| Wheat prices – an indicator of agricultural market risk from political conflicts. After corn, wheat prices also face the risk of a sharp increase. |

Climate change is making weather patterns unpredictable, putting many major producing nations at a disadvantage. Can the United States seize this opportunity to regain its former glory?

Market share is continuously shrinking.

In recent years, the US wheat market share in the global market has been shrinking. Since the 2020-2021 crop year, US wheat exports have declined for three consecutive crop years, signaling an alarming trend in demand.

According to the latest figures from the U.S. Department of Agriculture (USDA), U.S. wheat exports for the 2023-2024 crop year reached only 19.6 million tons, the lowest level since 1971. It can be said that, in the eyes of importers worldwide, the attractiveness of U.S. wheat has significantly diminished.

|

| U.S. share of global wheat exports over the years. |

Despite the volatile geopolitical situation around the world posing challenges to food security in many countries, U.S. wheat remains a less preferred choice for many international traders. This could be due to several factors, including intense competition from other producers offering lower costs and geopolitical shifts that have altered global trade flows.

As a result, U.S. wheat is losing market share to competitors in the Black Sea and South American regions, which offer more competitive prices and lower transportation costs. This shift is not only a warning sign of a long-term trend but also poses a significant challenge for American farmers and exporters in maintaining and expanding their market share internationally.

Risk of losses in major producing countries

Amidst escalating geopolitical tensions in the Middle East and the Black Sea, global wheat supplies were already facing serious concerns. In particular, recent extreme weather in Russia, the world's leading wheat supplier, has drawn even more attention from international markets.

Last week, eight key grain-growing regions of Russia declared a state of emergency due to severe damage to crops caused by early May frosts. Additionally, southern Russia has experienced virtually no rain since April, resulting in significantly reduced soil moisture in major producing regions such as Krasnodar, Rostov, and Stavropol. According to the Russian Ministry of Agriculture, this frost has affected approximately 1% of the country's grain acreage this year, equivalent to about 900,000 hectares.

|

| Forecasts for Russian wheat production in the 2024/25 season from various organizations. |

The extreme weather conditions in Russia will have a far-reaching impact on the global wheat market due to its crucial role in supplying many countries. In the current volatile environment, diversifying supply sources and developing contingency strategies are essential for wheat-importing nations. This will not only help them mitigate risks but also ensure food security in the face of unpredictable geopolitical and climate instability.

|

| Mr. Pham Quang Anh - Director of the Vietnam Commodity News Center |

Mr. Pham Quang Anh, Director of the Vietnam Commodity News Center, said: “The wheat shortage from Russia could create opportunities for other major wheat exporting countries such as the US, Canada, and Australia. These countries can take advantage of the opportunity to increase production and expand market share that Russia has lost due to the shrinking supply.”

Opportunities for US wheat

With positive supply forecasts this year, the US may have an opportunity to regain market share in the global wheat market. In its May report on global agricultural supply and demand, the USDA projected US wheat production for the 2024-2025 crop year to reach 50.56 million tons, higher than the current year's 49.31 million tons. Exports are also expected to increase to 21.09 million tons next year, up from 19.60 million tons this year.

During a recent annual field trip to Kansas, crop experts projected wheat yields in the state to reach 3.13 tonnes per hectare, the highest level since 2021 and well above the five-year average of 2.85 tonnes per hectare from 2018-2023. In most areas surveyed, despite some impact from adverse weather, the overall situation remained relatively favorable. Wheat yields in northern Kansas are also expected to be at their highest level in three years, suggesting a good supply outlook.

|

| US wheat production over the years |

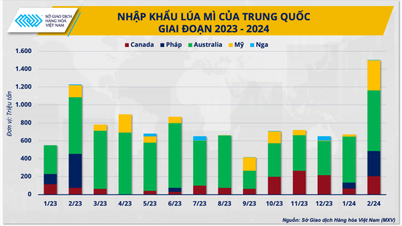

Last December, China placed a record-breaking order for soft red winter wheat (SRW) from the United States. While much of this was subsequently canceled due to sharply falling prices, it demonstrates that the U.S. remains a top choice amidst global supply tensions. Clearly, the U.S.'s role in maintaining stable wheat supplies is undeniable.

Mr. Pham Quang Anh commented: “ The volatility of the global geopolitical situation and the decline in production in Russia could disrupt the current global wheat export market share. The US may emerge this year as a reliable alternative source of supply, and regain some of its former market position.”

With increased production and consistent wheat quality, the U.S. can better meet the demands of even the most discerning markets, thereby expanding its market share and rebuilding trust with international partners.

Source: https://congthuong.vn/co-hoi-cho-lua-mi-my-tim-lai-thi-phan-toan-cau-321635.html

![[Image] Hanoi's urban life under the challenge of a "scorching hot" environment](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779706979265_nang-nong-t5-2026-minh-duy-7-4636-jpg.webp)

![[Image] Close-up view of the interchange connecting the two expressways and Long Thanh Airport.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779703378210_ndo_br_z7863716673926-224453a31600126cce10622af6290afd-4549-jpg.webp)

Comment (0)