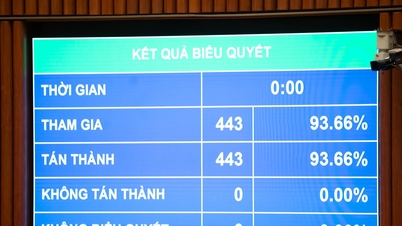

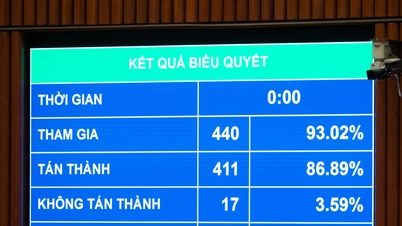

The amended Personal Income Tax Law will take effect from July 1, 2026.

Adding personal income tax to income from gold transfers.

Regarding income subject to personal income tax, the Law specifically stipulates 10 types of income, except for tax-exempt income specified in Article 4 of this Law.

Specifically, income from business; from salaries, wages; capital investment; capital transfer; from capital transfer in other forms; winnings; royalties; franchises; from receiving inheritances, gifts in the form of securities, capital shares in economic organizations, business establishments, real estate and assets that must be registered for ownership or registered for use; and other types of income.

Notably, among other types of income subject to personal income tax, the Law has added income from gold bar transfers. The Government stipulates the taxable gold bar value threshold, the time of application of tax collection and adjusts the personal income tax rate for gold bar transfers in accordance with the roadmap for gold market management.

Among the tax-free incomes, the Law has added income of households and individuals directly producing crops, planted forests, livestock, aquaculture, and fishing products that have not been processed into other products or have only undergone normal preliminary processing; salt production; income from dividends of members of cooperatives and agricultural cooperative unions, and individuals who are farmers signing contracts with enterprises participating in "Large Fields", planting production forests, and aquaculture.

In addition, income from salaries and wages from performing scientific, technological and innovative tasks or from copyright of scientific, technological and innovative tasks when the results of the tasks are commercialized according to the provisions of the law on science, technology and innovation and the law on intellectual property are all tax-exempt.

The progressive tax schedule is stipulated as follows: taxable income from 10 million VND/month is subject to a tax rate of 5%; over 10 - 30 million VND/month is subject to a tax rate of 10%; over 30 - 60 million VND is subject to a tax rate of 20%; over 60 - 100 million VND is subject to a tax rate of 30%; over 100 million VND is subject to a tax rate of 35%.

Household businesses will not be subject to tax if their income is below 500 million VND per year.

Previously, the National Assembly listened to Minister of Finance Nguyen Van Thang present a report on the reception, explanation, revision and completion of the draft Law on Personal Income Tax (amended).

Specifically, regarding taxes on business households and individuals, taking into account the opinions of the reviewers, the opinions of the delegates and the opinions of the National Assembly Standing Committee, the Government has reviewed and adjusted the regulations on taxes on business households and individuals:

Firstly, adjust the tax-free revenue of business households and individuals from 200 million VND/year to 500 million VND/year and deduct this amount before calculating tax at the rate on revenue. At the same time, adjust the tax-free revenue to 500 million VND accordingly.

Second , add a method of calculating tax on income (revenue - expenses) for households and individuals doing business with revenue from over 500 million VND/year to 3 billion VND and apply a tax rate of 15% (similar to the corporate income tax rate for businesses with revenue under 3 billion VND/year). At the same time, it is stipulated that these individuals can choose the method of calculating tax based on the rate on revenue.

Regarding the progressive tax schedule, according to the Minister, the tax schedule has been adjusted to reduce the tax rate from 15% (at level 2) to 10% and the tax rate from 25% (at level 3) to 20% to avoid sudden increases between levels, ensuring the reasonableness of the tax schedule.

Regarding the family deduction level, taking into account the opinions of the reviewers, the opinions of the National Assembly Deputies and the opinions of the National Assembly Standing Committee, the Government has included the family deduction level stipulated in Resolution No. 110/2025/UBTVQH15 of the National Assembly Standing Committee (the deduction level for the taxpayer himself is 15.5 million VND/month, for each dependent is 6.2 million VND/month) stipulated in the draft Law and assigned the Government to submit to the National Assembly Standing Committee to adjust this family deduction level based on fluctuations in prices and income to suit the socio-economic situation in each period.

Regarding the tax on gold transfers, Minister Nguyen Van Thang affirmed that the proposal to collect tax on gold transfers has been carefully reviewed and studied, based on the synthesis of opinions from agencies, ministries, branches and the acceptance of review opinions, opinions of National Assembly deputies, and opinions of the National Assembly Standing Committee.

The Government's assignment of specific regulations on the taxable gold bar value threshold is to eliminate cases where individuals buy and sell gold for the purpose of saving and storing (not for business purposes).

Since this is a new regulation with a wide range of impacts, the regulation as in the draft Law is a necessary step to implement the direction of the Party and State on strictly managing gold trading activities, contributing to limiting speculation in gold, attracting social resources to participate in the economy.

Regarding the family deduction level, taking into account the opinions of the National Assembly Deputies and the opinions of the National Assembly Standing Committee, the Government has included the family deduction level stipulated in Resolution No. 110/2025/UBTVQH15 of the National Assembly Standing Committee (the deduction level for the taxpayer himself is 15.5 million VND/month, for each dependent is 6.2 million VND/month) stipulated in the draft Law on Personal Income Tax (amended) and assigned the Government to submit to the National Assembly Standing Committee to adjust this family deduction level based on fluctuations in prices and income to suit the socio-economic situation in each period.

Source: https://daibieunhandan.vn/quoc-hoi-thong-qua-luat-thue-thu-nhap-ca-nhan-sua-doi-10399869.html

![[Photo] Explore the US Navy's USS Robert Smalls warship](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F10%2F1765341533272_11212121-8303-jpg.webp&w=3840&q=75)

![[Photo] The captivating scenery of the fragrant maple forest in Quang Tri](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F10%2F1765353233198_lan09046-jpg.webp&w=3840&q=75)

![[Podcast] National Assembly approves personal allowance deduction of VND 15.5 million/month](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/10/1765340032834_hnm-1cdn-vn-thumbs-540x360-2025-11-04-_hnm-1cdn-vn-thumbs-540x360-2025-06-27-a7b22b8722-_thu.jpeg)

![[Video] The craft of making Dong Ho folk paintings has been inscribed by UNESCO on the List of Crafts in Need of Urgent Safeguarding.](https://vphoto.vietnam.vn/thumb/402x226/vietnam/resource/IMAGE/2025/12/10/1765350246533_tranh-dong-ho-734-jpg.webp)

Comment (0)