|

MXV data shows that at the end of the last trading week, the world raw material market continued to fluctuate. At the end of the week (January 19), the agricultural product price list was in red, while the prices of many industrial raw material products increased. The MXV-Index decreased by 0.4% to 2,099 points.

The US stock market was closed for Martin Luther King Day at the beginning of last week, trading value dropped sharply but was active again shortly after. The average trading value remained at over VND4,600 billion per day.

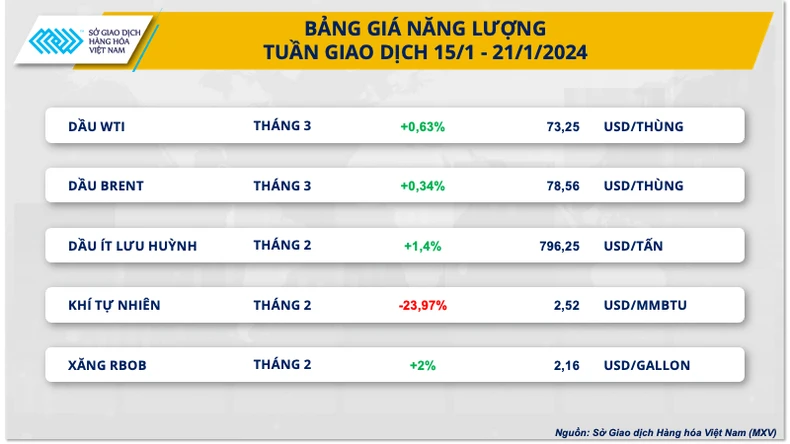

Oil prices fluctuate, natural gas prices plunge 24%

According to MXV, oil prices fluctuated during the trading week of January 15-21 due to mixed fundamental information. On the one hand, China's economy is still stagnant, increasing concerns about consumption demand. On the other hand, tensions in the Middle East continue to escalate, increasing the risk of supply disruptions in the region, supporting price recovery.

At the end of the session, WTI oil price increased by 0.63% to 73.25 USD/barrel. Brent oil increased by 0.34% to 78.56 USD/barrel.

|

Oil prices came under pressure in the first sessions of the week as the market reacted negatively to a series of weak economic data from China and concerns about the gloomy demand outlook increased.

According to the National Bureau of Statistics (NBS), China's gross domestic product (GDP) in the fourth quarter of 2023 increased by only 5.2% year-on-year, 0.1 percentage points lower than forecast. Meanwhile, retail sales growth slowed in December 2023, and housing prices in December 2023 fell the most in nearly 9 years.

However, buying pressure gradually returned to the market as geopolitical risks in the Middle East continued to escalate, raising concerns about supply disruptions in the region. The US has launched military operations against Houthi forces and listed the Yemen-based rebel group as a terrorist group. Notably, Pakistan's response to Iran is alarming for more serious instability across the Middle East since the Israel-Hamas conflict broke out on October 7.

Meanwhile, severe cold weather and operational challenges are still disrupting about 30% of oil production in North Dakota, the third-largest oil-producing state in the US. The North Dakota Energy Regulatory Authority said the state's oil production could take about a month to recover.

According to Bloomberg, oil production across the US was cut by about 10 million barrels this week. Losses in the Permian Basin of Texas and New Mexico were estimated at about 6 million barrels, while the Bakken region of North Dakota recorded a loss of nearly 3.5 million barrels.

A report from oil services firm Baker Hughes showed that the US oil rig count, an indicator of future production, fell by 2 rigs to 497 rigs in the week ending January 19. In addition, the US Department of Energy (DOE) recently announced that the US bought 3.2 million barrels of oil for delivery in April 2024 to add to the Strategic Petroleum Reserve (SPR).

Elsewhere, natural gas prices plunged nearly 24% to a two-week low on a smaller-than-expected drawdown in inventories and forecasts of lower demand due to warmer weather in late January. U.S. utilities withdrew 154 billion cubic feet (bcfd) of gas from storage in the week ended Jan. 12, the U.S. Energy Information Administration (EIA) said, less than the 164 bcf draw forecast by Reuters. Meanwhile, LSEG forecast U.S. gas demand, including exports, would fall from 154.1 bcfd this week to 139.9 bcfd next week.

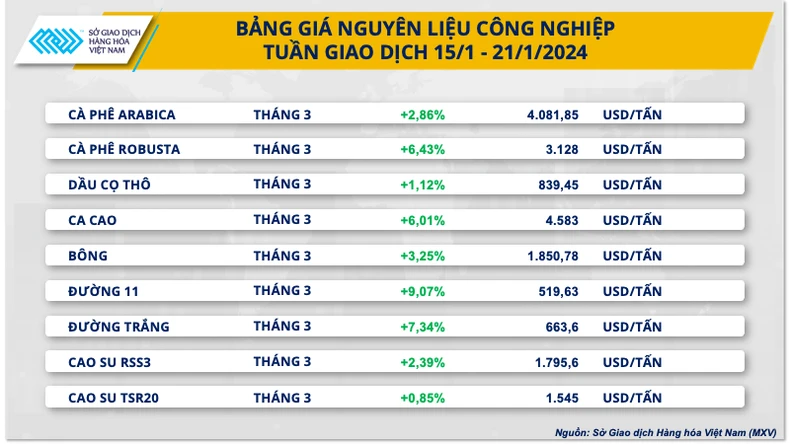

Robusta coffee prices hit 16-year high as Red Sea tensions escalate

At the end of the trading week of January 15-21, the price list of industrial raw materials was covered in green. In particular, Robusta prices increased sharply by 6.43%, reaching the highest level in 16 years. Concerns about escalating tensions in the Red Sea disrupting supply activities between the world's leading Robusta producing and consuming countries pushed prices up sharply.

Over the past week, the conflict in the Red Sea has become more serious with the participation of the US and the UK. This has caused the market to worry about the disruption of the transportation supply chain between Asian countries such as Vietnam and Indonesia with leading consumer markets such as the US and Europe. At that time, the possibility of local supply shortages is high, especially when importing countries cannot find alternative sources of goods from other producing countries.

Arabica prices also rose 2.86%, supported by Robusta prices and unexpectedly weak ICE benchmark inventory data.

|

In the week ending January 21, the ICE-US certified Arabica inventory fell by 8,331 60kg bags, bringing the total number of certified coffee bags to 253,108. This was quite a surprise to the market as the previous inventory data had recovered, albeit at a slow pace. And the decline also raised doubts about the current supply problem in the market.

Previously, the Brazilian government's Crop Supply Agency (CONAB) predicted that Brazil's coffee output in 2024 would reach 58.08 million 60kg bags, up 5.5% compared to 2023.

Meanwhile, the Brazilian Coffee Exporters Association said the South American country shipped 3.78 million bags of green coffee, up 31% from December 2022.

In the domestic market, it was recorded this morning (January 22), the price of green coffee beans in the Central Highlands and the Southern provinces also increased sharply by 1,400 VND/kg. Accordingly, domestic coffee is currently purchased at around 71,800 - 72,500 VND/kg.

Leading the rally last week was sugar 11, which was about 9.07% higher than the reference price. Hot weather in the South-Central region of Brazil, the main sugar producing region, raised concerns about upcoming production activities. In addition, concerns about poor harvests in India and Thailand still had a supportive impact on prices.

Source

![[Photo] Cat Ba - Green island paradise](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F04%2F1764821844074_ndo_br_1-dcbthienduongxanh638-jpg.webp&w=3840&q=75)

Comment (0)