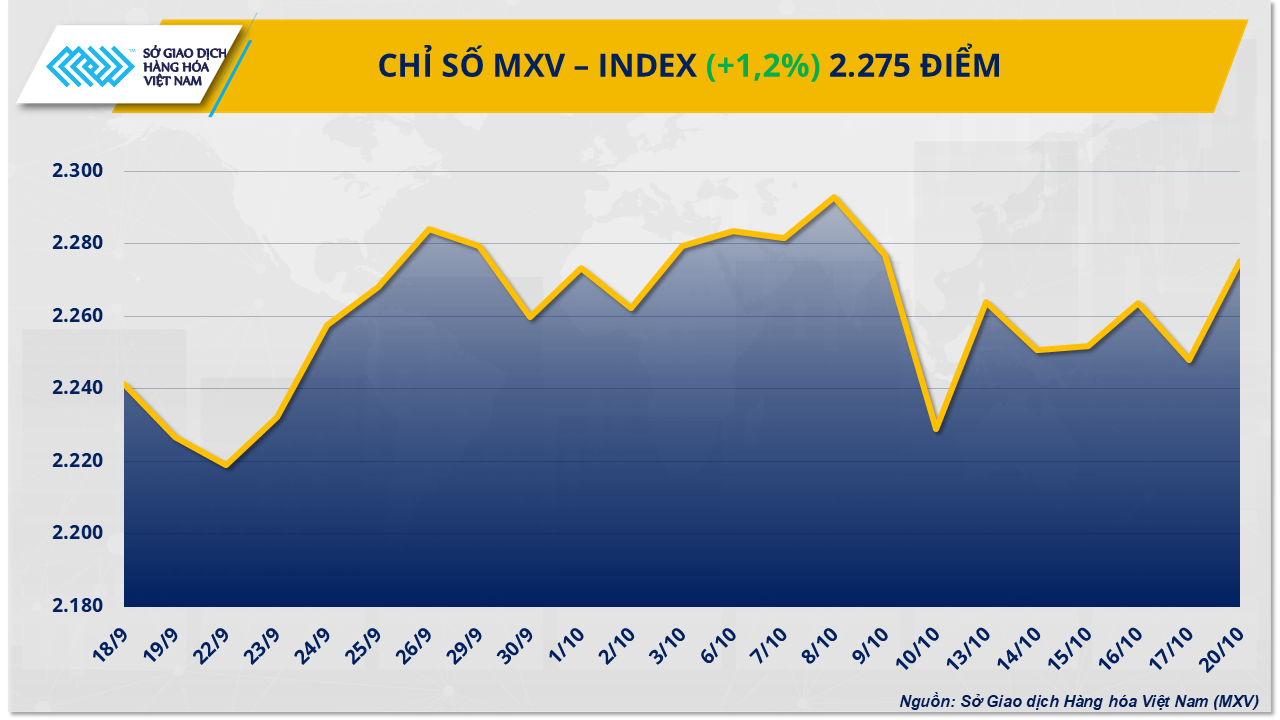

Steady demand from China supports sugar price recovery

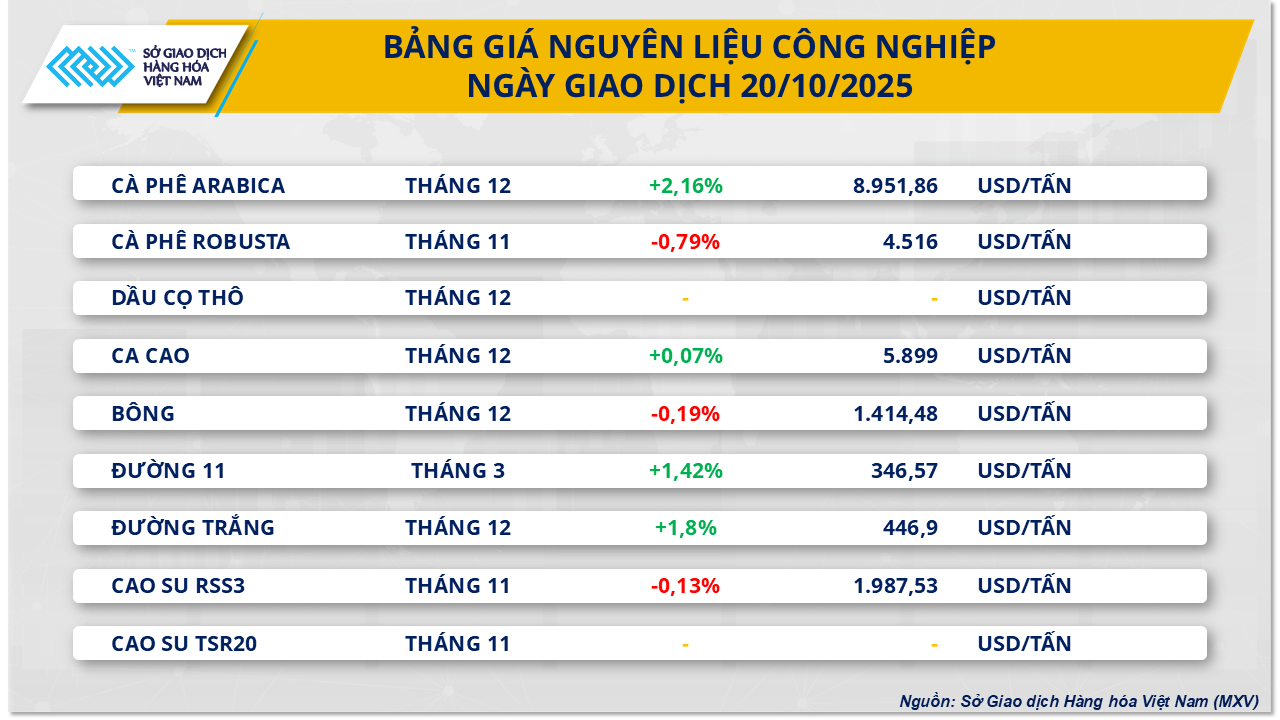

At the end of yesterday's trading session, the industrial raw materials market recorded positive buying pressure on most key commodities in the group. In particular, two sugar commodities recorded a slight recovery after the previous volatile week. At the close, raw sugar price 11 increased by more than 1.4% to 346.5 USD/ton, while white sugar increased by 1.8% to 447 USD/ton.

According to MXV, stable demand continued to be the main support for sugar prices in yesterday's session. Data from the General Administration of Customs of China showed that in September, the country imported 550,000 tons of sugar, down from the previous month but still up nearly 36% compared to the same period last year. From the beginning of the year to the end of September, the total import volume reached 3.16 million tons, up 9.4% compared to the same period in 2024.

Meanwhile, in Brazil - the world's largest sugar producer, output has seen a slight decline in the current crop year. According to data as of October 1, the Central - South region of Brazil has only crushed about 491 million tons of sugarcane, down 3% compared to the previous crop year. However, the proportion of sugarcane used for sugar production still reached a record 52.7%, showing that factories still prioritize sugar processing over ethanol.

However, according to MXV, world sugar prices are likely to remain under pressure as global supplies remain high. The Itaú BBA report shows that the harvest in the Northern Hemisphere is progressing well, especially in India, Thailand and Central America, where rainy weather conditions are favorable for production.

In the Russian market, as of early October, about 45% of the sugar beet area had been harvested, with yields up 3.2% year-on-year, despite a decrease in sucrose content. Russian sugar production in the 2025-2026 crop year is forecast to reach 6.6 million tonnes.

In the European Union, although the planted area is down 10% compared to the previous season, the harvest has started well with good yields in France and Germany. Rainfall in July-August has helped improve sucrose levels after the previous drought in May-June had negatively affected the growth of the crop.

In the domestic market, the price of unofficial sugar recorded in the trading session on October 20 showed the difference between regions. In the Central region, yellow sugar was offered for sale at around 16,400 - 16,500 VND/kg. Sugar prices in the South were higher, fluctuating at 17,600 - 17,800 VND/kg, while in the West, it was traded around 17,400 - 17,500 VND/kg.

At the factory, the offered price continues to decrease. Accordingly, Lam Son yellow sugar is currently offered at 19,000 VND/kg, while RS Nghe An sugar is traded at 17,300 VND/kg.

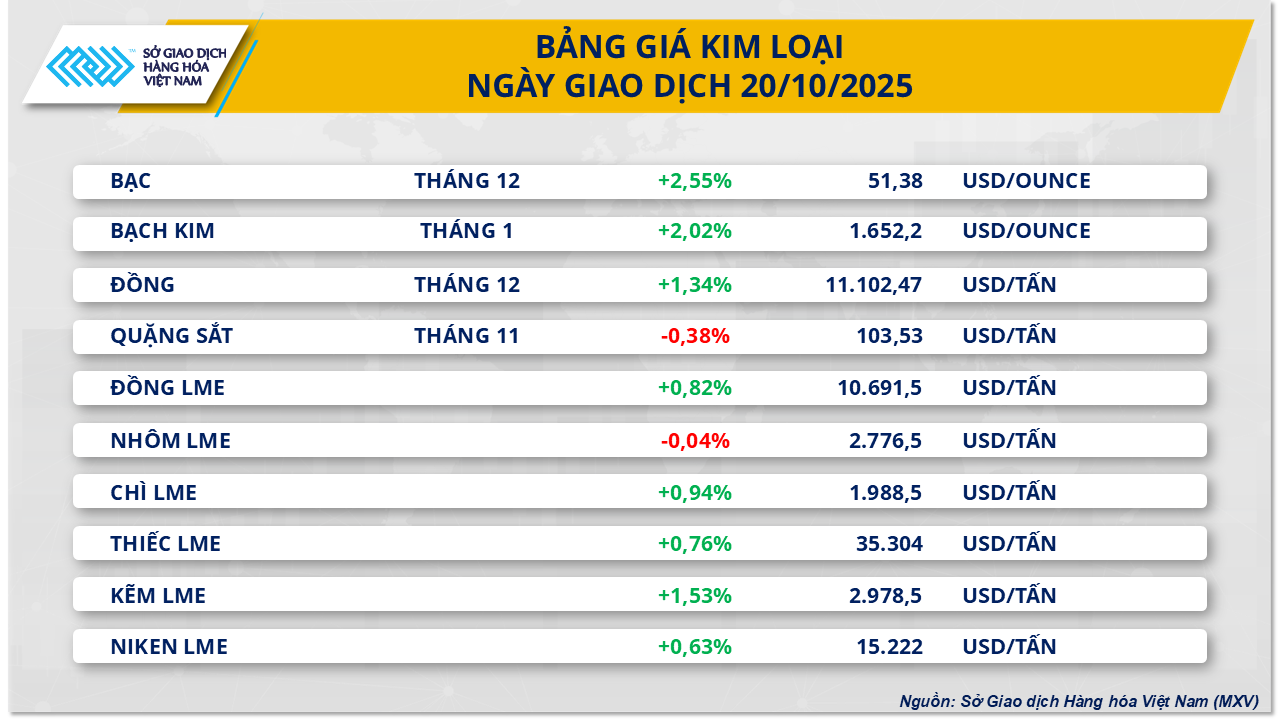

Iron ore prices extended their decline to the third consecutive session.

Meanwhile, yesterday's session saw green dominate the metal market with 8 out of 10 commodities increasing sharply. Of which, iron ore prices continued to weaken as they continued to fall nearly 0.4% to 103.53 USD/ton, marking the third consecutive session of decline.

According to data from MXV, the main reason comes from the trade tension between the US and China. This is raising concerns about the future consumption prospects of iron ore, especially when domestic demand in China is weakening. In addition, the US is threatening to impose triple-digit tariffs on Chinese goods, effective from November 1, and many other countries are also raising trade barriers to prevent cheap steel from flooding the international market from China.

In China - the world's largest iron ore consumer, the plan to cut steel production is gradually being implemented. Data from research organization SteelHome shows that iron ore inventories at Chinese ports have been continuously increasing since the end of September, reaching 133.4 million tons in the week ending October 17. In addition, the real estate segment, which is a large output for steel use, remains stagnant. Data from the National Bureau of Statistics (NBS) of China shows that new home prices in September fell 2.2% compared to the same period last year, although they narrowed compared to August.

Furthermore, according to Worldsteel, steel demand in China is forecast to fall by about 2% in 2025 and continue to fall by about 1% in 2026 as the housing market shows signs of bottoming out.

Domestically, domestic steel prices have stabilized after an upward adjustment in early September. This morning, CB240 coil prices were trading at around VND13.5 million/ton, while D10 CB300 rebar prices fluctuated at VND13.1 million/ton. Thanks to well-maintained construction and public investment activities, domestic consumption has remained at a relatively good level, ensuring price balance. However, steel exports are facing difficulties as many major markets have increased trade defense measures.

According to the Customs Department, in the first half of October (from October 1 to October 15), iron and steel imports reached nearly 701,500 tons, an increase of about 12% compared to the second half of September; meanwhile, exports decreased sharply by about 50%, from 473,000 tons to about 236,440 tons.

Source: https://baotintuc.vn/thi-truong-tien-te/thi-truong-hang-hoa-khoi-sac-ap-luc-van-de-nang-len-gia-quang-sat-20251021083407978.htm

![[Photo] General Secretary To Lam receives the Director of the Academy of Public Administration and National Economy under the President of the Russian Federation](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F08%2F1765200203892_a1-bnd-0933-4198-jpg.webp&w=3840&q=75)

Comment (0)