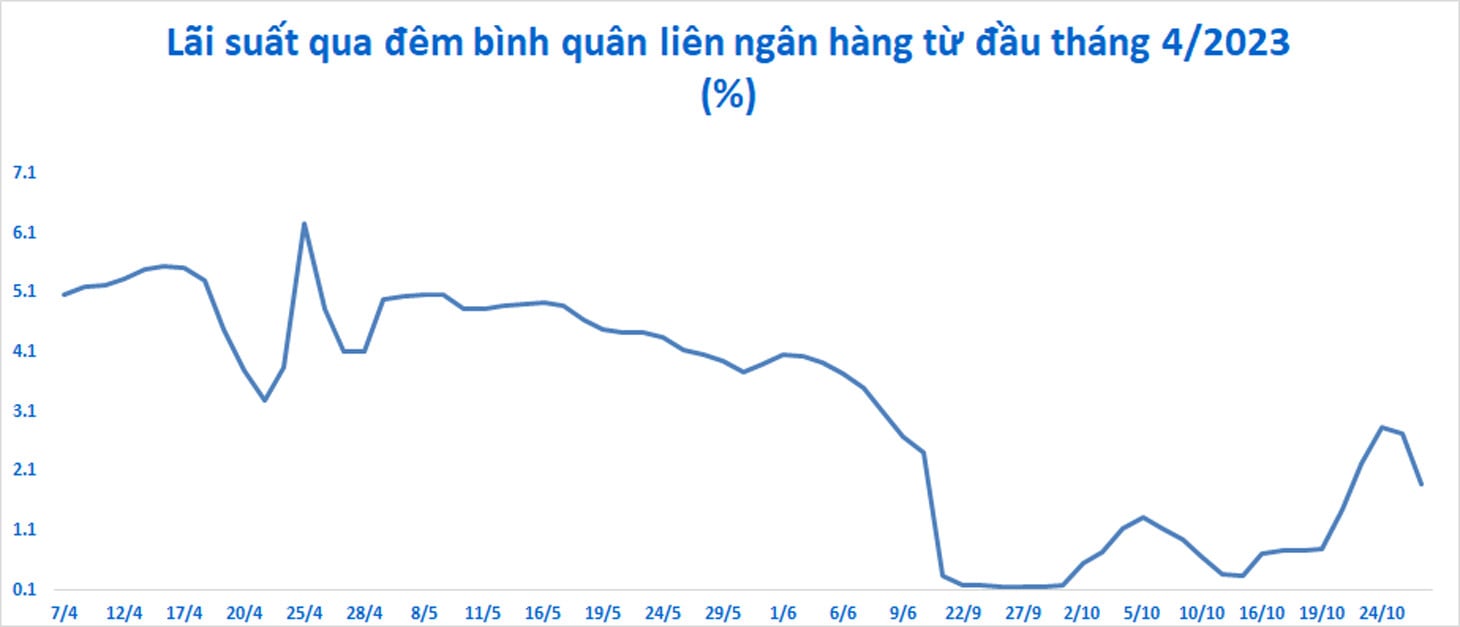

In the interbank market, interest rates have recently risen sharply again (at times reaching 2.84% per annum for overnight rates), and money is no longer cheap in the secondary market. This makes it difficult for Vietnam to lower interest rates to support economic growth, even though credit growth remains very low and real estate and manufacturing businesses are struggling with high financing costs.

Source

![[Infographic] Cross-exchange rates for determining taxable value from December 11-17](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/11/1765413245543_infographic-ty-gia-tinh-cheo-de-xac-dinh-tri-gia-tinh-thue-tu-11-1712-20251211021920.jpeg)

Comment (0)